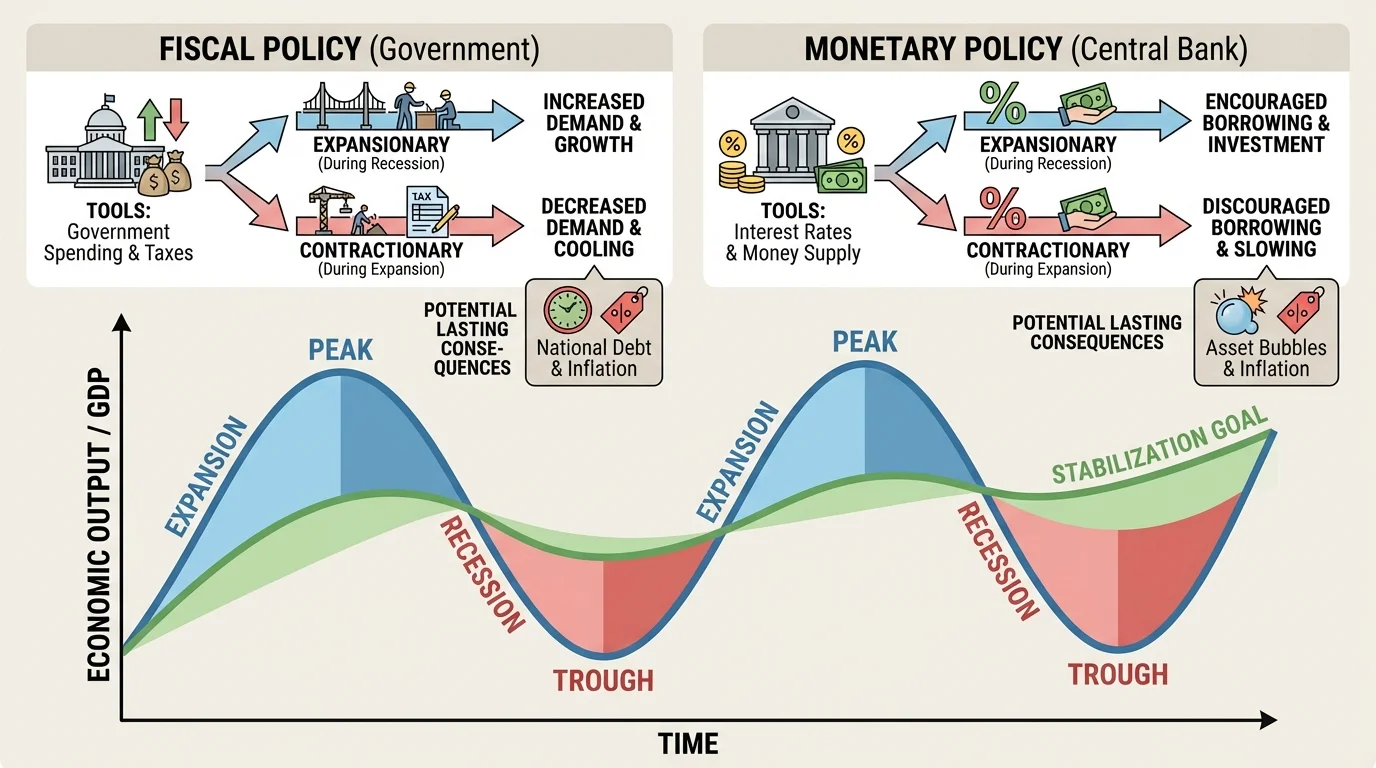

One of the most challenging realities of modern economies is that leaders are expected to fight two opposite problems at the same time: when the economy is weak, they try to increase spending and hiring, but when prices rise too fast, they try to slow spending down. Economies do not move in a straight line. As [Figure 1] illustrates, they rise, slow, fall, and recover in repeating patterns called the business cycle. Because millions of households and businesses make decisions at once, those ups and downs can spread quickly through the whole economy.

