Have you ever had enough money for one small thing right away, but not enough yet for something bigger you really wanted? That happens to people of all ages. Money choices are part of everyday life. A person might buy something now, or save money for later. Learning how to choose between those ideas helps you make a plan and reach a goal.

A financial goal is something you want to do with money. Some goals happen soon. These are called short-term goals. A short-term goal is usually something you can reach in a short amount of time, such as in a few days, a few weeks, or a few months.

Short-term goal means a money goal you plan to reach soon.

Spending goal means something you plan to buy with money.

Savings goal means something you plan to set money aside for until you have enough.

When you understand short-term spending and savings goals, you can make better choices. You can decide, "Should I use my money now?" or "Should I save it until I have enough for something else?" Both choices can be good, but they are for different situations.

A goal gives your money a job. Instead of spending money without thinking, you can choose what matters most. Maybe you need new crayons for school. Maybe you want to save for a soccer ball. A goal helps you focus.

Money goals also help people practice patience and responsibility. If you spend every coin as soon as you get it, it can be hard to buy something that costs more. But if you save part of your money, your money can grow little by little.

Even small amounts matter. If you save $2 each week, after 4 weeks you have \(2 + 2 + 2 + 2 = 8\), so you have $8. Small steps can help you reach a goal.

Many adults still use the same kind of planning kids use: they set a goal, check the cost, and save a little at a time until they have enough.

Short-term goals are useful because they feel close and possible. A third-grade student can often reach a short-term goal with careful planning.

