A single economic crisis can close businesses, erase jobs, shake stock markets, and change what families buy almost overnight. What makes the topic especially important is that governments are not just spectators when this happens. In a mixed economy, they can act as a rule-maker, spender, lender, employer, regulator, and safety net all at once. That combination of roles means government decisions can shape whether a crisis gets shorter or deeper, fairer or more unequal, and whether markets recover quickly or stay damaged for years.

An economic crisis is a period of severe disruption in normal economic activity. It may involve a recession, which is a significant decline in output and employment, or even a depression, which is longer and more severe. A crisis can also center on inflation, a sustained rise in the general price level, or a financial breakdown in banks and credit markets. When crisis conditions spread, households cut spending, businesses delay hiring, and investors become cautious. Because one person's spending is another person's income, these problems can reinforce each other.

Economists often describe total spending in the economy with the equation \[GDP = C + I + G + (X - M)\] where household consumption is represented by \(C\), business investment by \(I\), government spending by \(G\), exports by \(X\), and imports by \(M\). During a crisis, \(C\) and \(I\) often fall sharply. Governments may then try to support demand by changing \(G\), influencing borrowing, or reducing taxes.

Economic crisis is a period when major parts of the economy are under stress, such as falling production, rising unemployment, financial instability, or fast-rising prices.

Unemployment means people who are able and willing to work cannot find jobs.

Inflation is a sustained increase in the general level of prices over time.

For students, these events may sound abstract, but they affect daily life directly. Families may postpone buying cars, restaurants may see fewer customers, schools may face budget cuts, and workers may lose hours or jobs. At the same time, some industries may grow because crisis responses create new needs. During a health emergency, for example, production may shift toward medical supplies, vaccine research, and delivery services.

A mixed economy combines market activity with government involvement. Most modern economies are mixed rather than purely free-market or purely command systems. Producers and consumers still make many decisions through buying and selling, but governments set rules, enforce contracts, provide public goods, collect taxes, and respond when markets fail. During a crisis, this mixed structure becomes especially visible.

Governments can play several roles at the same time. They may act as a stabilizer by trying to reduce unemployment and restore confidence. They may serve as a regulator by preventing bank runs, fraud, or dangerous business practices. They may become a spender by funding projects or relief programs. They may also become a redistributor by moving income and wealth toward people who are suffering the most. In some cases, they even become a temporary owner or shareholder if key firms are rescued.

Why governments intervene in crises

Markets are powerful at coordinating supply and demand, but they do not always correct problems quickly or fairly. Fear can spread faster than facts, banks can stop lending, and firms can fail even when their products are still useful. Government action aims to prevent a short-term shock from turning into a long-term collapse of jobs, income, and productive capacity.

Government action does not replace markets completely. Instead, it changes incentives, rules, and flows of money so that producers keep producing, consumers keep buying essential goods, and financial institutions keep credit moving. In that sense, crisis policy is part of understanding how government policies affect market outcomes.

