Two people can invest the exact same amount of money and end up in very different financial situations. The difference is often not luck. It is usually a matter of choosing investments that fit a purpose. Someone saving for a car in two years should not invest the same way as someone saving for retirement in forty years. That is why smart investing is not about picking whatever seems exciting. It is about matching money decisions to goals, time, and risk.

Investing matters because simply saving money in cash often is not enough to build long-term wealth. Inflation causes prices to rise over time, so money that sits still can lose purchasing power. If inflation averages about 3% per year, an item that costs $100 today could cost about $103 next year. Over many years, that difference becomes much bigger. Investments are tools that can help money grow faster than inflation, although they also involve different levels of uncertainty.

Financial goal means a specific money target, such as building an emergency fund, paying for college, buying a home, or retiring comfortably. Risk tolerance is the amount of uncertainty or possible loss a person is emotionally and financially able to handle. Time horizon is the amount of time before the money will be needed. Return is the gain or loss from an investment over time.

These ideas work together. A person with a long time horizon may be able to take more risk because there is more time to recover from market drops. A person who needs money soon usually needs safer, more liquid options. An investor must also think about personal circumstances: income, family responsibilities, debt, health, and future plans all affect what makes sense.

When people talk about "good investments," they sometimes act as if there is one perfect answer. There is not. A good investment for one person may be a poor choice for another. For example, keeping all savings in a checking account is safe in the short term, but it usually offers low growth. Putting all savings into individual stocks may offer high growth potential, but it can also lead to major losses. The challenge is balance.

Think of investing like building a team for a long season. Some players are reliable and steady. Others are high-scoring but unpredictable. A successful team usually needs a mix. In finance, that mix depends on whether the goal is short-term access, long-term growth, income, or protection from loss.

The basic trade-off

In general, investments with lower risk tend to offer lower expected returns, while investments with higher risk tend to offer higher expected returns over long periods. This does not mean high-risk investments are always better. It means investors must decide how much uncertainty they are willing to accept in exchange for the possibility of growth.

A key point is that risk is not only about whether prices go down. Risk also includes the danger of not meeting a goal. For instance, if someone invests too conservatively for retirement, their money may not grow enough. So being "too safe" can also be risky when the goal is far in the future.

A time horizon strongly affects investment decisions. If money is needed in less than a year, many investors prefer cash or cash-like options because price swings could hurt them right before they need the money. If the horizon is ten, twenty, or forty years, temporary drops may matter less because there is more time for recovery and growth.

Risk tolerance has both an emotional side and a practical side. Emotionally, some people lose sleep if their account balance falls. Practically, a person with unstable income or no emergency fund may not be able to take as much risk even if they want higher returns. Risk tolerance is not about bravery. It is about being realistic.

Return can be earned in different ways. Some investments grow in value, such as stocks or real estate. Others pay income, such as bonds paying interest or some stocks paying dividends. Total return includes all gains, whether from price increases, income payments, or both.

Another major factor is liquidity, which means how quickly an investment can be converted to cash without losing much value. A savings account is very liquid. Real estate is much less liquid because selling property takes time and money. Liquidity matters most for emergency savings and short-term goals.

A small difference in annual return can lead to a huge difference over time because of compounding. Money that earns returns can begin earning returns on earlier returns, not just on the original amount.

Compound growth is one of the most powerful ideas in personal finance. If $1,000 grows at 7% per year, after one year it becomes $1,070. After the second year, growth is based on $1,070, not just the original $1,000. That gives approximately $1,144.90 because \(1,070 \times 1.07 = 1,144.90\). Over a long period, compounding can make time more important than the size of a single deposit.