When businesses cut production, workers may lose jobs and families spend less. That lower spending can hurt other businesses too. These ups and downs can repeat over time. On the other hand, if spending grows too quickly, prices may rise faster than wages, making everyday life more expensive. Governments and central banks use policy tools to try to smooth these swings. They cannot eliminate the business cycle entirely, but they try to reduce its most harmful effects.

Two of the most important tools are fiscal policy and monetary policy. Fiscal policy involves decisions about government spending and taxes. Monetary policy involves decisions by a central bank, such as the Federal Reserve in the United States, about interest rates and the money supply. Both aim to influence total spending in the economy, but they work in different ways and can create different consequences over time.

Recession is a period of declining economic activity, usually marked by falling output and rising unemployment.

Inflation is a sustained increase in the general level of prices over time.

Unemployment is the condition of people who are able and willing to work but cannot find jobs.

Aggregate demand is the total demand for goods and services in an economy.

A useful way to think about stabilization policy is this: if the economy is operating below its potential, leaders may try to push total demand upward. If the economy is overheating and inflation is accelerating, they may try to pull total demand downward. In a simplified way, economists often describe total output as depending on spending by households, businesses, government, and foreign buyers. When one part falls sharply, policy can try to fill some of the gap.

Fiscal policy is controlled mainly by elected officials and government budget decisions. It includes changes in government purchases, transfer payments, and taxes. When the government increases spending or cuts taxes to boost the economy, it is using expansionary fiscal policy. This policy raises aggregate demand: more government spending or lower taxes can increase consumer and business spending, which encourages firms to produce more and hire more workers.

