A single swipe, tap, click, or transfer can move money in seconds, but the account behind that payment determines whether the transaction helps you stay in control or pushes you into fees and debt. For many people, financial trouble does not begin with one huge mistake. It begins with small choices: using the wrong account for the wrong purpose, forgetting to track a balance, or treating borrowed money like free money.

A financial account is more than a place to store money. It is a tool for managing daily life. People use accounts to receive paychecks, save for goals, pay bills, shop online, transfer money, and build a record of their financial behavior. A payment method is the way money moves from one person or institution to another. Choosing wisely matters because every method has trade-offs in security, speed, cost, and control.

For example, paying for lunch with cash is immediate and simple, but cash is hard to recover if it is lost. Using a debit card is convenient, but it can lead to overdraft fees if the account balance is too low. Using a credit card may offer fraud protection and rewards, but carrying a balance can trigger interest charges. A smart consumer understands not just how to pay, but when each method makes sense.

Account means a financial record held by a bank, credit union, or other company that tracks money you deposit, withdraw, borrow, or store.

Payment method means the tool or process used to transfer money, such as cash, debit card, credit card, electronic transfer, or mobile wallet.

Balance is the amount of money in an account at a given time, while available balance is the amount currently usable after pending transactions and holds are considered.

When students start earning income, receiving money digitally, or paying for subscriptions, they begin entering the same financial system adults use. Learning these tools early can prevent expensive mistakes later.