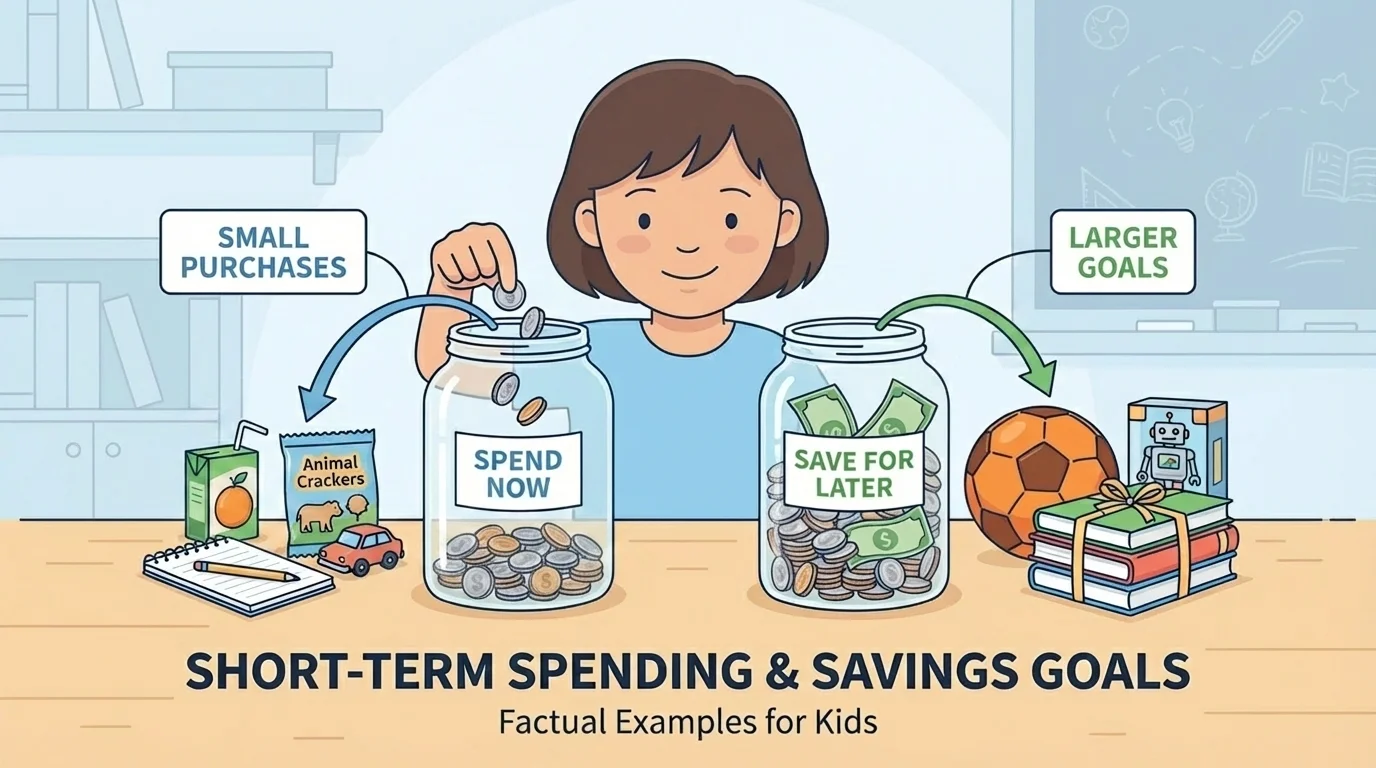

[Figure 1] There are two important kinds of short-term money goals. One is a spending goal, and the other is a savings goal. A spending goal uses money soon for something you need or want, while a savings goal means keeping money set aside until later.

A short-term spending goal might be buying a notebook for school this week or paying for a small treat at a school event. A short-term savings goal might be saving for a new set of markers over the next month or saving for a small toy by the end of the season.

The main difference is what happens to the money. In a spending goal, the money is used soon. In a savings goal, the money is kept for later until there is enough for the goal.

Both kinds of goals can be short-term. For example, buying glue for a class project tomorrow is short-term. Saving for a puzzle you want next month is also short-term.

A short-term spending goal is often for something you can buy now or very soon. Sometimes it is a need, and sometimes it is a want. Here are some examples.

School supply goals: buying pencils, erasers, folders, or poster board for a project. These are often needs because they help with schoolwork.

Gift goals: buying a birthday card or a small birthday gift for a friend or family member. This is a spending goal because the money is used soon for a planned purpose.

Event goals: bringing money for a school fair, book sale, or class snack day. The goal is to have enough money when the event happens.

Personal item goals: buying stickers, a small action figure, a yo-yo, or a snack. These are wants, but they are still examples of spending goals if you plan to buy them soon.

Hobby goals: paying for a pack of trading cards, art paper, or a music notebook. If the money is meant to be used right away, it is a spending goal.

| Goal | Type | Why |

|---|---|---|

| Buy a notebook today | Short-term spending | Money is used now |

| Buy a snack at Friday's game | Short-term spending | Money is used soon |

| Buy a birthday gift this week | Short-term spending | It is planned for the near future |

| Pay for poster board tomorrow | Short-term spending | It is needed very soon |

Table 1. Examples of short-term spending goals and why they fit that category.

Spending goals are easier to reach when you know the price. If your snack costs $3 and you have $5, then after you buy it, you have \(5 - 3 = 2\) dollars left. Planning before spending helps you avoid using all your money without thinking.

A short-term savings goal is for something you cannot or do not want to buy right away. You save money over time until you have enough. The time is still short, but you need to wait a little.

Examples include saving for a book set, a board game, a stuffed animal, a jump rope, a larger art kit, or part of the cost of a class trip. These goals may take several weeks or a few months.

Suppose you want a game that costs $18, but you only have $6. You need \(18 - 6 = 12\) more dollars. That means your plan is to save $12 more before buying the game.

Another example is saving for sports equipment. A student might save for shin guards, swim goggles, or a basketball. These items may cost more than a small daily purchase, so saving makes sense.

A student may also save for a need. For example, maybe a lunch box costs more than the money they have today. If they set aside money each week, that becomes a short-term savings goal. Saving is not only for wants.

Needs and wants both matter

A need is something important for everyday life, learning, health, or safety. A want is something nice to have but not necessary. Some short-term goals are needs, like school supplies. Some are wants, like a toy or treat. Good planning helps you decide which goal should come first.

As we saw earlier in [Figure 1], saving means putting money aside on purpose. You do not spend it yet because you are working toward a goal.

Sometimes a goal can sound similar, so it helps to ask a few questions.

Question 1: Am I using the money now, or am I setting it aside?

If the money is being used now or very soon, it is a spending goal. If the money is being kept for later, it is a savings goal.

Question 2: Do I already have enough money?

If you already have enough and plan to buy the item soon, that is often a spending goal. If you do not have enough yet and need time to collect more, that is often a savings goal.

Question 3: How long will it take?

Both kinds can be short-term, but a savings goal usually lasts longer than a spending goal because you must wait and collect money.

