Two people can buy the same pair of shoes, pay the same sales tax at the cash register, and yet experience that tax very differently. For one person, it may feel minor. For another, it may take a painful share of a weekly budget. That surprising difference is one reason economists care not just about how much tax is collected, but what kind of tax a government uses.

Taxes are one of the most powerful tools governments have in a mixed economy. They raise money for roads, schools, police, parks, defense, and health programs. They also shape behavior. A tax on cigarettes can discourage smoking. A tax break for solar panels can encourage clean energy. Because taxes affect both households and businesses, they help determine prices, wages, spending, saving, investment, and the distribution of income.

In a mixed economy, markets do much of the work of producing and distributing goods and services, but governments also step in where markets alone may not create the outcomes society wants. Taxes provide the revenue needed for public goods and services, including things that private markets may underproduce, such as street lighting, national defense, and some infrastructure.

Taxes also support redistribution, which means shifting purchasing power or resources through government policy. For example, tax revenue may fund unemployment benefits, food assistance, or public education. Some tax systems are designed so that people with greater ability to pay contribute a larger share. Others focus more on simplicity or economic incentives.

Tax is a required payment to a government. The tax base is whatever is being taxed, such as income, property, purchases, or profits. The tax burden is the economic weight of the tax: how much a person, household, or business actually gives up because of it.

Economists also study who really pays a tax after market adjustments. A tax may be collected from a business, but part of the cost might be passed on to consumers through higher prices or to workers through lower wages. This idea matters because tax policy influences both producers and consumers, not just the group that physically sends money to the government.