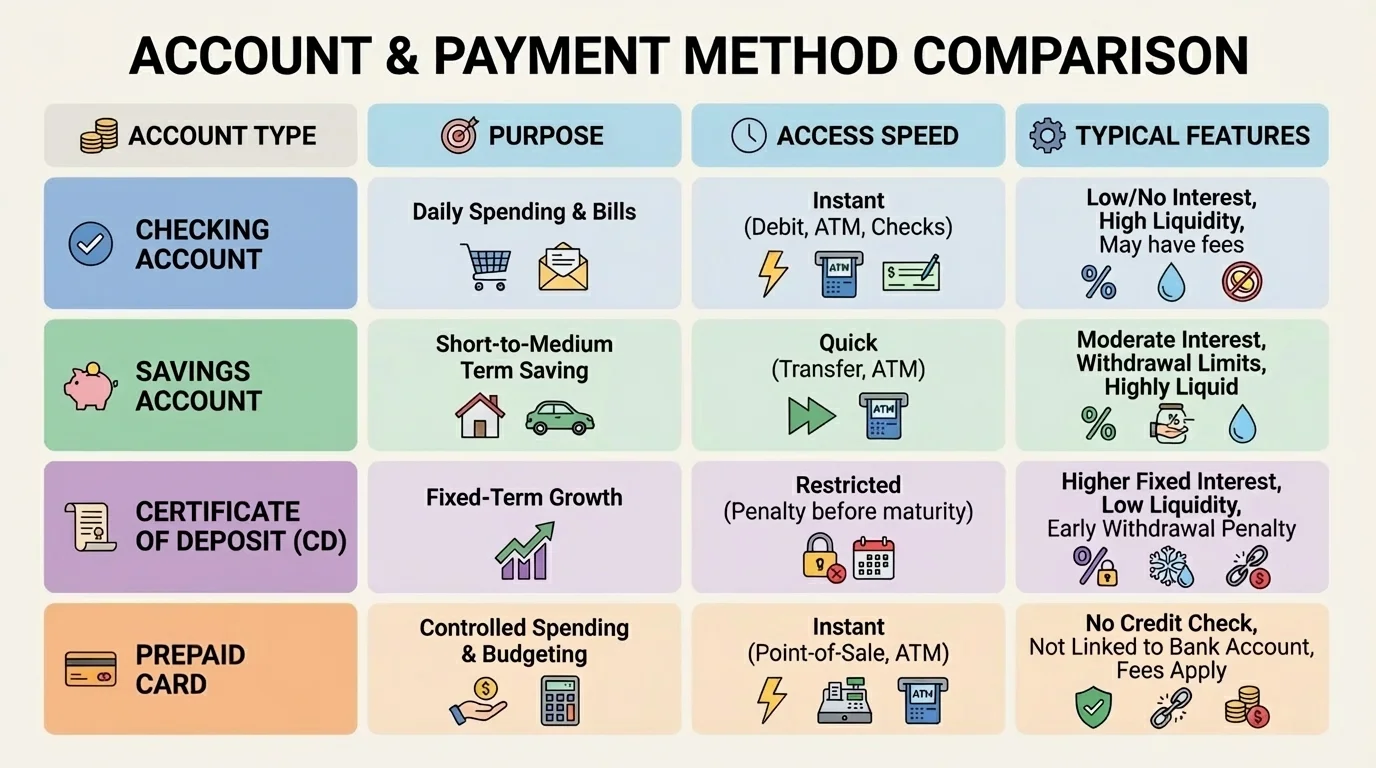

[Figure 1] Different accounts are designed for different jobs. The most common starting point is a checking account, which is built for everyday spending. It usually allows frequent deposits, withdrawals, debit card purchases, ATM use, checks, and online bill payments.

A savings account is designed for money you do not plan to spend right away. It typically pays interest, which is money the bank pays you for keeping funds there. For example, if the annual interest rate is 2%, then the interest on $500 for one year is \(500 \times 0.02 = 10\), so the account earns $10 in one year, ignoring compounding. Savings accounts help separate money for emergencies, short-term goals, or planned purchases.

Some institutions also offer money market accounts, which may combine features of checking and savings. They often pay higher interest than a basic savings account but may require a higher minimum balance. A certificate of deposit, often called a CD, locks money in for a set amount of time, such as 6 months or 12 months, in exchange for a fixed interest rate. CDs can be useful for money you are sure you will not need soon.

A prepaid card account is different from a bank account. You load money onto the card in advance, then spend only what is loaded. This can limit overspending, but prepaid cards often charge activation, reload, or monthly fees. They also may provide fewer protections than traditional bank accounts.

As students get older, they may also hear about brokerage or investment accounts. Those are used to buy assets like stocks or bonds rather than to handle everyday spending. They are important in personal finance, but they are not a substitute for a checking or savings account.

A bank and a credit union both provide accounts and payment services, but they are organized differently. Banks are for-profit businesses. Credit unions are not-for-profit cooperatives owned by members. In practice, both can offer checking accounts, savings accounts, debit cards, mobile apps, loans, and ATMs.

One major issue is insurance. Deposits at insured banks are typically protected by the FDIC insurance system, and deposits at insured credit unions are typically protected by the NCUA insurance system. This means that, within legal limits, your money is protected if the institution fails. That protection is one reason many consumers choose regulated financial institutions instead of storing large sums in cash.

Institutions also differ in fees and features. Some accounts charge monthly maintenance fees unless you meet conditions such as direct deposit, a minimum balance, or student status. Others may charge for using out-of-network ATMs, ordering checks, or overdrawing an account. Interest rates matter too. A savings account paying 0.1% grows much more slowly than one paying 4%, especially over time.

Some people choose a bank based on a branch near home, while others care more about whether the mobile app lets them deposit checks by phone, freeze a card instantly, or set spending alerts. Convenience is not just about location anymore.

Another important feature is account ownership. A teen account may be joint, meaning a parent or guardian also has access. An individual account belongs to one person. Joint accounts can help with supervision, but they also require trust because each owner may be able to make withdrawals.