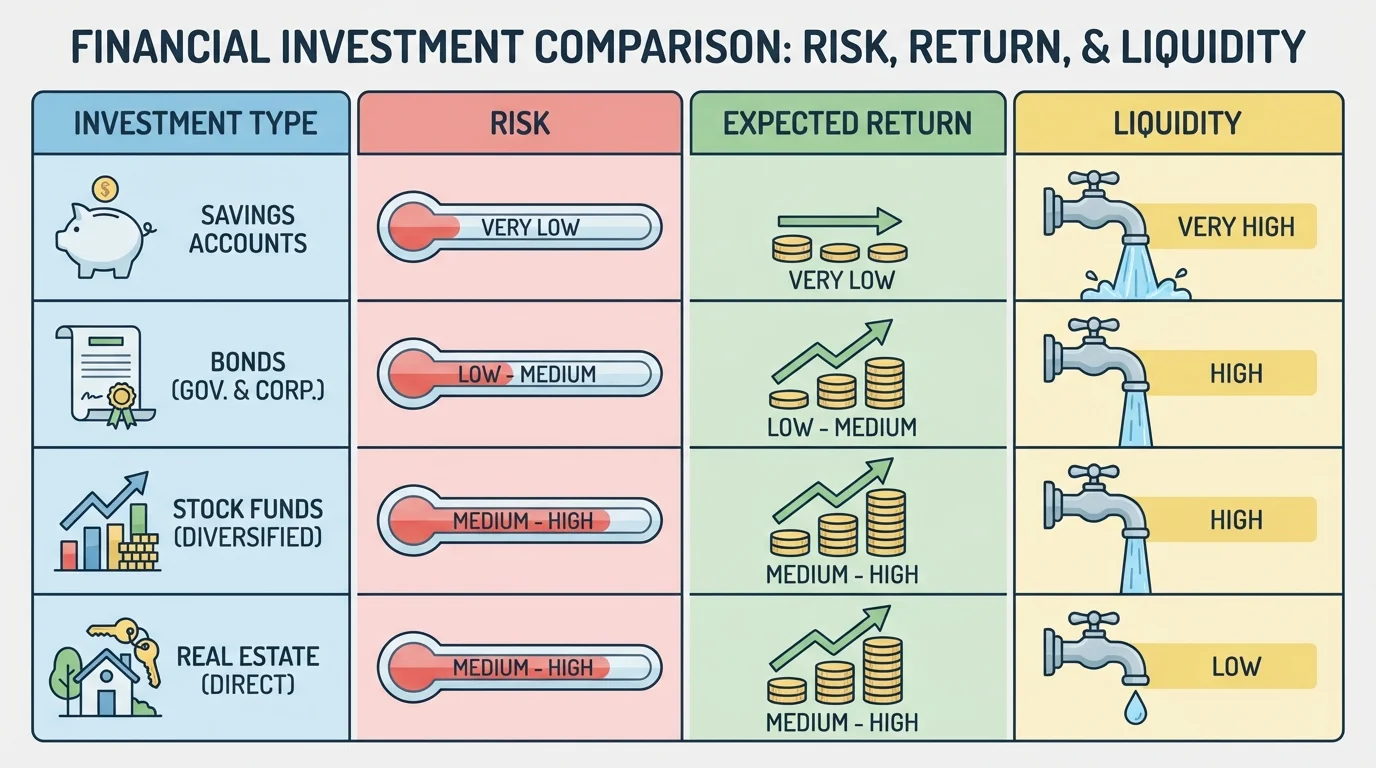

Investment choices exist on a spectrum, as [Figure 1] shows, from safer options with lower expected returns to riskier options with greater growth potential. Understanding the basic categories helps investors choose tools that fit their needs instead of reacting to trends or advertisements.

Cash and cash equivalents include checking accounts, savings accounts, and money market accounts. These are useful for emergency funds and short-term goals because they are stable and liquid. However, they usually have lower returns, so they are not ideal for long-term growth by themselves.

Bonds are loans that investors make to governments or corporations. In return, the issuer promises to pay interest and return the original amount later. Bonds are often less volatile than stocks, but they still carry risk. For example, interest rates can affect bond prices, and some issuers may fail to repay.

Stocks represent ownership in a company. If the company grows and becomes more profitable, the stock may rise in value. Stocks have historically offered strong long-term growth, but their prices can change quickly. Owning one or two individual stocks is usually riskier than owning many through a fund.

Mutual funds and ETFs bundle many investments together. A stock mutual fund or ETF may hold shares in hundreds of companies. This makes them popular because they help with diversification. ETFs are traded on exchanges like stocks, while mutual funds are typically bought and sold through the fund company at the end of the trading day.

Real estate can include buying property directly or investing through real estate investment trusts. Real estate can provide rental income and possible price growth, but it may require more money, maintenance, and patience. It also is not as easy to sell quickly as stocks or bonds.