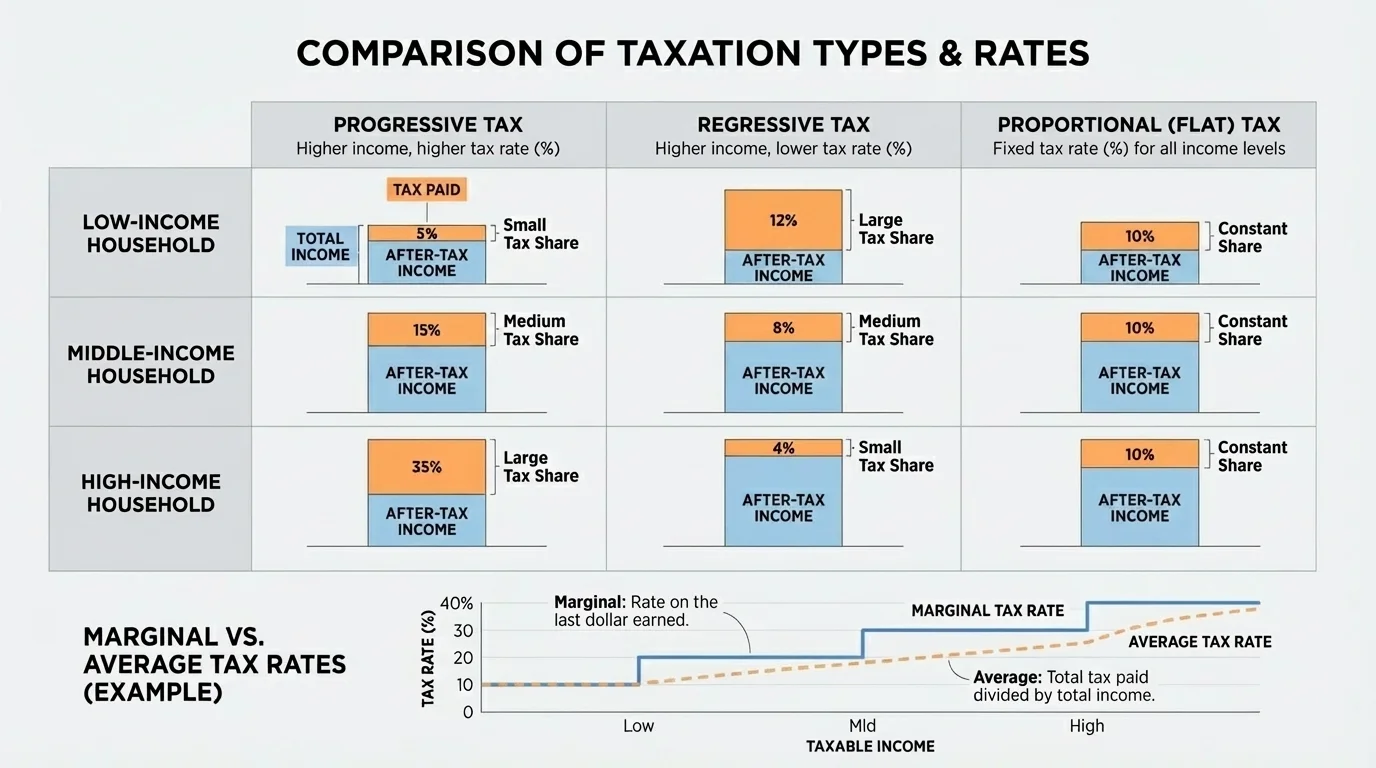

A progressive tax takes a larger percentage of income as income rises. A regressive tax takes a larger percentage of income from lower-income people than from higher-income people. A proportional tax, sometimes called a flat tax, takes the same percentage from all taxpayers.

These categories describe patterns, not moral judgments by themselves. A tax system can be progressive in one part and regressive in another. For instance, a country might have a progressive income tax but also rely heavily on sales taxes that are more regressive. That means economists often examine the overall tax structure, not just one tax in isolation.

The difference among these tax types becomes easier to see when you compare how the tax burden changes as income rises, as [Figure 1] shows. The key question is not simply, "Who pays more dollars?" Higher-income people often pay more dollars under almost any system. The more revealing question is, "What percentage of income do they pay?"

With a progressive tax, the percentage paid rises as income rises. With a regressive tax, the percentage paid falls as income rises. With a proportional tax, the percentage stays constant. That is why economists often compare tax systems using shares or rates instead of just total dollars collected.

Progressive taxes are commonly defended on the basis of ability to pay. The argument is that losing $1,000 affects a low-income household much more strongly than losing $1,000 affects a high-income household. Progressive taxation is often connected to goals such as reducing inequality and funding public services in a way many people consider fairer.