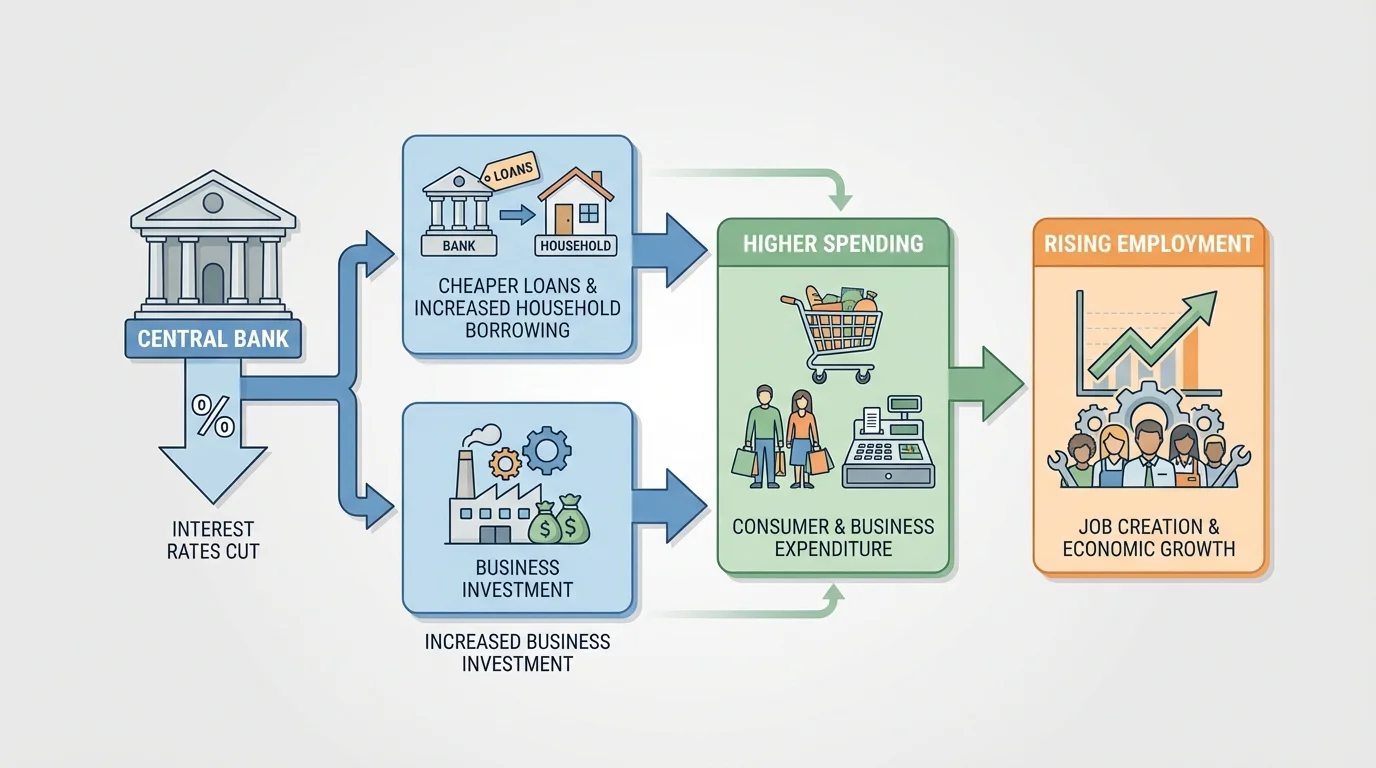

[Figure 1] Monetary policy is the use of central bank tools to influence the money supply, credit conditions, and interest rates. In the United States, the Federal Reserve plays this role. When a recession hits, the central bank often tries to make borrowing easier because a lower interest rate can trigger a chain reaction: cheaper loans can encourage households to spend and businesses to invest, which can support production and employment.

The most common tool is changing interest rates. If the central bank lowers a policy rate, banks may lower rates on loans for houses, cars, and business expansion. That can increase demand. The central bank can also buy government securities in open-market operations, adding money to the banking system. In some systems, it can change reserve requirements or use emergency lending to support banks and financial markets.

Lower rates are called expansionary monetary policy because they are meant to expand economic activity. Higher rates are called contractionary monetary policy because they are meant to slow spending and reduce inflation. If inflation rises too fast, the central bank may increase rates so that borrowing becomes more expensive and demand cools down.

Monetary policy is powerful, but it has limits. If people are frightened about the future, they may not borrow even when rates are low. Banks may also become cautious and lend less. This is one reason monetary policy sometimes works more slowly than people expect. There can be a time lag between the policy change and the effect on jobs and prices.

Another challenge is that low interest rates can push up asset prices, such as stocks and housing, which may help some households more than others. This means monetary policy can affect inequality as well as overall output. Later, when recovery begins, the central bank may need to reverse course if inflation becomes a problem, a trade-off that becomes clearer when comparing crises over time, as [Figure 4] displays in historical context.

In severe crises, some central banks use unconventional tools such as large-scale asset purchases, sometimes called quantitative easing, to push more money into financial markets when normal rate cuts are not enough.

