One financial decision made in five minutes can affect your choices for five years. Buying a phone on impulse, missing a payment, signing up for a subscription you forget about, or saving part of every paycheck may seem small in the moment, but each choice changes what you can do next. Personal finance is not just about money. It is about freedom, pressure, priorities, and responsibility.

Every time you choose what to do with money, you are making a financial decision. That includes obvious choices, such as whether to save $100, but also less obvious ones, such as whether to take extra work hours, how to pay for transportation, or whether a "deal" is really worth it. Financial decisions matter because money is limited. If you use money for one purpose, you usually cannot use the same money for something else at the same time.

For high school students, financial choices often start with everyday situations: school lunches, streaming subscriptions, gas, rideshares, sports fees, clothes, entertainment, gifts, and saving for a car, college, training program, or emergency. These decisions become more serious over time because habits form early. A student who learns to compare options carefully is much more prepared for adult decisions about housing, insurance, taxes, and loans.

Alternative means one possible choice among several options.

Consequence means the result of a decision, including both intended and unintended effects.

Responsibility means the duty to manage money honestly, carefully, and with awareness of how your choices affect yourself and others.

Opportunity cost is the value of the next best option you give up when you choose something else.

Good financial decision-making is not about picking the cheapest option every time. Sometimes the best choice costs more now but saves money later. Sometimes the most financially sound option is to wait. Sometimes the right decision depends on your goals, such as reducing stress, helping family, avoiding debt, or preparing for college. Money choices are tied to values.

A strong decision begins by recognizing all the realistic choices, not just the most tempting one. Suppose a student earns $240 from a weekend job and wants better transportation to school activities. The alternatives might include saving for a used bike, paying for occasional rides, contributing toward family gas costs, or continuing to use free school transportation. If the student only thinks about the bike, then the decision is incomplete.

When people overlook alternatives, they often make emotional decisions instead of informed ones. Sales tactics, peer pressure, urgency phrases like "limited time only," and fear of missing out can narrow your thinking. A systematic thinker pauses and asks: What are my real options? Which choice best supports my goals? What am I giving up by choosing this?

The idea of opportunity cost is especially important. If you spend $300 on concert tickets, the cost is not only the $300. It is also whatever else that $300 could have done, such as covering car insurance, building savings, or reducing future stress. The more limited your money is, the more important opportunity cost becomes.

Many bad financial choices start with bad information. Reliable information is accurate, current, and complete enough to support a decision. Unreliable information is misleading, incomplete, or designed mainly to persuade rather than inform. An advertisement may highlight "only $20 a month" while hiding a contract length, fees, taxes, or penalties.

Reliable sources often include bank or credit union websites, official account disclosures, pay stubs, loan documents, government consumer websites, billing statements, and direct communication with a company about terms and fees. Friends, influencers, and advertisements may provide ideas, but they should not be treated as final sources for financial decisions.

To evaluate information, ask several questions. Who created this information? What do they gain if I choose this option? Are the total costs clearly shown? Is the information recent? Are important details missing? If a company offers a free trial, for example, the reliable-information questions include when the trial ends, whether payment begins automatically, how cancellation works, and whether taxes or processing fees apply.

Reliable information reduces expensive mistakes. In personal finance, the most important details are often not the headline price. You need to look for total cost, interest, fees, penalties, deadlines, and contract terms. Two choices can look similar at first and become very different once hidden costs are included.

Comparison shopping is part of using reliable information. If one bank account has no monthly fee but requires a minimum balance, while another charges a fee only after a certain number of withdrawals, the best account depends on how you actually use money. A good decision uses facts about both the product and your own behavior.