Retirement accounts are not a separate asset by themselves. Instead, they are accounts that can hold investments such as stock funds, bond funds, or target-date funds. The account type affects taxes and withdrawal rules.

As seen earlier in [Figure 1], no single investment wins in every category. Savings accounts offer stability and liquidity, while stock funds offer stronger long-term growth potential. Investors usually combine types instead of choosing only one.

Comparing short-term and long-term goals

Suppose Jordan wants $4,000 for a car in two years, while Maya wants to invest for retirement in forty-five years.

Step 1: Identify the time horizon.

Jordan has a short horizon of about 2 years. Maya has a long horizon of about 45 years.

Step 2: Match the need to the investment style.

Jordan may prefer safer, more liquid choices such as savings or short-term bonds because a market drop right before the purchase would be a major problem. Maya can usually accept more stock exposure because there is more time for recovery and compounding.

Step 3: Explain why the same investment does not fit both goals.

A risky stock portfolio might grow quickly, but Jordan cannot wait decades if the market falls. A very conservative account protects Jordan better, while Maya may need more growth to outpace inflation over many years.

The best investment depends on the goal, not on what is most exciting.

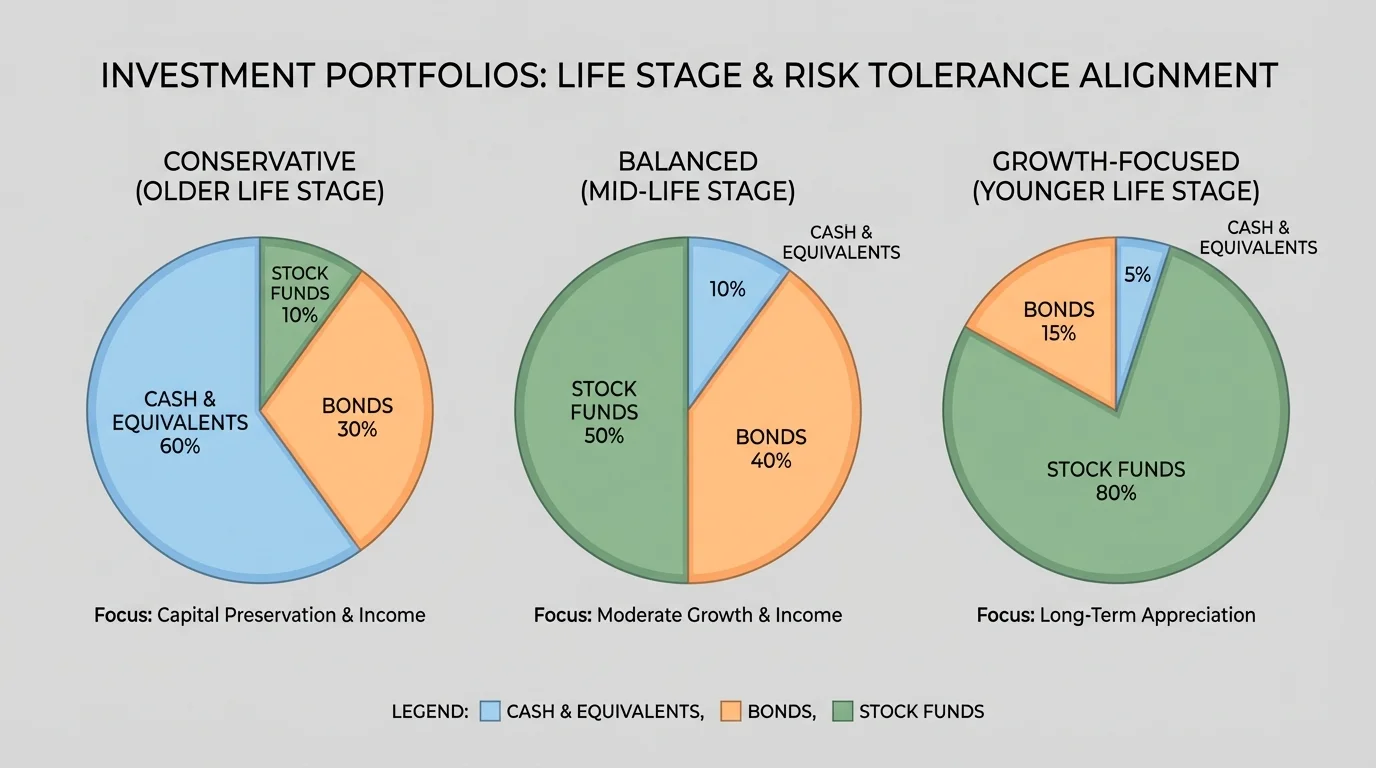

[Figure 2] Diversification means spreading money across different investments so that one weak area does not damage the entire portfolio. This is one reason many investors use broad mutual funds or ETFs. A diversified portfolio may include a mix of cash, bonds, and stock funds instead of depending on one company or one asset type.