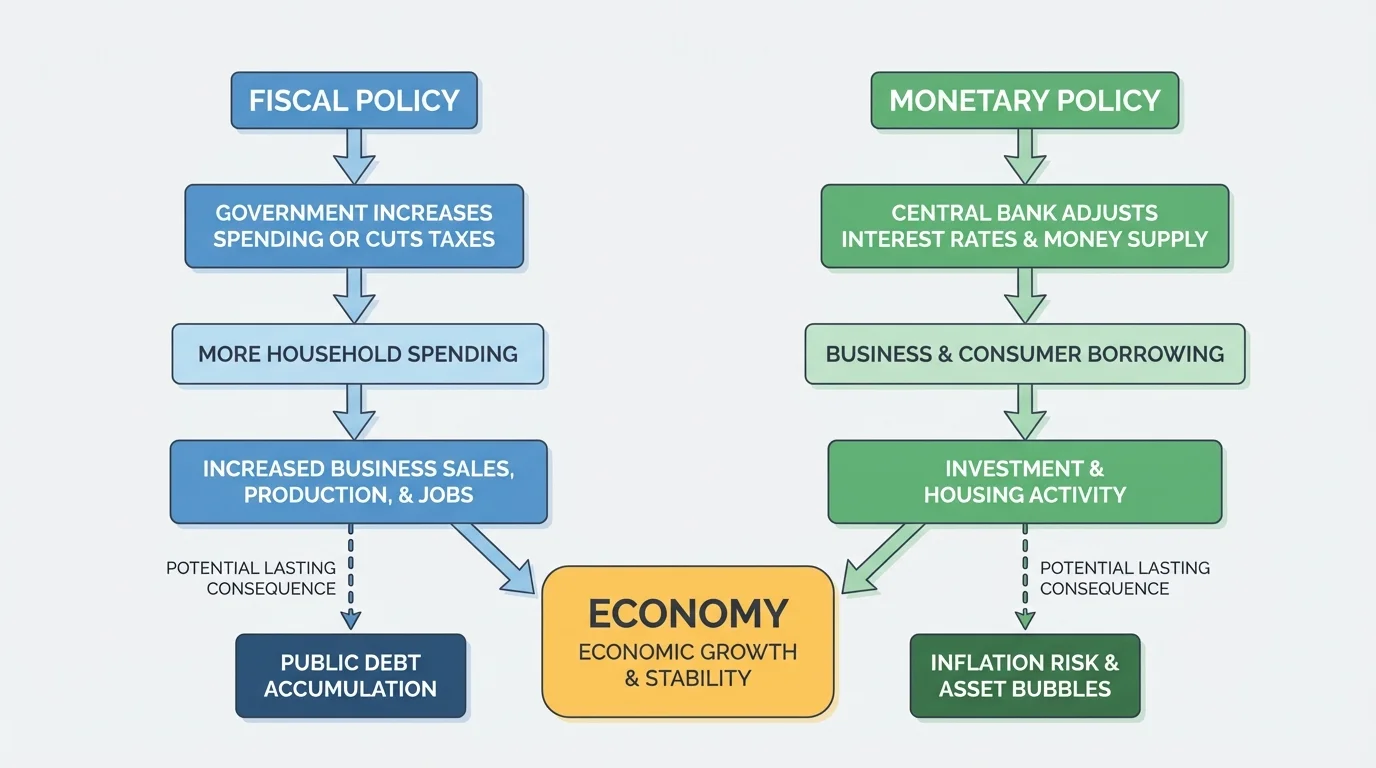

For example, suppose the economy is in recession. As [Figure 2] shows, fiscal stimulus can set off a chain reaction through spending, production, and employment. Factories have unused capacity, stores have fewer customers, and unemployment is rising. The government might fund road repairs, school construction, clean-energy projects, or disaster recovery. Those projects directly create jobs. The workers who get paid then buy food, clothes, transportation, and other goods. That extra spending becomes income for other businesses and workers.

Tax cuts can work in a similar way. If households keep more of their income, they may spend more. If businesses receive tax relief, they may invest in new equipment or expand production. In both cases, the goal is to increase total spending fast enough to support recovery.

The opposite approach is contractionary fiscal policy. This means reducing government spending, increasing taxes, or both, in order to slow the economy and reduce inflationary pressure. If demand is rising so quickly that prices are climbing rapidly, the government may try to remove some spending power from the economy. This can help cool inflation, but it may also slow growth and increase unemployment.

Fiscal policy has strengths. It can target specific groups or sectors. For instance, infrastructure spending can focus on transportation, energy, or technology. Aid can be directed toward unemployed workers, low-income households, or local governments. But fiscal policy also has weaknesses. It often takes time for lawmakers to debate, pass, and implement budget changes. By the time a policy takes effect, economic conditions may already have changed.

Case study: A recession response

A country enters a downturn and unemployment rises from low levels to a much higher rate. Consumer spending falls, and businesses delay investment.

Step 1: The government approves $200 billion in infrastructure spending.

This directly raises demand because the government is purchasing labor, materials, and services.

Step 2: Households receive wages and suppliers receive payments.

Some of that new income is spent on other goods and services, spreading the effect through the economy.

Step 3: Businesses respond to stronger sales.

They may rehire workers, increase orders, and restart delayed projects.

The intended result is lower unemployment and higher output, though the exact effect depends on timing, confidence, and how much of the extra income is actually spent.

Another important fiscal idea is the budget balance. When government spending is greater than tax revenue, the government runs a deficit. When deficits continue year after year, they add to the national debt. Deficits may be useful during severe recessions, but large long-term debt can create future challenges such as higher interest costs and pressure on future budgets.

Monetary policy is managed by a country's central bank. The central bank influences the supply of money and credit, mainly by changing short-term interest rates and using tools that affect lending conditions. When the central bank lowers interest rates to encourage borrowing and spending, it is using expansionary monetary policy. Cheaper borrowing can lead households to finance cars and homes more easily, while businesses may borrow to open new locations, buy machines, or hire workers.