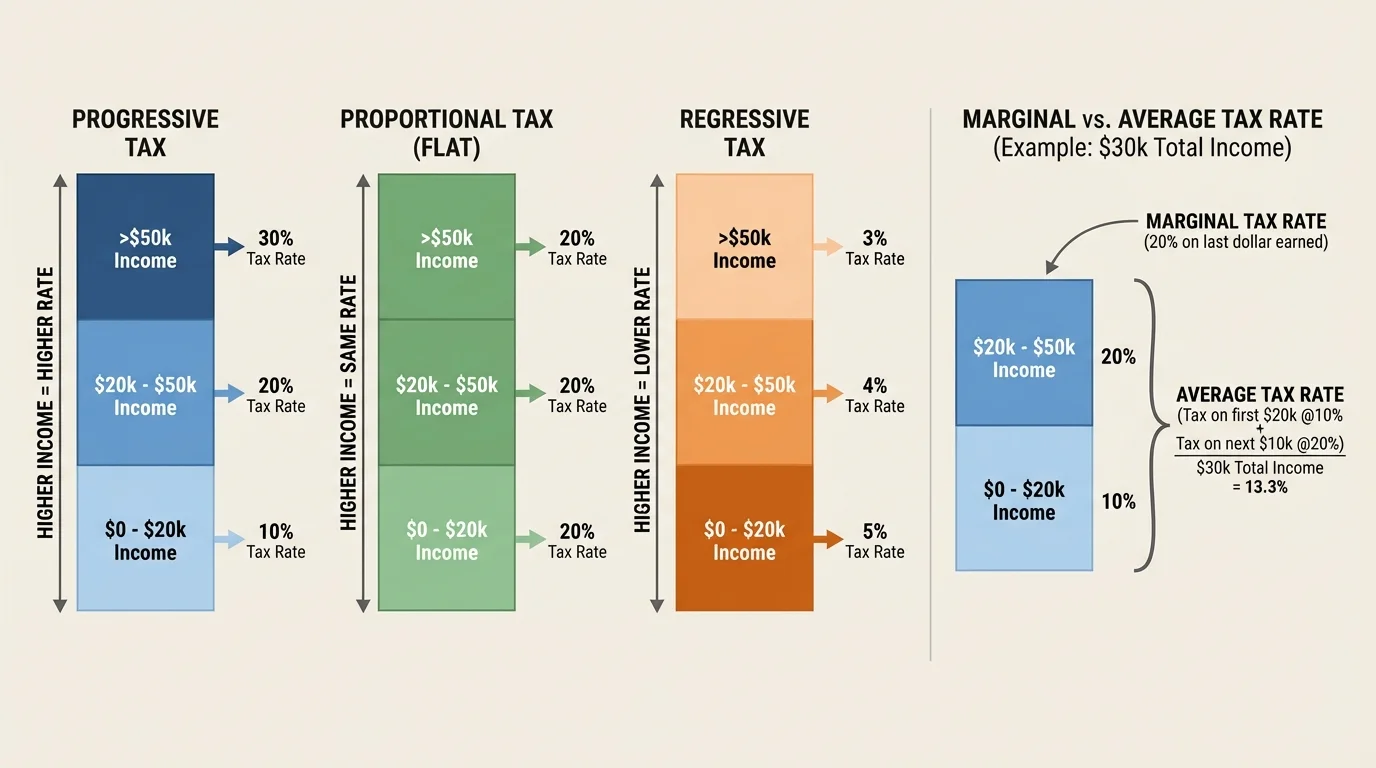

A classic example is an income tax system with brackets. If income rises from $20,000 to $200,000, the share paid in taxes may rise as well. This does not always mean the system is highly progressive; it simply means higher-income earners pay a higher percentage. Later, when we examine [Figure 2], we will see that progressive systems often rely on bracketed marginal rates.

Regressive taxes often appear in everyday life through sales taxes, payroll taxes up to a limit, and excise taxes on specific goods like gasoline, tobacco, or soda. A sales tax charges the same rate on a purchase no matter who buys the product, but lower-income households usually spend a larger fraction of their income on consumption. As a result, the tax takes up a bigger share of their total income.

For example, if two families each spend $200 on school supplies and pay a sales tax of 5% on that purchase, both owe $10 in tax. But if one family earns $20,000 and the other earns $200,000, that same $10 represents a much larger share of the first family's income. That is why many economists classify general sales taxes as regressive, even though the rate at the register is the same for everyone.

Proportional taxes apply the same percentage to everyone's taxable income. Suppose every taxpayer pays 10% of income. A person earning $30,000 pays $3,000, and a person earning $100,000 pays $10,000. The dollar amounts differ, but the percentage remains 10% for each person.

Supporters of proportional taxes often say they are simple, transparent, and may reduce distortions in work and investment decisions. Critics argue that equal percentages do not necessarily mean equal sacrifice. If essentials like rent, food, and transportation already consume much of a low-income household's budget, then paying the same percentage can still feel less fair than a progressive system.

Many real tax systems are hybrids. A country may use progressive income taxes, regressive sales taxes, property taxes, and business taxes all at the same time, which is why economists analyze the full tax mix rather than only one rule.

One useful way to compare systems is to ask what happens as income rises. In a progressive system, tax share rises. In a regressive system, tax share falls. In a proportional system, tax share stays the same. That simple comparison helps explain why the same law can be viewed differently by different groups of consumers and producers.

A major source of confusion in public debates is the difference between the marginal tax rate and the average tax rate. As [Figure 2] illustrates, a bracketed tax system does not tax all income at the highest rate someone reaches. Instead, different portions of income are taxed at different rates.

The marginal tax rate is the rate paid on the next dollar earned. The average tax rate is total tax paid divided by total income. These are related, but they are not the same.

Why the distinction matters

If a student hears that someone is "in the 22% bracket," it is easy to assume that all of that person's income is taxed at 22%. In reality, only the top portion of income in that bracket is taxed at that rate. The lower portions are taxed at lower rates. That is why the average tax rate is usually lower than the top marginal tax rate in a progressive bracket system.

The formula for average tax rate is:

\[\textrm{Average tax rate} = \frac{\textrm{Total tax paid}}{\textrm{Total income}}\]

The marginal tax rate depends on the bracket that applies to the next dollar earned. If the next dollar falls into a 22% bracket, then the marginal tax rate is 22%, even if the taxpayer's average rate is much lower.

This distinction affects decisions. A worker considering overtime may focus on the marginal rate because it affects the tax on additional earnings. A policymaker comparing fairness across households may look more closely at average tax rates. Businesses also care about marginal rates because those rates can influence hiring, investment, and expansion decisions.

Now let's compare tax systems using actual numbers. These examples show how economists turn ideas about fairness and incentives into measurable outcomes.

Example 1: Comparing progressive, proportional, and regressive tax burdens

Suppose Household A earns $25,000 and Household B earns $100,000.

Step 1: Proportional tax at 10%

Household A pays $2,500 because 10% of $25,000 is $2,500.

Household B pays $10,000 because 10% of $100,000 is $10,000.

Both households pay the same share of income: 10%.

Step 2: Progressive tax example

Suppose Household A pays 8% of income and Household B pays 15% of income.

Household A pays $2,000.

Household B pays $15,000.

The higher-income household pays both more dollars and a larger percentage of income.

Step 3: Regressive tax example

Suppose Household A pays 12% of income and Household B pays 6% of income.

Household A pays $3,000.