Asset allocation is the percentage of a portfolio placed in different categories, such as stocks, bonds, and cash. A person with a high need for growth may place more in stock funds. A person who needs stability and income may put more in bonds and cash.

Diversification does not guarantee profits or prevent all losses. If the entire market falls, a diversified portfolio can still lose value. But diversification can reduce the damage caused by a problem in one company, one industry, or one type of investment.

Students sometimes think diversification means owning many things randomly. It does not. Owning ten different social media companies is not very diversified if all of them are affected by the same trend. Real diversification spreads risk across different sectors, asset types, and sometimes different countries.

| Portfolio style | Typical goal | Possible mix | Main trade-off |

|---|---|---|---|

| Conservative | Protect money, short or medium horizon | More cash and bonds, fewer stocks | Lower risk, lower growth |

| Balanced | Mix growth and stability | Moderate stocks, bonds, some cash | Moderate risk, moderate growth |

| Growth-focused | Long-term growth | Mostly stock funds, fewer bonds and cash | Higher risk, higher growth potential |

Table 1. Common portfolio styles and the trade-offs between stability and growth.

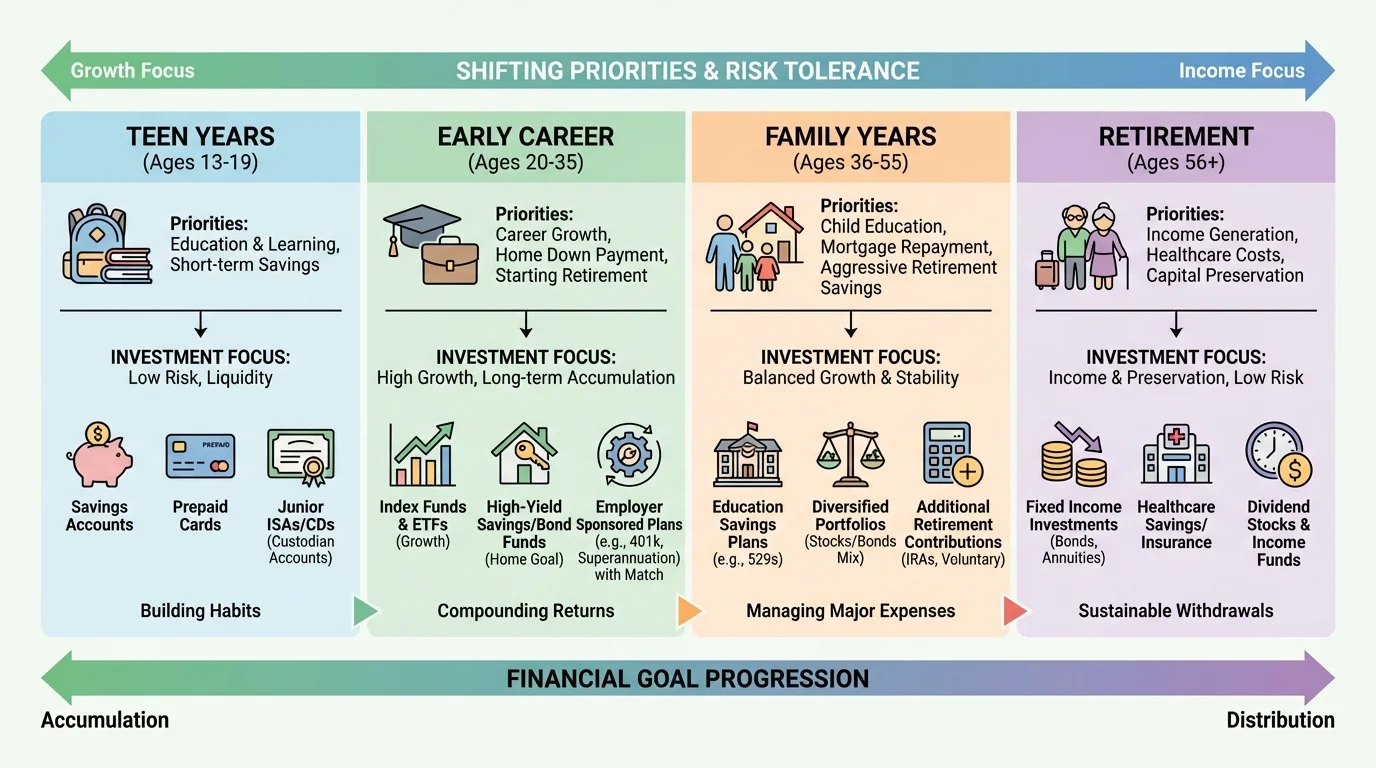

As [Figure 3] shows, investment strategy changes over time because life changes over time. Goals, responsibilities, and time horizons shift from the teen years to retirement. A strong plan adjusts to those changes instead of remaining fixed.

For teenagers and young adults, the first priorities are often building saving habits, creating an emergency fund, avoiding high-interest debt, and beginning to invest early if possible. At this stage, the biggest financial advantage is time. Even small amounts invested early can grow significantly because of compounding.

In the early career stage, a person may begin full-time work and gain access to employer retirement plans. This is often a good time to invest more for long-term goals because retirement may still be decades away. Many people at this stage can accept more stock exposure, especially if they also have an emergency fund.

During the family and mid-career stage, financial goals may multiply. A person might save for a home, children's education, emergencies, and retirement at the same time. Because some goals are short-term and others are long-term, one account may not fit all needs. Money for a home down payment in three years may need safer investments, while retirement money may still be invested for growth.

In the pre-retirement stage, protecting accumulated savings becomes more important. Many investors begin reducing risk gradually by increasing bond or cash exposure, though they may still keep stocks for growth because retirement can last decades. The point is not to eliminate all risk but to lower the chance of a severe loss right before or just after retirement.