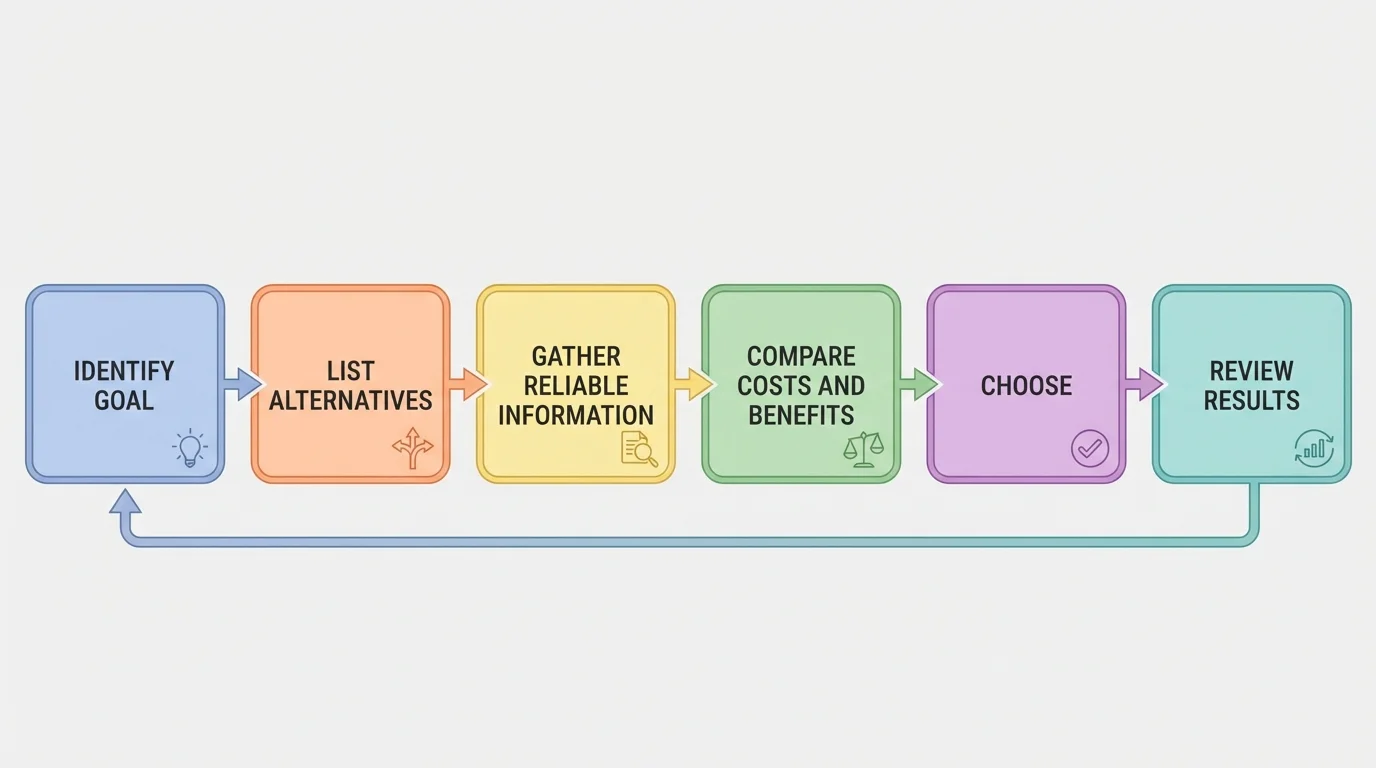

Strong financial thinkers do not rely only on instinct. They use a repeatable process, as [Figure 1] shows, to move from a goal to a choice and then to a review of the results. This approach lowers the chance of impulse decisions and increases the chance that money is used in ways that match long-term goals.

A practical process has six parts. First, identify the goal. Second, list alternatives. Third, gather reliable information. Fourth, compare costs, benefits, and risks. Fifth, choose and act. Sixth, review the outcome later. The review step matters because financial decision-making improves when you learn from what happened, not just from what you expected.

Consider a student deciding whether to buy a laptop immediately. The goal might be school productivity. Alternatives could include buying new, buying refurbished, borrowing temporarily, saving for a later purchase, or using school devices. Reliable information would include price, warranty, battery life, software compatibility, repair costs, and return policy. Comparing alternatives means looking beyond appearance and asking which option best fits school needs and budget limits.