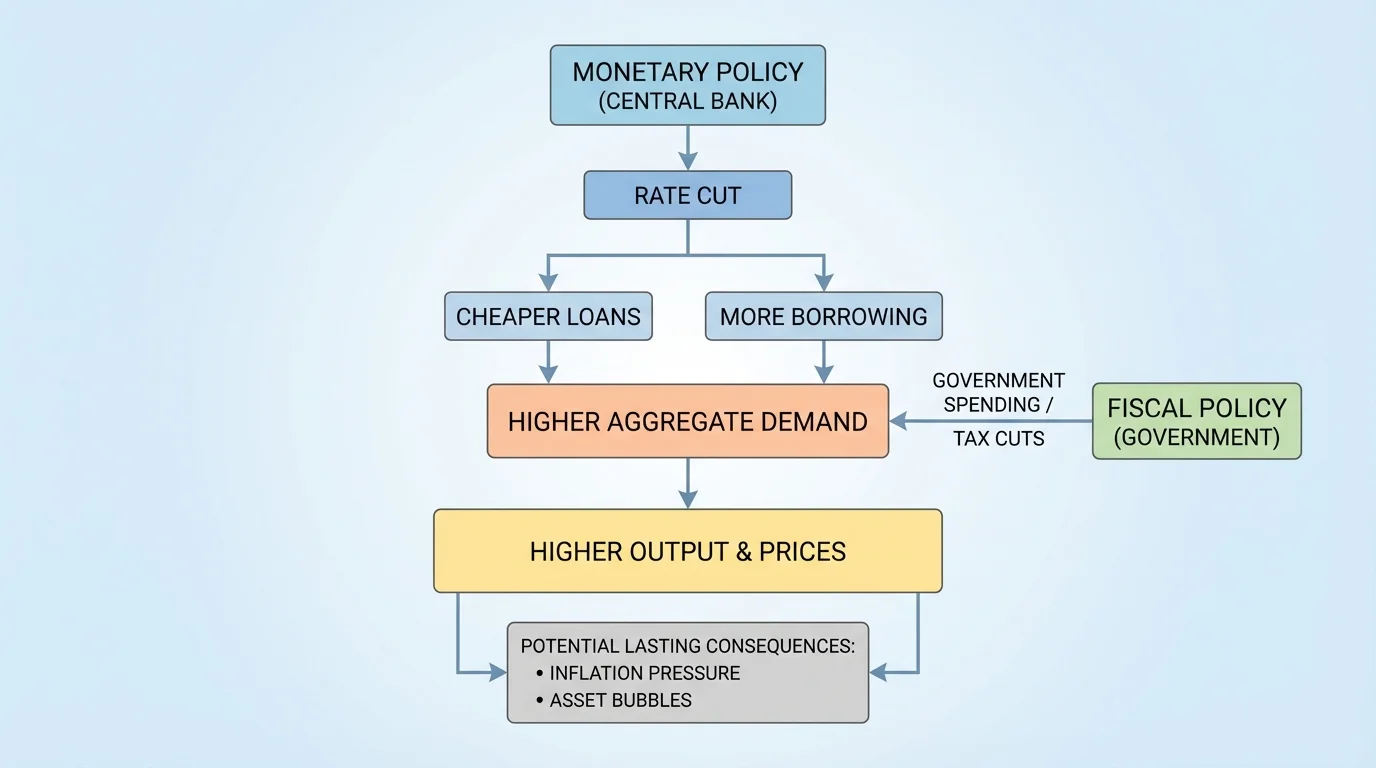

As [Figure 3] shows, lower interest rates matter because they change the cost of credit. If it becomes less expensive to borrow, demand often rises. A family may decide that a mortgage payment is now affordable. A company may decide that a factory upgrade is worth the cost. Higher spending can raise production and reduce unemployment.

Central banks can also increase liquidity in the financial system. In unusual crises, they may purchase financial assets to push down longer-term rates and keep lending markets functioning. This was especially important during major financial disruptions, when fear caused banks and investors to pull back.