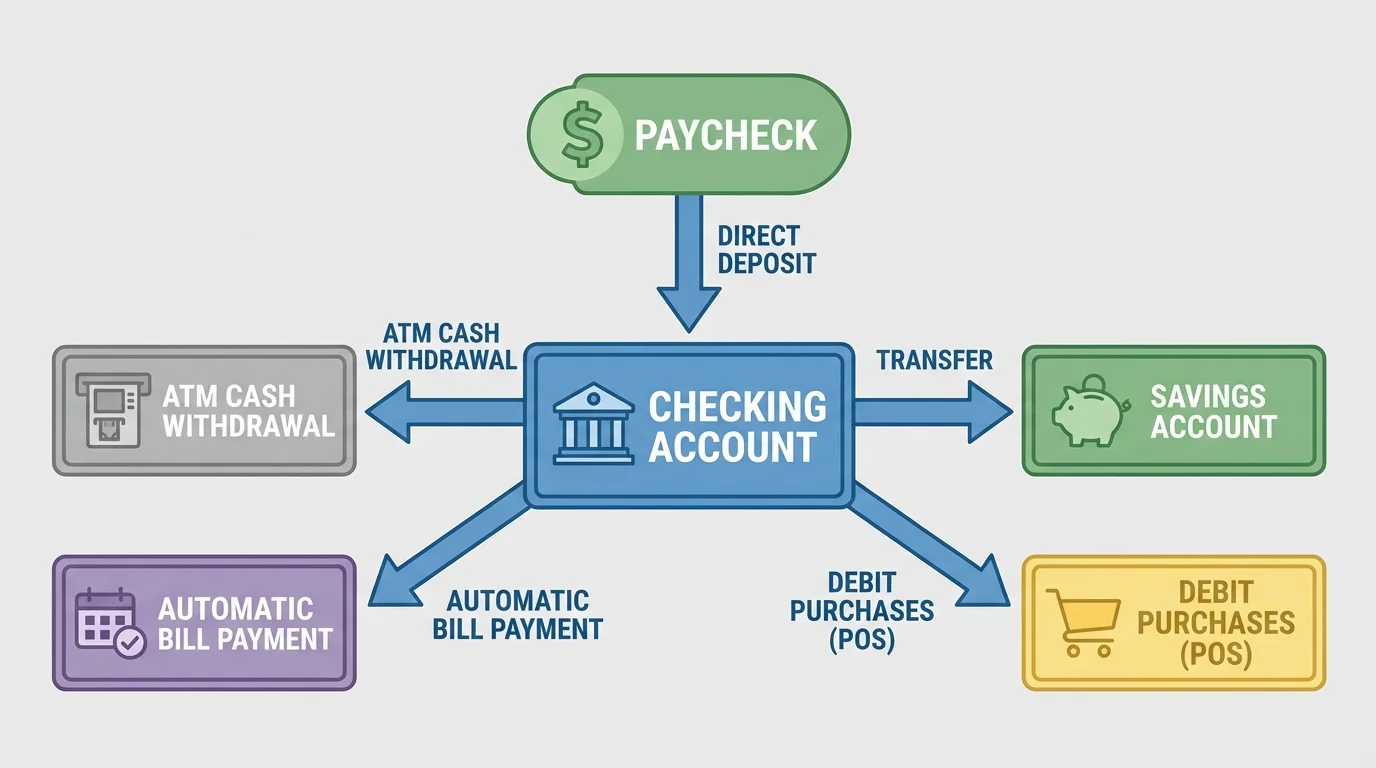

[Figure 2] Managing money well starts with understanding how money flows through deposits, transfers, purchases, and bill payments. To open an account, a person usually needs identification, personal information, and sometimes an opening deposit. Depending on age, a parent or guardian may need to be present.

Once the account is open, the first task is learning how money enters it. Money can come through cash deposits, checks, transfers, or direct deposit, which sends a paycheck electronically into an account. Direct deposit is common because it is fast and secure.

The next task is understanding how money leaves the account. Withdrawals can happen through ATM cash withdrawals, debit card purchases, electronic transfers, checks, and automatic bill payments. This is why checking the balance regularly matters. If you have $120 in your account and spend $45 on groceries, $18 on a streaming subscription, and $70 on shoes, then the total spending is \(45 + 18 + 70 = 133\). That is $13 more than the original balance, which can lead to an overdraft or a declined transaction.

Online and mobile banking tools help account holders monitor activity. A monthly statement lists deposits, payments, fees, and the ending balance. Reading statements can reveal mistakes, forgotten subscriptions, or unauthorized purchases. Many apps also allow alerts when the balance drops below a set amount, such as $50.