This process also helps separate needs from wants. A need is something essential for health, safety, work, or education. A want is something desirable but not essential. The difference is not always fixed. Internet access may be a want in one situation and a need in another if it is necessary for schoolwork or a job application. Good judgment depends on context.

Many subscription services make cancellation harder than sign-up because they depend on people forgetting to stop automatic payments. A small monthly charge can become a surprisingly large annual cost.

If a subscription costs $12 per month, the yearly cost is \(12 \times 12 = 144\), so the total is $144 per year. If that money were saved instead, it could cover books, athletic fees, exam costs, or part of an emergency fund.

Teenagers may not yet be signing mortgages, but they already face meaningful money choices. These include whether to spend or save income, whether to use cash or a debit card, whether to open a bank account, how to manage digital payments, whether to borrow from family, whether to take on a car payment later, and how much to work during the school year.

Spending decisions often look simple but involve alternatives. Buying trendy shoes may compete with saving for a school trip. Taking on more work hours may bring more income but reduce time for studying, sleep, or activities that matter for scholarships and future opportunities. Financial decisions often involve trade-offs between money and time.

Education choices are also financial choices. A student comparing college, community college, apprenticeship, military service, or immediate employment is comparing tuition, wages, debt, training length, career outcomes, and lifestyle. The smartest choice is not the same for everyone because goals, values, and family situations differ.

Case study: comparing phone plans

A student is choosing between two phone options.

Step 1: Identify the alternatives

Plan A costs $35 per month with no contract. Plan B costs $25 per month but requires a 12-month contract and a $120 activation fee.

Step 2: Find total yearly cost

Plan A for one year costs \(35 \times 12 = 420\), so the total is $420.

Plan B for one year costs \(25 \times 12 = 300\). Adding the activation fee gives \(300 + 120 = 420\), so the total is $420.

Step 3: Compare consequences and responsibilities

The yearly totals are equal, but the consequences differ. Plan A offers flexibility because there is no contract. Plan B locks the student into a longer commitment.

Even when the math ends in a tie, the best choice may depend on flexibility, risk, and personal goals.

Financial decisions also include protection against mistakes and fraud. Using digital payment apps, saving passwords insecurely, ignoring account statements, or sharing account information can lead to losses. Responsible money management includes protecting private information, checking balances, and noticing unauthorized charges quickly.