Household B pays $6,000.

Household B still pays more dollars, but Household A gives up a larger share of income.

The key comparison is the percentage, not just the dollar amount.

Notice something important: a tax can be regressive even if richer households pay more total dollars. Regressivity is about the share of income, not who writes the bigger check.

Example 2: Calculating total tax, marginal tax rate, and average tax rate

Suppose a tax system works like this:

\[\begin{array}{l} \textrm{First } \$10{,}000 \textrm{ taxed at } 10\% \\ \textrm{Next } \$20{,}000 \textrm{ taxed at } 15\% \\ \textrm{Any income above } \$30{,}000 \textrm{ taxed at } 25\%\end{array}\]

A worker earns $50,000.

Step 1: Tax the first bracket

The first $10,000 is taxed at 10%, so the tax is $1,000.

Step 2: Tax the second bracket

The next $20,000 is taxed at 15%, so the tax is $3,000.

Step 3: Tax the remaining income

The remaining income is $20,000 because \(\$50{,}000 - \$30{,}000 = \$20{,}000\).

That amount is taxed at 25%, so the tax is $5,000.

Step 4: Find total tax

Total tax is \(\$1{,}000 + \$3{,}000 + \$5{,}000 = \$9{,}000\).

Step 5: Find average tax rate

\[\frac{9{,}000}{50{,}000} = 0.18 = 18\%\]

The worker's marginal tax rate is 25% because the next dollar earned falls in the top bracket. The average tax rate is 18%.

This is why entering a higher tax bracket does not mean all of your income is suddenly taxed at that top rate. The bracket applies only to the income within that range, as shown earlier in [Figure 2].

Example 3: Average tax rate from a sales tax

Suppose a city has a sales tax of 8%. Student X has annual income of $15,000 and spends $12,000 on taxable goods. Student Y has annual income of $60,000 and spends $24,000 on taxable goods.

Step 1: Find tax paid by Student X

\[0.08 \times 12{,}000 = 960\]

Student X pays $960 in sales tax.

Step 2: Find tax paid by Student Y

\[0.08 \times 24{,}000 = 1{,}920\]

Student Y pays $1,920 in sales tax.

Step 3: Compare as a share of income

Student X's average tax burden from this sales tax is

\[\frac{960}{15{,}000} = 0.064 = 6.4\%\]

Student Y's average tax burden from this sales tax is

\[\frac{1{,}920}{60{,}000} = 0.032 = 3.2\%\]

Even though Student Y pays more dollars, Student X pays a larger share of income. That is why sales taxes are often described as regressive.