Transfers between accounts are another basic skill. A student might move part of each paycheck from checking to savings automatically. If a paycheck is $240 and the student transfers 20% to savings, the amount saved is \(240 \times 0.20 = 48\). That leaves $192 in checking for spending and bills. Automation makes saving more likely because it happens before the money is casually spent.

Account management is really decision management. Every account transaction reflects a choice: spend now, save for later, move money to organize goals, or borrow and repay over time. Good management means matching the account to the purpose and checking often enough to catch problems early.

Keeping records matters even when apps make payments feel invisible. A purchase can seem small in the moment, but many small charges add up. Four app purchases of $7 each, two fast-food meals costing $12 each, and one game subscription costing $15 add up to \(4 \times 7 + 2 \times 12 + 15 = 28 + 24 + 15 = 67\) dollars. That is $67 gone from the account, even though none of the individual charges looked dramatic.

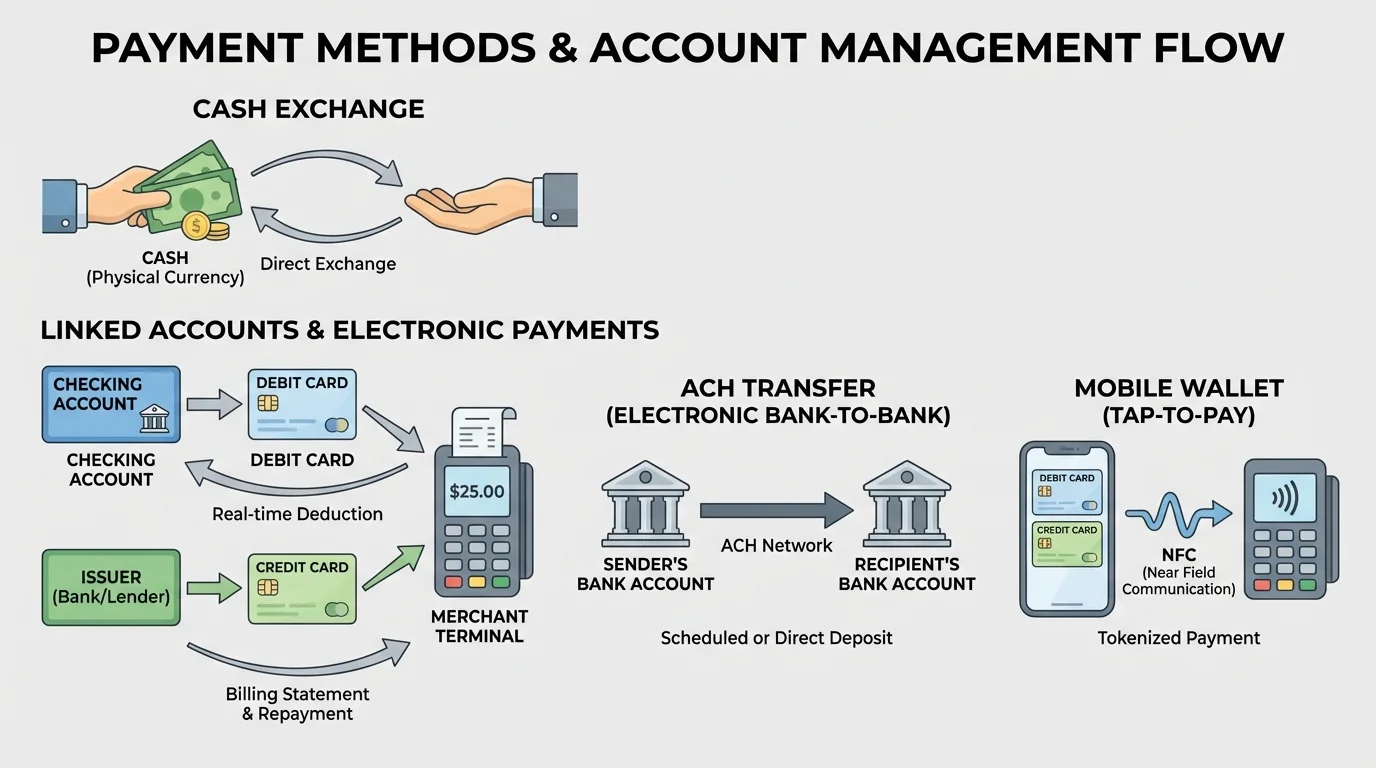

[Figure 3] Each payment method moves money differently, and each has strengths and weaknesses. Smart consumers do not use one method for everything. They choose based on the situation.