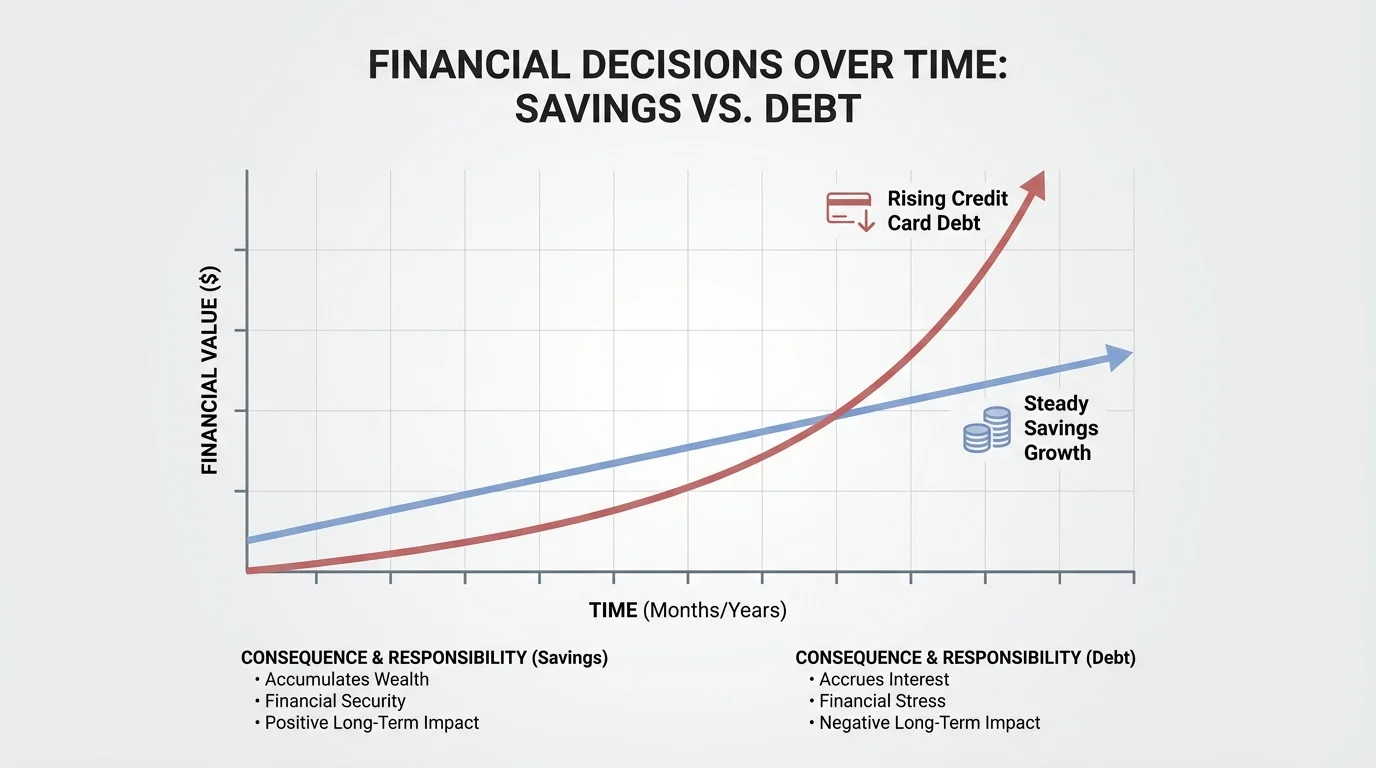

Money decisions are often deceptive because the immediate result is easy to see, while later effects are harder to notice. Over time, choices can push finances in very different directions, as [Figure 2] illustrates with rising savings and growing debt. Saving regularly can build options and security, while repeated borrowing or missed payments can create pressure that grows month after month.

Some consequences are short-term, such as having less cash available after a purchase. Others are long-term, such as lower savings, damaged credit history, fewer future choices, or more stress. A person who buys now and pays later may enjoy the short-term benefit but face long-term costs through interest and fees.

Saving benefits from consistency. If you save $25 each week for one year, the total saved is \(25 \times 52 = 1{,}300\), so you would have $1,300, not counting any interest. That amount could cover an emergency, a training course, or a major purchase without borrowing.

Debt can also grow over time, especially when payments are late or balances are carried from month to month. If you borrow $500 from family or on a credit account and agree to pay back $50 each month, then ten on-time payments would repay \(50 \times 10 = 500\). But if fees or interest are added, the total cost becomes greater than the original $500. This is why the full terms of borrowing matter.

Credit history and future consequences matter even if you are not using major loans yet. Paying bills on time, avoiding overdrafts, and handling accounts responsibly help build trust with financial institutions. Missing payments, ignoring bills, or defaulting can make later borrowing more difficult and more expensive.

Risk is another long-term consequence to consider. Some financial choices promise fast rewards, but high return often comes with high risk. For example, buying something because a social media post says its price will "definitely go up" is not a reliable investment strategy. Reliable financial decisions require evidence, not hype.

As seen earlier in [Figure 1], reviewing outcomes is part of good decision-making. If a past choice led to overdraft fees, overspending, or regret, that result provides useful data. Smart decision-makers use consequences as feedback.

Managing money responsibly means more than keeping track of your own spending. It includes planning ahead, meeting obligations, acting honestly, and understanding that your money choices can affect family members and the wider community. One of the clearest responsibilities is budgeting, which means assigning income to priorities before spending on optional items.