For everyday life, monetary policy matters because it influences monthly loan payments, credit card costs, home buying, business borrowing, and the willingness of firms to hire. Even students who do not yet have loans are affected when local employers respond to changes in credit conditions.

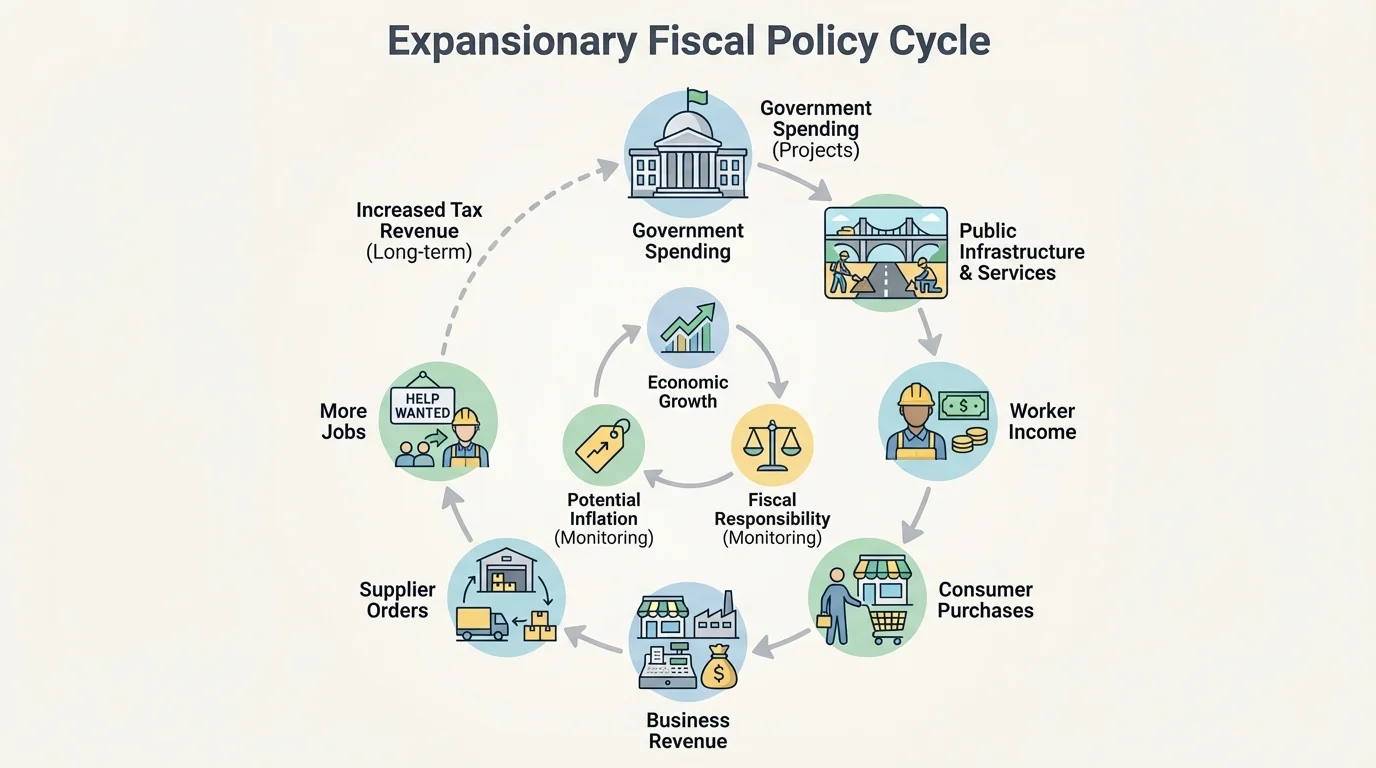

[Figure 2] Fiscal policy refers to government decisions about spending and taxation. Unlike monetary policy, which is mainly handled by a central bank, fiscal policy is usually shaped by elected officials and government budgets. During a recession, governments often use expansionary fiscal policy by increasing spending, cutting taxes, or both.