Cash is physical money. It works well for small in-person purchases and can help people stick to a spending limit because once the cash is gone, spending stops. However, cash offers little protection if lost or stolen, and it does not create an automatic record.

Debit cards take money directly from a checking account. They are useful for daily purchases and ATM access, but they require close balance monitoring. If the account does not have enough money, a transaction may be declined or may go through and trigger an overdraft fee.

Credit cards let the user borrow money up to a limit and repay later. If the full statement balance is paid by the due date, interest may be avoided during the grace period. If not, interest is charged on the unpaid balance. Suppose a person carries a $300 balance at a monthly rate of 2%. The interest for that month is \(300 \times 0.02 = 6\), so the balance becomes about $306 before any new purchases or fees.

Checks are written instructions telling a bank to pay a certain amount from an account. Checks are less common for everyday teen spending, but they are still used for some rent payments, school fees, or official transactions. A bounced check happens when the account lacks enough money, and that can cause fees from both the bank and the business.

Electronic transfers, including ACH payments, move money between accounts digitally. They are common for payroll, bill payments, and online transfers. Peer-to-peer payment apps let users send money quickly to friends or family, but they can be risky if money is sent to the wrong person because transfers may be hard to reverse.

Mobile wallets store payment information on a phone or smartwatch and allow tap-to-pay purchases. They can be convenient and secure because they often use tokenization, meaning the actual card number is not always shared directly with the merchant.

Buy now, pay later services split a purchase into several payments. These services can seem harmless, but they still create obligations. Missing a payment can lead to fees and damage budgeting plans. Splitting a $160 purchase into 4 equal payments means each payment is \(160 \div 4 = 40\), so the buyer must remember that $40 will be due repeatedly, not just once.

Gift cards and store credit can be useful for controlled spending, but they are limited to specific sellers and may carry terms or inactivity rules.