The opposite strategy is contractionary monetary policy. If inflation is too high, the central bank may raise interest rates. Borrowing then becomes more expensive. Households may postpone big purchases, businesses may reduce investment, and demand may cool. Slower demand can reduce inflation, but it can also raise unemployment in the short run.

Monetary policy can often move faster than fiscal policy because central banks do not need the same kind of legislative approval for each decision. However, it still works with a time lag. A rate change today does not instantly alter prices or employment tomorrow. It may take months before businesses and consumers fully respond.

How interest rates transmit monetary policy

Interest rates influence more than loans. They affect saving, stock prices, housing demand, exchange rates, and business confidence. When rates rise, saving becomes more attractive and borrowing becomes less attractive. When rates fall, the reverse tends to happen. Because these changes affect many decisions at once, monetary policy can spread through the entire economy.

There are limits to monetary policy. If rates are already very low, cutting them further may not have much effect. During a crisis, people and businesses may be too uncertain to borrow even if loans are cheap. Banks may also lend less if they fear defaults. That is one reason fiscal policy and monetary policy are sometimes used together.

Both fiscal and monetary policy try to influence aggregate demand, but the pathways differ. Fiscal policy changes spending directly through the government budget or indirectly through taxes. Monetary policy changes the incentives to borrow, lend, save, and invest. In both cases, the goal is to affect output, employment, and prices.

Economists sometimes express total output as the sum of major spending categories: \[Y = C + I + G + NX\]

where output \(Y\) depends on consumption \(C\), investment \(I\), government spending \(G\), and net exports \(NX\). Fiscal policy mainly changes \(G\) and can influence \(C\) through taxes. Monetary policy mainly affects \(C\) and \(I\) through interest rates and credit conditions.

This is why the same policy can feel different depending on where you are in the economy. A student's family may notice lower mortgage rates before noticing changes in inflation. A construction company may benefit early from public spending. A retiree may feel harmed by inflation even during strong employment growth. Policy affects groups differently, even when the national goal is stabilization.

The smoothing idea from [Figure 1] matters here. Policymakers are not just trying to make the economy bigger; they are trying to reduce harmful swings. A deep recession wastes labor and resources. Very high inflation erodes purchasing power and makes planning difficult for households and firms.

During a recession, expansionary policy is common. Governments may raise spending or cut taxes, and central banks may lower interest rates. During a strong recovery, policymakers may slowly reduce emergency support to avoid creating too much inflation later. During an overheating period, contractionary policy becomes more likely.

These choices are difficult because the economy does not send perfectly clear signals. Inflation might be caused by excessive demand, but it can also be caused by supply shocks, such as rising energy prices or disrupted shipping. If inflation comes mostly from supply problems, reducing demand may lower inflation only partly while still hurting employment.

| Economic condition | Common fiscal response | Common monetary response | Main goal |

|---|---|---|---|

| Recession | Increase spending or cut taxes | Lower interest rates | Raise output and employment |

| Recovery | Reduce emergency support gradually | Keep rates supportive, then normalize | Maintain growth without overheating |

| High inflation | Cut spending or raise taxes | Raise interest rates | Slow price increases |

Table 1. Typical policy responses during different phases of the business cycle.

No response is automatic or perfect. If policymakers act too weakly, a recession may last longer. If they act too strongly, inflation or debt problems may worsen. Good policy requires timing, judgment, and constant revision as new data arrives.