Government spending can support demand directly. If the government funds road repairs, school improvements, transit systems, or emergency relief, workers and firms receive income. Those workers then spend money at grocery stores, restaurants, and other businesses. The multiplier effect shows why one dollar of government spending can create more than one round of economic activity as income moves from one part of the economy to another.

Tax cuts can also stimulate demand. If households keep more of their income, they may increase spending. If firms face lower taxes, they may invest more in equipment or hiring. However, the impact depends on what people do with the extra money. If they save instead of spend, the short-term boost is smaller.

Some fiscal tools work automatically. Automatic stabilizers are programs that increase support during downturns without requiring a brand-new law every time. Unemployment insurance is a major example. When more people lose jobs, more benefits are paid, which helps families keep spending on necessities. Progressive income taxes can also stabilize the economy because tax payments tend to fall when incomes fall.

Fiscal policy often involves deficit spending, which means the government spends more than it collects in taxes. Supporters argue this is necessary during a crisis because private spending is too weak. Critics worry that rising debt can become a burden later or that heavy borrowing may reduce private investment. This concern is sometimes called crowding out, although its strength depends on economic conditions.

Case example: Stimulus during a recession

A government approves $100 billion for infrastructure and emergency aid when businesses are cutting jobs.

Step 1: The government pays construction firms, transit agencies, and local governments.

These organizations hire workers, buy materials, and maintain services.

Step 2: Workers receive wages and spend part of that income.

Restaurants, stores, and service providers gain customers.

Step 3: Businesses that see stronger sales place new orders and may hire more staff.

The original spending creates additional rounds of income throughout the economy.

The total increase in economic activity may be larger than the initial government payment, though the exact size depends on how much money is saved, taxed, or spent on imports.

Fiscal policy also has time lags. Legislatures may debate a bill for months, and large projects take time to begin. That is why governments often combine fiscal policy with faster-acting monetary tools.