In retirement, the focus often shifts toward income, stability, and careful withdrawal planning. Retirees may use a mix of bonds, dividend-paying stock funds, and cash reserves to cover living expenses while still maintaining some growth to keep up with inflation.

The timeline in [Figure 3] makes an important pattern visible: younger investors often emphasize growth, while older investors usually move toward a more balanced or conservative mix. However, age alone does not decide everything. Health, family support, pension income, and personal comfort with risk matter too.

Before investing, basic financial security still comes first. An emergency fund and a plan to manage debt help protect investors from being forced to sell investments at a bad time.

People can invest through different kinds of accounts. Some are regular personal accounts, often called taxable brokerage accounts. These are flexible because money can usually be added or withdrawn at any time, though investment gains may be taxed.

Retirement accounts are designed to encourage long-term saving. An employer-sponsored plan may allow automatic contributions from each paycheck. Sometimes employers offer matching contributions. If an employer matches part of an employee's contribution, that match is often considered one of the most valuable benefits because it increases the amount invested.

Individual retirement accounts, or IRAs, are another option. The exact tax rules vary, but the main idea is that retirement accounts can provide tax advantages either when money goes in, while it grows, or when it is withdrawn later. In exchange, these accounts usually have rules about when money can be taken out without penalties.

Target-date funds are common in retirement accounts. These funds automatically adjust their asset allocation over time. A fund designed for someone retiring far in the future may hold more stocks now and gradually shift toward more bonds as the target year approaches. For people who want a simple, diversified option, target-date funds can be useful.

Why taxes matter in investing

Taxes can reduce how much of an investment return an investor keeps. That means the type of account matters, not just the investment inside it. A tax-advantaged retirement account may allow more growth to remain invested over time, which can increase long-term results.

Personal and retirement options should fit the goal. A student saving for college expenses in a few years may need more flexibility than a worker saving for retirement in forty years. A household may use both: regular accounts for medium-term goals and retirement accounts for long-term goals.

When comparing investments, ask several questions. What is the goal? When will the money be needed? How much loss can be tolerated? How easily can the investment be sold? What fees or taxes apply? These questions often matter more than recent headlines.