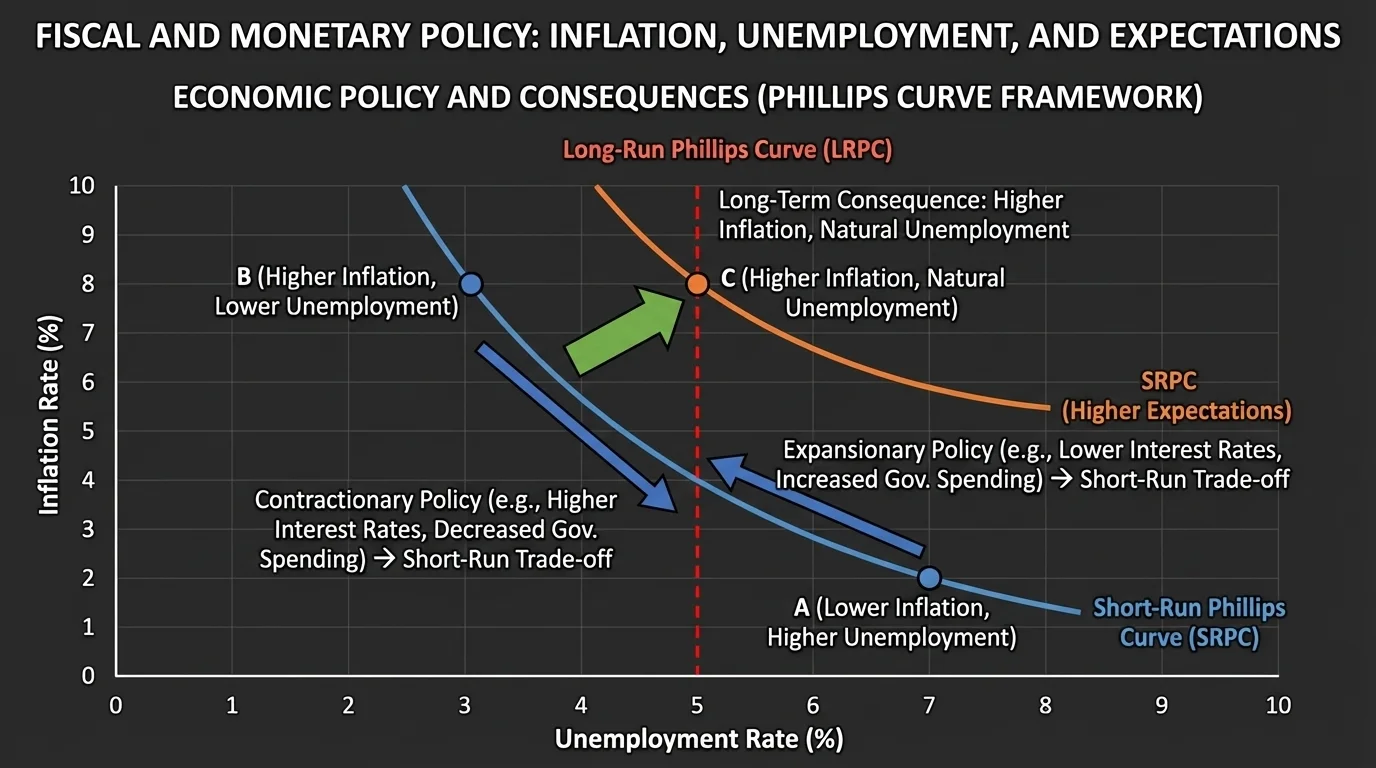

Policy does not just create short-term effects. It can also leave long-lasting consequences. As [Figure 4] illustrates, one major trade-off involves inflation and unemployment. In the short run, efforts to reduce inflation can slow the economy and raise joblessness, while efforts to reduce unemployment can increase inflationary pressure. This short-run tension also shows why expectations matter: if people begin to expect higher inflation in the future, controlling inflation becomes harder.

If workers expect prices to keep rising, they may demand higher wages. Businesses expecting higher costs may raise prices sooner. This can create an inflationary cycle that becomes self-reinforcing. Central banks often try to prevent this by acting firmly enough that the public believes inflation will come back down.

Fiscal policy can create lasting effects through public debt. Borrowing to fight a recession can be useful, especially when unemployment is high and private spending is weak. But if debt grows continuously, future governments may face harder choices. More tax revenue may go toward paying interest instead of funding education, infrastructure, or health care.