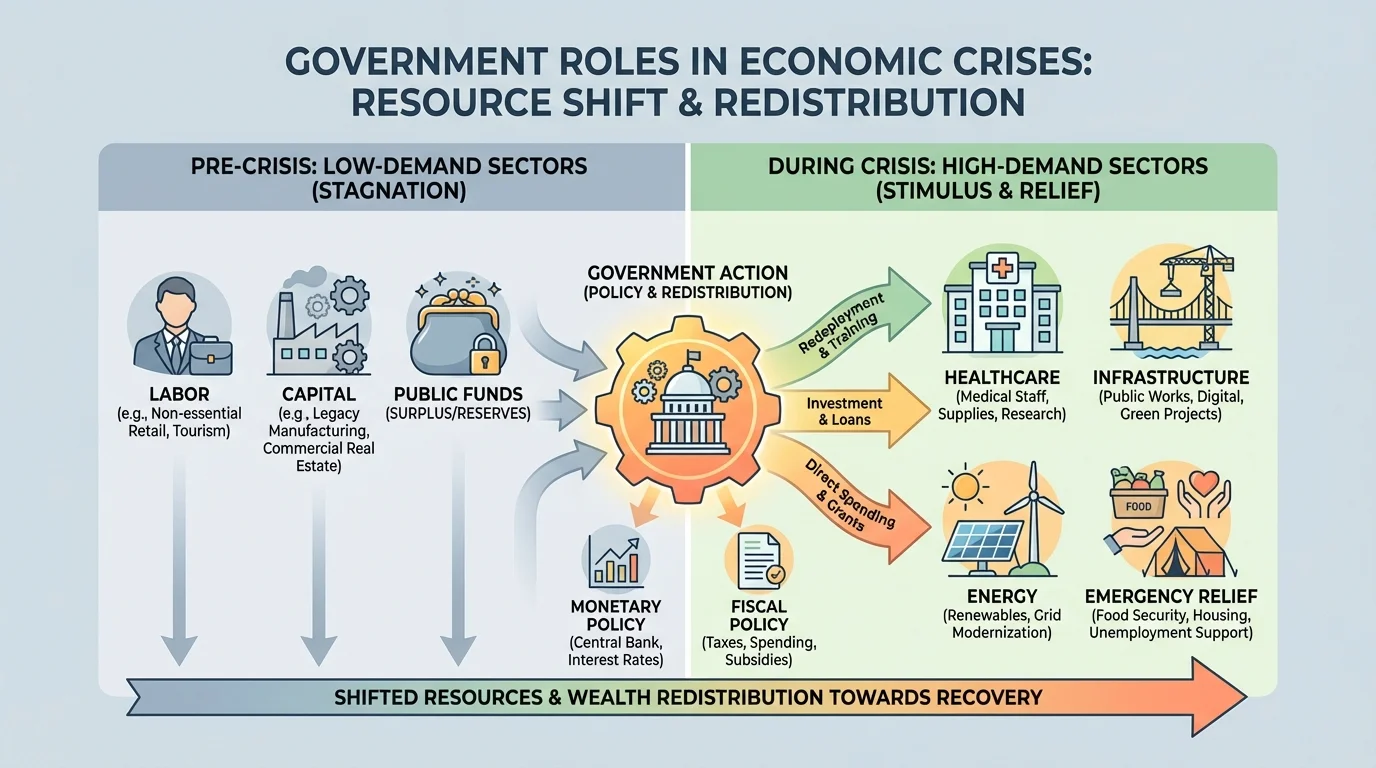

[Figure 3] Besides changing taxes and interest rates, governments may engage in resource allocation, meaning they direct labor, capital, materials, and public funds toward urgent needs. In a major crisis, markets alone may not move resources quickly enough. Governments can shift resources away from lower-priority uses and toward healthcare, infrastructure, energy support, or emergency relief.

Resource reallocation can happen in several ways. Governments can place large public orders, offer subsidies, set temporary rules, or coordinate production across industries. During the Great Depression, public works programs moved labor into construction and conservation. During wartime, factories may switch from consumer goods to military production. During the COVID-19 crisis, governments funded vaccine development, testing, hospital capacity, and support for supply chains.

This role matters because an economy is not only about the total amount of spending; it is also about where workers, machines, and money are being used. A crisis may reveal shortages in medicine, energy, housing, or transportation. Government action can redirect resources to prevent those shortages from becoming even worse.

Reallocation can protect long-term productivity too. If governments invest in bridges, broadband, public transit, or power grids during a downturn, they are not only creating short-term jobs. They are also improving the infrastructure that producers and consumers rely on later. In this way, crisis policy can shape future market outcomes, not just immediate survival.

However, governments do not always choose perfectly. Political pressure, poor information, and lobbying can lead resources to be directed inefficiently. Some industries may receive support because they are powerful, not because they are most essential. This is one reason economists debate which interventions are truly necessary.

Economic crises rarely hurt everyone equally. Workers in unstable jobs, small businesses, renters, and low-income households often face the greatest pressure first. Because of this, governments may use redistribution to move income or wealth toward groups most affected by the downturn.

Redistribution can happen through transfer payments, such as unemployment benefits, food assistance, housing aid, child tax credits, or direct stimulus checks. It can also happen through the tax system. A progressive tax structure, in which higher incomes are taxed at higher rates, can reduce inequality and fund public programs. During a crisis, redistribution aims to keep people housed, fed, and connected to the economy rather than allowing a sharp fall in living standards.

Why redistribution affects markets

Redistribution is not only about fairness. Lower-income households are more likely to spend additional money quickly on necessities. That means support directed to those households can also stabilize demand for producers such as grocery stores, landlords, transportation services, and local retailers.

At the same time, redistribution is debated. Supporters say it reduces suffering, protects opportunity, and strengthens recovery. Critics argue that very high taxes or poorly designed benefits may reduce incentives to work, save, or invest. The challenge is to design policies that provide security without creating long-term dependence or unfair burdens.

This issue also connects to wealth, not just income. Wealth includes assets such as homes, stocks, and savings. During some crises, wealthier households may recover faster because they own assets that rise in value after government rescue measures. That is why some analysts argue that rescue policies should be paired with broader support for renters, workers, and small business owners.