Fees are especially important because even small percentages can reduce long-term growth. If one fund charges 1% per year and another similar fund charges 0.1% per year, the lower-cost option may leave more money invested over time. A difference that seems tiny in one year can become large over decades.

Inflation should also be considered. If an investment earns 4% in a year while inflation is 3%, the investor's real increase in purchasing power is only about 1%. That idea can be estimated by subtracting inflation from the nominal return: \(4\% - 3\% = 1\%\). This is a simple estimate, but it helps show why low-growth options may not be enough for long-term goals.

Compound growth example

A student invests $2,000 and it grows at 6% per year for 5 years.

Step 1: Write the compound growth formula.

Use \[A = P(1 + r)^t\]

Here, \(P = 2,000\), \(r = 0.06\), and \(t = 5\).

Step 2: Substitute the values.

\(A = 2,000(1.06)^5\)

Step 3: Calculate the growth factor.

\((1.06)^5 \approx 1.3382\)

Step 4: Find the final amount.

\(A \approx 2,000 \times 1.3382 = 2,676.40\)

After 5 years, the investment is worth approximately $2,676.40.

This example helps explain why starting early matters. If the same money stays invested longer, compounding has more time to work. That is one reason younger investors may benefit from beginning with even modest amounts.

One common mistake is chasing returns, which means buying whatever has recently gone up the most. By the time everyone is excited about an investment, its price may already be high. Another mistake is putting too much money into one company, one cryptocurrency, or one hot trend. That creates concentration risk.

A third mistake is ignoring personal goals. An investment is not "bad" because it grows slowly if it is serving a short-term need for stability. Likewise, an investment is not "good" just because it had a big return last year if it exposes someone to more risk than they can handle.

Smart habits include investing regularly, reviewing goals, keeping costs low, staying diversified, and avoiding emotional decisions during market swings. Automatic contributions can be especially powerful because they turn investing into a routine rather than a reaction.

"Do not save what is left after spending, but spend what is left after saving."

— Warren Buffett

This idea connects to long-term investing because regular saving creates the money that can later be invested. Even the best investment strategy cannot work without consistent contributions.

The following scenarios show how similar amounts of money can lead to different investment choices depending on the person's goals and stage of life.

Case study: high school student with part-time income

Ana is 16 and has $1,500 from a part-time job. She wants to keep $800 available for emergencies and future school expenses, but she does not need the remaining $700 for many years.

Step 1: Separate short-term and long-term money.

The $800 should stay in a safe, liquid place such as a savings account.

Step 2: Match the long-term money to the long horizon.

The $700 could go into a diversified stock fund through an eligible custodial or youth account if available, because the horizon is long and the amount is not needed soon.

Step 3: Explain the strategy.

Ana is not choosing between saving and investing. She is using both for different goals.

This is a balanced approach for someone just starting out.

Ana's plan shows that investing is not all-or-nothing. Students often think they must choose either total safety or total risk. In reality, different buckets of money can have different jobs.

Case study: new worker with retirement access

Marcus is 24, has steady income, and his employer matches retirement contributions up to 4% of salary.

Step 1: Identify the opportunity.

If Marcus contributes 4% of his salary, he receives the full employer match.

Step 2: Choose a suitable investment inside the account.

Because Marcus is young and retirement is far away, he may prefer a diversified stock-heavy fund or a target-date retirement fund.

Step 3: Consider risk and time.

Marcus can usually handle more short-term fluctuation because he has decades before retirement.

The employer match makes this option especially valuable for long-term investing.

Near retirement, the decision changes. Someone with a large retirement account who plans to stop working in three years may choose to reduce stock exposure gradually. That does not mean moving everything to cash. It means aligning investments with the need for stability and future withdrawals.

Inflation and real growth example

Suppose an investment earns 5% in one year and inflation is 2%.

Step 1: Find the nominal return.

The nominal return is 5%.

Step 2: Estimate the real return.

Real return \(\approx 5\% - 2\% = 3\%\).

Step 3: Interpret the result.

The investment grew, but purchasing power increased by only about 3%, not the full 5%.

This is why long-term investors often seek growth above inflation, not just growth by itself.

By combining goals, risk tolerance, time horizon, diversification, and account type, investors can make decisions that are more thoughtful and more realistic. The goal is not to predict every market move. The goal is to build a strategy that fits a real life.