Another concern is crowding out. If government borrowing becomes very large, it can compete with private borrowers for available funds. That may push interest rates upward and reduce private investment. In that case, short-term stimulus could partly weaken long-term growth if businesses invest less in productivity-improving projects.

Monetary policy also has long-lasting risks. Very low interest rates for a long time can encourage excessive borrowing or speculation. Asset prices such as housing or stocks may rise far above sustainable levels, creating bubbles. If those bubbles burst, the economy can suffer another downturn. As seen earlier in [Figure 3], the same channels that stimulate growth can also overstimulate markets.

Policies can affect inequality as well. Inflation tends to hurt people on fixed incomes if their income does not keep up with prices. Higher interest rates may hurt workers in interest-sensitive industries such as housing and construction. At the same time, very loose monetary policy can increase stock and home prices, which may benefit people who already own assets more than those who do not.

Small changes in interest rates can matter enormously because they affect millions of decisions at once, from business loans and credit cards to home construction and currency values.

There are also policy lags. Recognition lag is the time it takes to realize the economy has changed. Decision lag is the time needed to choose a response. Impact lag is the time before the policy actually changes economic behavior. Because of these delays, policy can sometimes arrive too late or push too far.

Fiscal and monetary policy often aim at the same targets, but they differ in who controls them, how quickly they work, and what side effects they may create. Fiscal policy is more directly political because it involves budgets and taxes. Monetary policy is usually run by a central bank that is designed to be somewhat independent from day-to-day politics.

Fiscal policy can be highly targeted. It can send relief to households, support schools, rebuild roads, or subsidize certain industries. Monetary policy is less targeted but broader. It changes financial conditions across the whole economy. When interest rates move, many sectors react at once.

| Feature | Fiscal policy | Monetary policy |

|---|---|---|

| Main decision-maker | Government leaders and legislature | Central bank |

| Main tools | Spending, taxes, transfers | Interest rates, lending conditions, asset purchases |

| Best at | Targeted support | Broad economy-wide influence |

| Common weakness | Political and implementation delays | May be weak when borrowing confidence is low |

| Long-term risk | Persistent deficits and debt | Inflation, bubbles, or over-tightening |

Table 2. A comparison of the main features, strengths, and risks of fiscal and monetary policy.

In real life, the two policies often interact. If both are expansionary at the same time, the economy may recover faster, but inflation risk can increase. If one is expansionary while the other is contractionary, they can partly cancel each other out.

During major recessions, governments have often increased public spending, sent direct payments, expanded unemployment benefits, or cut taxes. Central banks have lowered rates and taken emergency steps to support lending. These actions aim to stop a downward spiral in which falling income causes falling spending, which then causes even more job losses.

During periods of high inflation, central banks have often raised rates sharply even though the move risks recession. This can be controversial, because fighting inflation may require slowing hiring, reducing investment, and weakening consumer demand. Yet allowing inflation to remain high for too long can damage savings, wages, and business planning even more.

As [Figure 2] shows, fiscal stimulus works through direct spending and disposable income. As [Figure 4] shows, however, reducing inflation may involve painful short-run trade-offs. Real-world policy is rarely about choosing between good and bad options; it is often about choosing between competing costs.

These policies are not abstract. They affect whether jobs are available, whether student loan payments rise, whether car loans become more expensive, whether rent and groceries outpace wages, and whether businesses in a town decide to expand or cut back. If interest rates rise, monthly borrowing costs usually rise too. If a government builds a bridge, upgrades broadband, or funds a new transit project, local hiring can increase.

Students may not vote yet, run a central bank, or write a national budget, but they already live inside the results of these decisions. Economic policy helps shape the cost of college, the ease of finding a first job, and the price of everything from movie tickets to electricity. Understanding fiscal and monetary policy means understanding how societies try to balance growth, stability, and fairness.