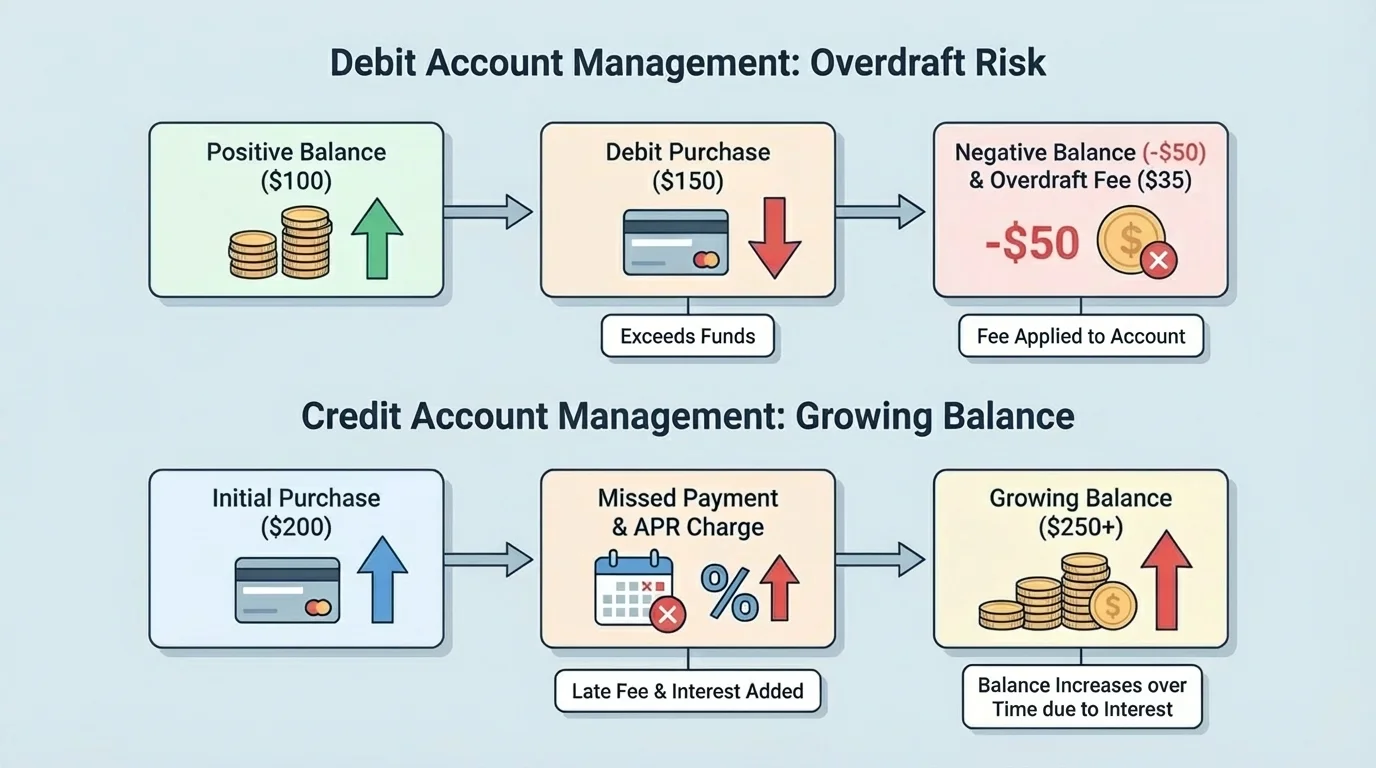

[Figure 4] Convenience can become expensive when consumers do not understand fees and protections, especially with overdrafts and growing card balances. One major risk with checking accounts is the overdraft. An overdraft happens when you spend more money than is available in the account. Some banks decline the transaction. Others cover it temporarily and charge a fee.

Suppose an account has $25 available, and a debit purchase of $40 goes through. The shortage is \(40 - 25 = 15\). If the bank charges a $35 overdraft fee, then the account may effectively have a negative balance of $50 after the purchase and fee are counted together. A small mistake becomes a large cost very quickly.

Credit cards have a different risk: debt can grow over time through the APR, or annual percentage rate. The APR helps show the yearly cost of borrowing. A high APR makes carrying balances expensive. Late payments may also add fees and hurt a person's credit history.

Fraud and identity theft are also serious concerns. If someone steals account information, they may make unauthorized purchases or transfers. Consumers should protect passwords, avoid suspicious links, and monitor account activity. Reporting suspicious charges quickly improves the chance of fixing the problem.

Different payment methods offer different protections. Credit cards usually provide strong dispute rights for unauthorized charges. Debit cards may also offer protection, but the rules can depend on how quickly the issue is reported. Cash has almost no recovery options if stolen. Peer-to-peer apps may treat mistaken transfers as the sender's responsibility.

Budgeting and account management are connected. A budget tells your money where to go before you spend it. An account shows whether your real transactions match that plan. If the two do not match, the problem is often not math but behavior.

Consumers should also understand holds and pending transactions. For example, a gas station may place a temporary hold larger than the amount actually purchased. That means the available balance can look lower than expected until the final amount posts.