For example, bringing $2 tomorrow to buy a pencil grip is a spending goal. Saving $2 each week for 5 weeks for a $10 sketchbook is a savings goal because \(2 + 2 + 2 + 2 + 2 = 10\).

You already know how to add and subtract money amounts. Those math skills help you compare a price with the money you have and figure out how much more you need.

Knowing the difference helps you make a plan that fits the goal.

[Figure 2] A simple money plan has clear steps. First choose the goal, then find the price, count how much money you already have, and decide how much more you need.

You can think of the plan like this: choose, check, count, and save or spend. This keeps your goal organized and easy to follow.

Step 1: Choose your goal. Be specific. Instead of saying "I want something fun," say "I want to buy a new marker set."

Step 2: Find the cost. If the marker set costs $9, write that down.

Step 3: Count the money you already have. Maybe you have $4.

Step 4: Find how much more you need. Subtract: \(9 - 4 = 5\). You need $5 more.

Step 5: Decide how to reach the goal. You might save $1 each week for 5 weeks, because \(1 + 1 + 1 + 1 + 1 = 5\).

This kind of planning works for spending goals and savings goals. If the item is needed right away and you already have enough, you can spend. If not, you save until you are ready.

Students can track progress week by week, and [Figure 3] helps show how savings can grow toward a short-term goal. Looking at progress makes the goal feel real and reachable.

Example 1: Saving for a class trip

Mia wants to go on a class trip that costs $15. She already has $3. How much more does she need?

Step 1: Write the total cost.

The trip costs $15.

Step 2: Write the money Mia already has.

She has $3.

Step 3: Subtract to find the amount still needed.

\(15 - 3 = 12\)

Mia needs $12 more. This is a short-term savings goal because she is collecting money for later.

In a chart like this, each week adds a little more to the total. That makes it easier to see how regular saving leads to success.

Example 2: Buying a notebook now

Leo needs a notebook that costs $4. He has $6. Does he have enough, and how much will be left?

Step 1: Compare the money he has with the cost.

Leo has $6, and the notebook costs $4.

Step 2: Subtract to find the money left after buying it.

\(6 - 4 = 2\)

Leo has enough to buy the notebook, and he will have $2 left. This is a short-term spending goal because the money is used right away for a need.

Some goals happen quickly, while others take several weeks of saving. Both are part of good financial planning.

Example 3: Saving each week for a toy

Aria wants a toy that costs $12. She saves $2 each week. How many weeks will it take if she starts with $0?

Step 1: Count by twos until you reach $12.

\(2, 4, 6, 8, 10, 12\)

Step 2: Count how many weeks that takes.

It takes 6 weeks of saving $2.

It will take 6 weeks. This is a short-term savings goal.

These examples show that simple math can help with money decisions. You add to see how savings grow, and you subtract to see how much more is needed or how much is left.

Sometimes you may have more than one goal. You might want to buy a snack and also save for a book. In that case, you need to decide what is more important right now.

If something is a need, it often should come before a want. For example, if you need a folder for school and also want a small toy, buying the folder first may be the smarter choice.

Plans can also change. Maybe the item costs more than you thought. Maybe you decide on a different goal. That is okay. A good plan can be adjusted. If your goal changes from a $10 puzzle to a $14 puzzle, then the extra amount needed is \(14 - 10 = 4\) more dollars than before.

Saving part of your money and spending part of your money is also a smart idea for many people. For example, if you get $8, you might spend $3 on a snack and save $5 for a game. Since \(3 + 5 = 8\), all the money has a purpose.

"A goal without a plan is hard to reach, but a goal with small steps can be reached one step at a time."

Being thoughtful with money does not mean never spending. It means choosing carefully so your money helps you do what matters most.

Short-term spending and savings goals are everywhere in daily life. At school, students may plan for supplies, book fairs, or field trips. At home, they may save for a game, craft kit, or sports item. In activities, they may save for team gear or music supplies.

Families use similar ideas too. A family may have a spending goal for groceries this week and a savings goal for a special outing next month. The time is short, but there is still a plan.

When you understand short-term goals, you become more confident with money. You learn that money is not only for spending fast. It can also be used wisely, a little at a time, to reach something important.

Whether your goal is a need or a want, the important part is to think ahead. Ask what the goal is, how much it costs, how much money you have, and whether you should spend now or save for later.