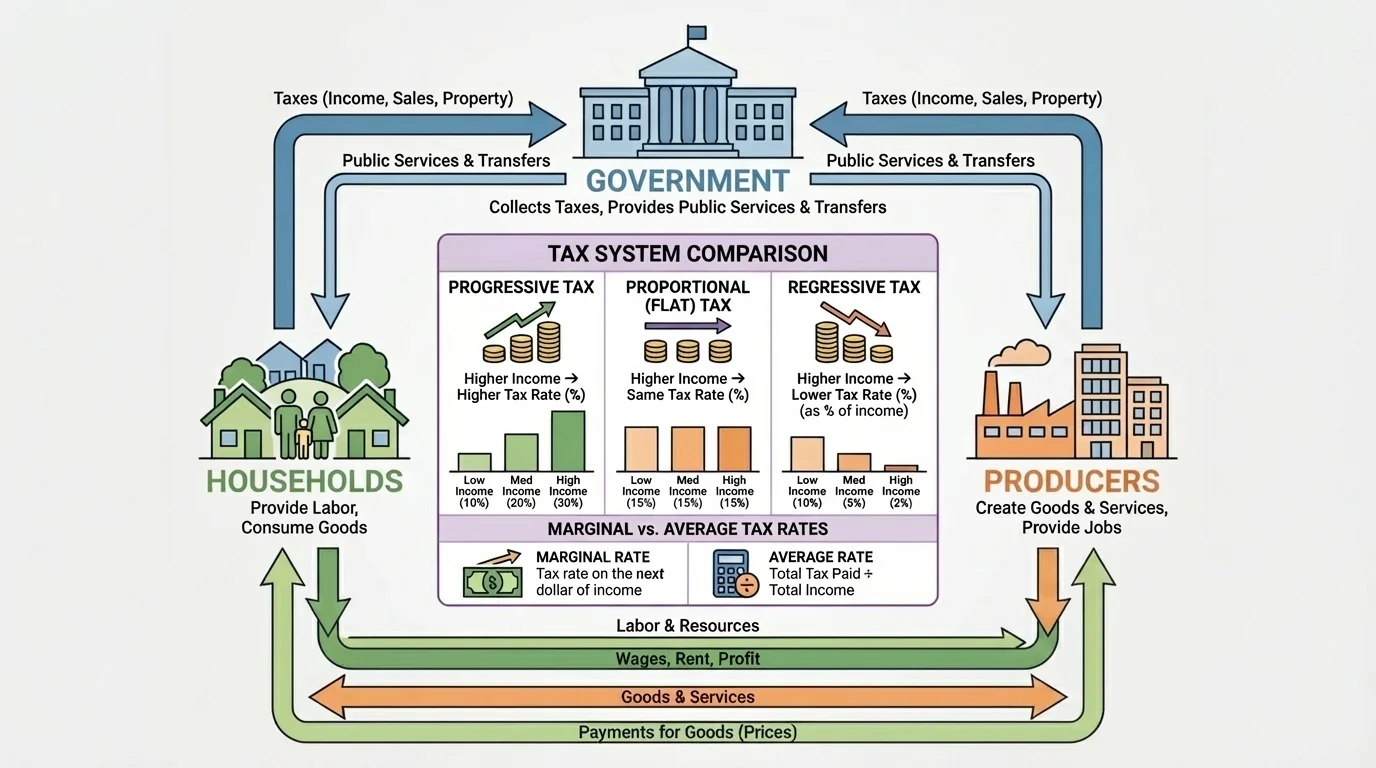

Tax policy is part of how mixed economies balance private decision-making with public goals, and [Figure 3] shows that taxes connect households, firms, and government in a continuous flow. Consumers earn income from work, spend money on goods and services, and pay taxes. Producers hire workers, invest in equipment, sell products, and pay business-related taxes. The government then uses revenue to provide services and influence economic behavior.

Taxes can change market outcomes in several ways. If a government raises a sales tax on a product, the final price consumers face may increase. That can reduce quantity demanded. If a government taxes corporate profits heavily, firms may have less incentive to invest, though the exact effect depends on many factors, including competition, access to capital, and expected demand. If government uses tax revenue to improve transportation or education, firms may actually benefit from a more productive economy.

In competitive markets, taxes are often shared between buyers and sellers. If demand is very strong and consumers are not sensitive to price, businesses may pass more of the tax on to buyers. If consumers can easily switch products, firms may absorb more of the tax themselves. This is one reason economists distinguish between who is legally responsible for paying a tax and who actually bears the burden.

Government policy can also use taxes to address externalities, which are costs or benefits that affect people outside a market transaction. For example, a tax on pollution can make producers account for environmental damage that would otherwise be ignored by the market price. In that case, taxation is not only about revenue; it is also about changing incentives so market outcomes better reflect social costs.

On the other hand, taxes can create tradeoffs. High taxes may discourage work, saving, or entrepreneurship in some situations. Very low taxes may leave governments unable to fund the public goods and safety nets that support long-term growth and social stability. Tax policy is therefore a balancing act between equity and efficiency.

One debate centers on equity, or fairness. Supporters of progressive taxes argue that people with higher incomes can contribute a larger share without severe hardship. Critics sometimes respond that highly progressive systems may reduce incentives to earn more, invest, or start businesses. The disagreement is not only about numbers; it is also about values.

Another debate involves simplicity. Proportional taxes are often praised for being easy to understand and administer. Progressive systems can be more complicated because of multiple brackets, deductions, exemptions, and credits. Yet many people accept complexity if it better matches their sense of fairness or allows policy to target specific goals.

Regressive taxes are controversial because they tend to hit lower-income households harder as a share of income. Still, governments often use them because they are relatively easy to collect and can provide stable revenue. Sales taxes, for example, are gathered in many small transactions throughout the economy. To reduce their regressive effect, some governments exempt essentials such as groceries or medicine.

The choices governments make affect daily life in visible ways. Taxes influence the price of gasoline, the cost of online purchases, take-home pay on a paycheck, and the amount of funding available for schools, transit, parks, and public health. For producers, taxes affect profit margins, hiring decisions, and location choices. For consumers, taxes affect what goods are affordable and how much income remains after required payments.

When evaluating any economic policy, ask two questions: Who pays? and How do incentives change? Those questions are central to understanding why the same tax can help achieve one goal while creating a new tradeoff somewhere else in the economy.

As the systems compared earlier in [Figure 1] make clear, the structure of taxation matters just as much as the amount collected. And as the flow among households, firms, and government in [Figure 3] shows, taxes are not isolated rules on paper. They shape market outcomes across the whole economy.