A useful way to choose a payment method is to compare it across several factors: speed, safety, cost, recordkeeping, and whether it uses existing money or borrowed money. The best method depends on what matters most in that moment.

| Payment Method | Where Money Comes From | Main Advantages | Main Risks or Limits | Best Use |

|---|---|---|---|---|

| Cash | Physical money on hand | Simple, immediate, helps control spending | Can be lost, no automatic record | Small in-person purchases |

| Debit card | Checking account | Convenient, widely accepted, easy tracking | Overdraft risk, balance must be monitored | Routine spending when funds are available |

| Credit card | Borrowed money | Fraud protection, rewards, builds credit history if used well | Interest, debt, late fees | Planned purchases paid off on time |

| Check | Checking account | Useful for formal payments | Can bounce, slower processing | Rent, school fees, official transactions |

| ACH transfer | Bank account | Efficient for bills and payroll | Processing delays, possible transfer errors | Bills, direct deposit, account transfers |

| Peer-to-peer app | Linked account or card | Fast person-to-person payments | Hard to reverse mistakes, scam risk | Paying trusted people |

| Mobile wallet | Linked card or account | Fast, contactless, can improve security | Depends on device access and merchant acceptance | Everyday purchases with a phone or watch |

Table 1. Comparison of major payment methods by source of funds, benefits, risks, and common uses.

The comparison also shows why no single payment method is always best. A responsible spender may carry a debit card for ordinary purchases, keep emergency savings separate, use direct deposit for income, and use a credit card only when able to pay the statement balance in full.

Good financial habits are often quiet and repetitive rather than dramatic. They include checking balances before spending, reading statements, updating passwords, setting alerts, and keeping some money in savings. They also include asking smart questions before opening an account: Is there a monthly fee? Is there a minimum balance? What is the overdraft policy? How easy is it to talk to customer service?

One strong habit is separating money by purpose. For example, a student with $900 might keep $600 in checking for monthly expenses and $300 in savings for emergencies. If monthly spending averages $150 on transportation, $120 on food, $80 on subscriptions and entertainment, and $200 on other needs, total monthly expenses are \(150 + 120 + 80 + 200 = 550\). That means the $600 checking balance covers the month with a $50 cushion.

Real-world example: Choosing the right setup for a part-time job

Maya works after school and earns about $180 per week. She wants money for everyday spending, a concert in three months, and an emergency cushion.

Step 1: Divide money by purpose.

Maya sends her paycheck to checking, then transfers 25% to savings. The savings transfer is \(180 \times 0.25 = 45\), so $45 goes to savings and $135 stays in checking.

Step 2: Match payment methods to goals.

She uses her debit card for transportation and groceries, cash for weekend spending limits, and avoids using a credit card for impulse purchases.

Step 3: Track progress toward a goal.

After 12 weeks, the concert savings total is \(45 \times 12 = 540\) if she leaves the transfers untouched.

Because Maya uses separate accounts and planned payment methods, she is less likely to spend her concert money by accident.

Another strong habit is reviewing a payment before approving it. This matters especially with subscriptions, free trials, and online shopping. A service charging $9.99 each month costs $119.88 per year because \(9.99 \times 12 = 119.88\). What feels tiny month to month can become significant over a year.

Earlier, [Figure 1] shows that accounts serve different purposes, and that idea remains central to good budgeting. Spending money belongs in a highly accessible account, while emergency money belongs somewhere safer from impulse use. In the same way, [Figure 2] shows that money management is a flow, not a single event. Income comes in, choices are made, and every transaction changes future options.

Consider three situations. First, a student is buying a snack after practice. Cash or a debit card may be best because the amount is small and immediate. Second, a family is paying a utility bill. An ACH transfer or online bill pay may be efficient and creates a record. Third, a college student books a hotel room online. A credit card may be preferred because hotels often require one and because fraud protections can be stronger.

Now think about risk. If you send rent money through a peer-to-peer app to the wrong username, fixing the mistake may be difficult. If you lose $60 in cash, it is probably gone. If a thief uses a stolen credit card number, the charge can often be disputed. That is why understanding how the system works matters as much as understanding your own budget.

As [Figure 3] makes clear, payment methods are really pathways between consumers, businesses, and financial institutions. And as [Figure 4] shows, poor choices can create long-lasting costs through fees and debt. Financial literacy is not about memorizing definitions only. It is about making decisions that protect your money, match your goals, and reduce avoidable risk.

"The safest financial tool is the one you understand well enough to use on purpose."