Government responses can change the balance between large firms and small firms. In a highly concentrated industry, a few dominant businesses may survive a crisis more easily because they have larger cash reserves and easier access to loans. Smaller competitors may fail. If the government supports only major firms, the crisis can leave markets less competitive afterward.

This raises questions about bailouts and moral hazard. Moral hazard happens when people or firms take greater risks because they expect to be rescued from the consequences. If banks believe the government will always save them, they may make riskier decisions. Yet if governments never intervene, the failure of a giant bank or airline could spread damage across the whole economy. Policymakers must weigh the risk of future bad behavior against the need to prevent immediate collapse.

Competition usually leads to lower prices, more innovation, and better choices for consumers. During a crisis, one goal of policy is not just to save output today but to preserve healthy competition for the future.

Consumer outcomes matter too. If policies preserve employment and keep supply chains operating, consumers benefit from steadier prices and product availability. If policies are weak or poorly targeted, shortages, layoffs, and business closures can leave consumers with fewer options and higher costs.

Regulation also becomes important. Governments may tighten rules on banks, stock markets, or essential goods after a crisis. These rules are meant to make future breakdowns less likely, though businesses sometimes argue that excessive regulation can slow growth.

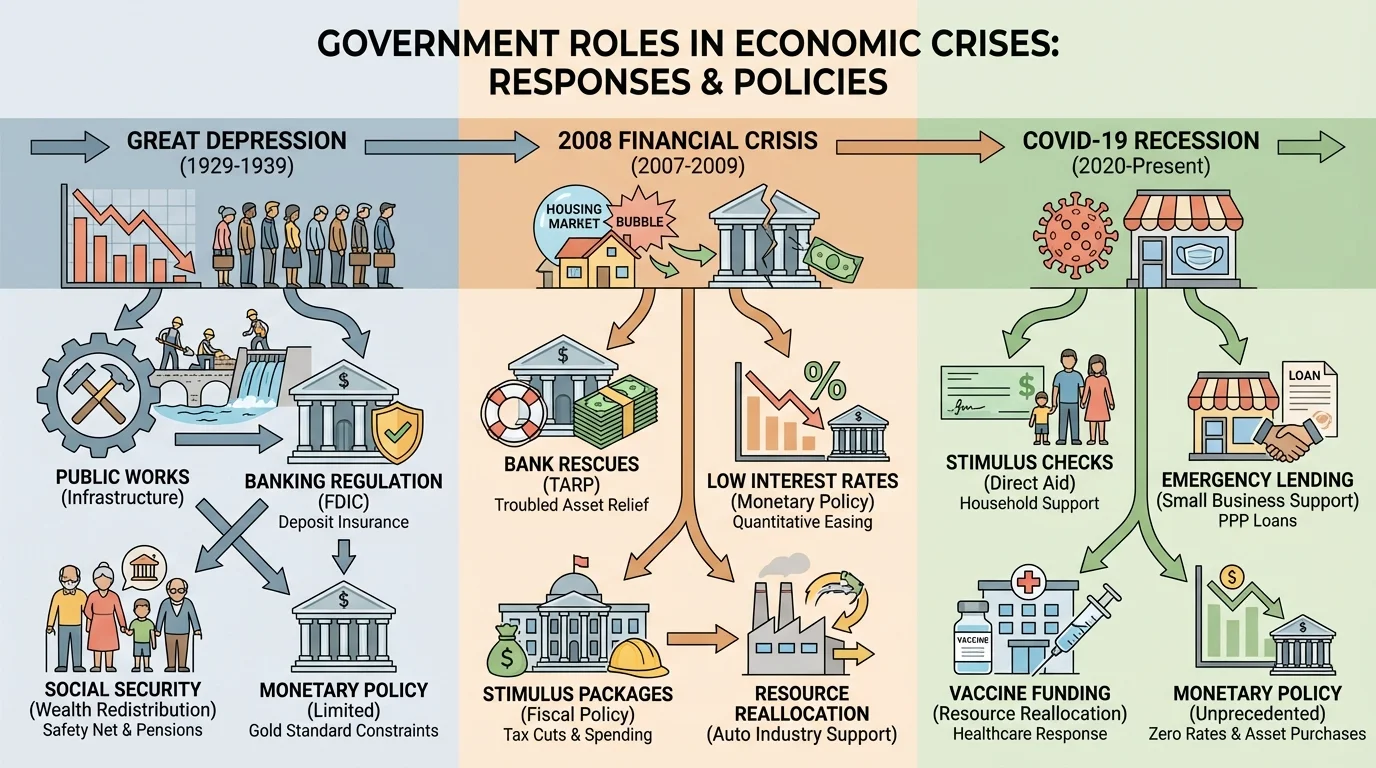

A timeline compares major crises with the government responses used in each era. History shows that no single tool solves every crisis. Different periods call for different combinations of policies. Looking at these examples helps explain why policymakers argue so intensely about what to do.

The Great Depression of the 1930s brought massive unemployment and bank failures. Governments responded with public works programs, banking reforms, financial protections, and social insurance systems. These measures expanded the government's role in stabilizing the economy and protecting households. Public jobs programs were also a form of resource reallocation because labor was moved into roads, parks, schools, and other public projects.

During the 2008 financial crisis, governments and central banks focused heavily on the banking system and credit markets. Interest rates were cut, emergency lending expanded, and major financial institutions were rescued or supported. Fiscal stimulus was also used in several countries. Critics argued that banks were helped faster than homeowners, while supporters argued that stabilizing finance was necessary to prevent a deeper collapse.