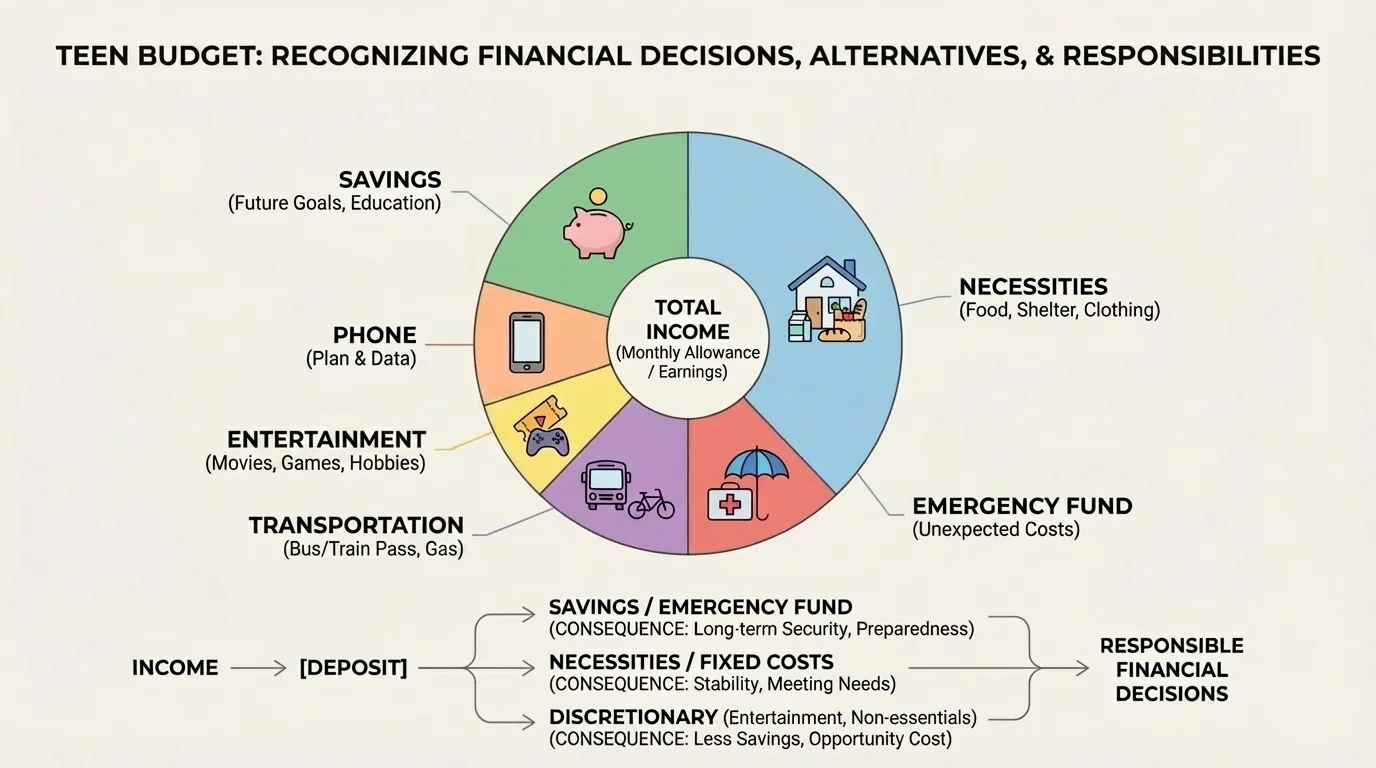

[Figure 3] A budget does not need to be complicated. It is simply a plan for where money will go. If a student earns $200 in two weeks, a budget might set aside part for savings, part for transportation, part for personal spending, and part for upcoming school costs. Without a plan, money tends to disappear into whatever feels urgent or appealing at the moment.

Responsibility also includes paying people back when you owe them, reading agreements before signing, keeping receipts or records, reporting errors on statements, and avoiding purchases you know you cannot realistically afford. Financial honesty matters. Borrowing money with no plan to repay it or using someone else's payment account without permission is both irresponsible and harmful.

Money decisions can affect families. If a teen spends all earned income on entertainment, they may be unable to contribute to gas, supplies, or shared needs. In some households, a student's financial choices matter directly because earnings help support siblings, bills, or groceries. Community values may shape decisions too. Some people prioritize helping relatives, supporting local businesses, donating, or avoiding companies whose practices conflict with their ethics.

| Decision Area | Responsible Behavior | Possible Consequence of Irresponsibility |

|---|---|---|

| Bank account | Monitor balance and fees | Overdrafts or unexpected charges |

| Borrowing | Repay on time and know the terms | Damaged trust and added costs |

| Subscriptions | Track renewal dates | Repeated charges for unused services |

| Work income | Save part of each paycheck | No cushion for emergencies |

| Digital payments | Protect passwords and check transactions | Fraud or stolen funds |

Table 1. Examples of responsible financial behaviors and the consequences of failing to manage them carefully.

Limited resources mean every choice uses money, time, or energy that cannot be used somewhere else at the same moment. That idea connects directly to trade-offs in personal finance.

Taxes are another responsibility connected to income. If you work a job, your paycheck may include deductions. Understanding a pay stub helps you know the difference between gross income and net income. Gross income is the total earned before deductions. Net income is the amount you actually take home after deductions.

Systematic decision-making becomes clearer when you compare realistic options side by side. Numbers matter, but so do timing, flexibility, risk, and goals.

Case study: spend now or save for a larger goal

A student has $480 saved and earns $60 per week. They want to buy a gaming system for $360, but they also want to save $900 for a summer training program.

Step 1: Find the gap to the larger goal now

The amount still needed is \(900 - 480 = 420\), so the student needs $420 more.

Step 2: Find how many weeks it takes if they do not buy the gaming system

At $60 per week, the time needed is \(420 \div 60 = 7\) weeks.

Step 3: Find how many weeks it takes if they buy the gaming system first

After buying it, savings would be \(480 - 360 = 120\). The amount still needed for the training program would then be \(900 - 120 = 780\). At $60 per week, that takes \(780 \div 60 = 13\) weeks.

The opportunity cost of buying the system now is at least 6 extra weeks of saving time toward the training goal.

This example shows why consequences are not only about money amounts. They are also about timing. Delays can matter if a deadline exists, such as tuition due dates, application fees, or travel costs.

Case study: cheaper item or better value?

A student needs headphones for school and chooses between Option A at $18 lasting about 3 months and Option B at $42 lasting about 12 months.

Step 1: Compare yearly cost for Option A

If Option A lasts 3 months, then 4 sets are needed in a year. The cost is \(4 \times 18 = 72\), so the yearly total is $72.

Step 2: Compare yearly cost for Option B

Option B costs $42 for the full year.

Step 3: Decide using total cost and reliability

Although Option A is cheaper at the moment of purchase, Option B is the better long-term value if the durability estimate is accurate.

A low sticker price does not always mean a lower overall cost.

These examples connect back to [Figure 2], which shows that repeated small choices can produce very different long-term outcomes. This is why financially responsible people think in patterns, not just in single purchases.

Personal financial decisions should make sense not only mathematically but also ethically and personally. A decision that works for one person may be wrong for another because values differ. One student may value independence and build an emergency fund first. Another may prioritize helping family with bills. Another may reduce work hours to protect grades and mental health because academic success is the larger long-term goal.

Individual and community values can shape spending, saving, and giving. Some people prefer to support local businesses even if prices are slightly higher. Some avoid products from companies they consider harmful. Some set money aside for donations or mutual aid. Values do not remove the need for careful comparison, but they do help explain why two informed people may choose differently.

"Do not save what is left after spending, but spend what is left after saving."

— Common financial principle

The best personal financial decisions combine reliable information, realistic alternatives, careful analysis of consequences, and responsibility for outcomes. If any one of these is missing, the decision is weaker. A student who knows the price but not the contract terms is missing information. A student who knows the alternatives but ignores long-term effects is missing consequence analysis. A student who understands the numbers but ignores family obligations is missing responsibility.

Financial decision-making is a skill, and like any skill, it improves with practice, reflection, and honesty. People make mistakes with money. What matters is learning to slow down, compare carefully, ask better questions, and act in ways that protect both present needs and future possibilities. The goal is not perfection. The goal is informed, responsible choice.