In the COVID-19 recession, the crisis began not from a normal business cycle slowdown but from a global health emergency that disrupted work, travel, schools, and supply chains. Governments responded with direct payments, unemployment support, loans to businesses, public health spending, and aggressive central bank action. This period also showed the tension between stabilizing the economy and later controlling inflation, since strong support combined with supply problems helped push prices upward in many countries.

These examples reveal a pattern. Monetary policy often supports financial conditions. Fiscal policy supports income and demand. Resource reallocation addresses urgent shortages. Redistribution tries to reduce hardship and prevent inequality from widening too far. Together, these tools show the many roles governments can play in a mixed economic system.

Government intervention can reduce damage, but it is never cost-free. Expansionary policies can contribute to inflation if demand rises faster than supply. Large deficits can increase public debt. Poorly timed policies may arrive after the worst of the downturn has passed. Excessive support for failing firms may weaken competition and reward bad management.

There are also political trade-offs. Voters may agree that action is needed but disagree on who should receive help first: large employers, local governments, banks, homeowners, students, or low-income families. Some want faster recovery even if debt rises; others prefer smaller government even if recovery is slower. These disagreements are normal because crisis policy combines economics with values about fairness, risk, and responsibility.

| Government role | Main tools | Goal during crisis | Possible risks |

|---|---|---|---|

| Central bank | Interest rate changes, asset purchases, emergency lending | Support credit, spending, and financial stability | Inflation, asset bubbles, unequal gains |

| Fiscal authority | Government spending, tax cuts, transfers | Raise demand and protect incomes | Debt growth, delays, inefficient spending |

| Resource coordinator | Subsidies, contracts, emergency rules, public investment | Move labor and capital to urgent needs | Political favoritism, waste |

| Redistributor | Benefits, progressive taxes, direct aid | Reduce hardship and inequality | Incentive concerns, budget pressure |

| Regulator | Bank rules, market oversight, consumer protections | Prevent collapse and future instability | Compliance costs, overregulation |

Table 1. Major government roles during economic crises, their policy tools, goals, and risks.

The most effective response usually depends on the type of crisis. A banking panic may require fast central bank action. A collapse in consumer spending may call for fiscal stimulus. A supply shock may require targeted resource reallocation. A crisis that increases inequality may demand stronger redistribution. Good policy is rarely about using one tool alone; it is about choosing the right mix for the problem.