Two people can earn the same paycheck and still live completely different financial lives. One may feel constantly stressed, while the other steadily builds savings, pays bills on time, and moves toward future goals. The difference is often not just income. It is planning. A sustainable household budget is more than a list of expenses. It is a way to match your money to the kind of life you want to build.

For teenagers, budgeting may seem like something adults deal with later. But major money decisions begin long before your first full-time job. The courses you take, the skills you develop, whether you pursue college, a certificate, an apprenticeship, military service, or direct entry into work, all shape your income. Those choices also affect where you can afford to live, how quickly you can save, and how flexible your future budget will be.

A household budget is a plan for how income will be used to cover expenses, savings, and financial goals over a period of time, usually a month. The word sustainable matters. A sustainable budget is one you can actually keep using without constantly running short of money or taking on unhealthy debt.

Budgeting connects directly to personal goals. If your future goal is to live independently in a city, your housing and transportation costs may be high. If your goal is to attend a four-year college, you may need to plan for tuition, books, or student loan payments. If your goal is to start a business someday, you may need to build savings early. Financial decisions are not random; they reflect priorities.

Gross income is the total amount of money earned before taxes and deductions. Net income, often called take-home pay, is the amount left after taxes and other deductions are removed. Fixed expenses stay mostly the same each month, while variable expenses change depending on use or choices.

When people ignore budgeting, they often end up reacting to problems instead of preparing for them. A missed bill, a car repair, or a drop in work hours can quickly become a crisis. A good budget does not eliminate problems, but it makes them easier to handle.

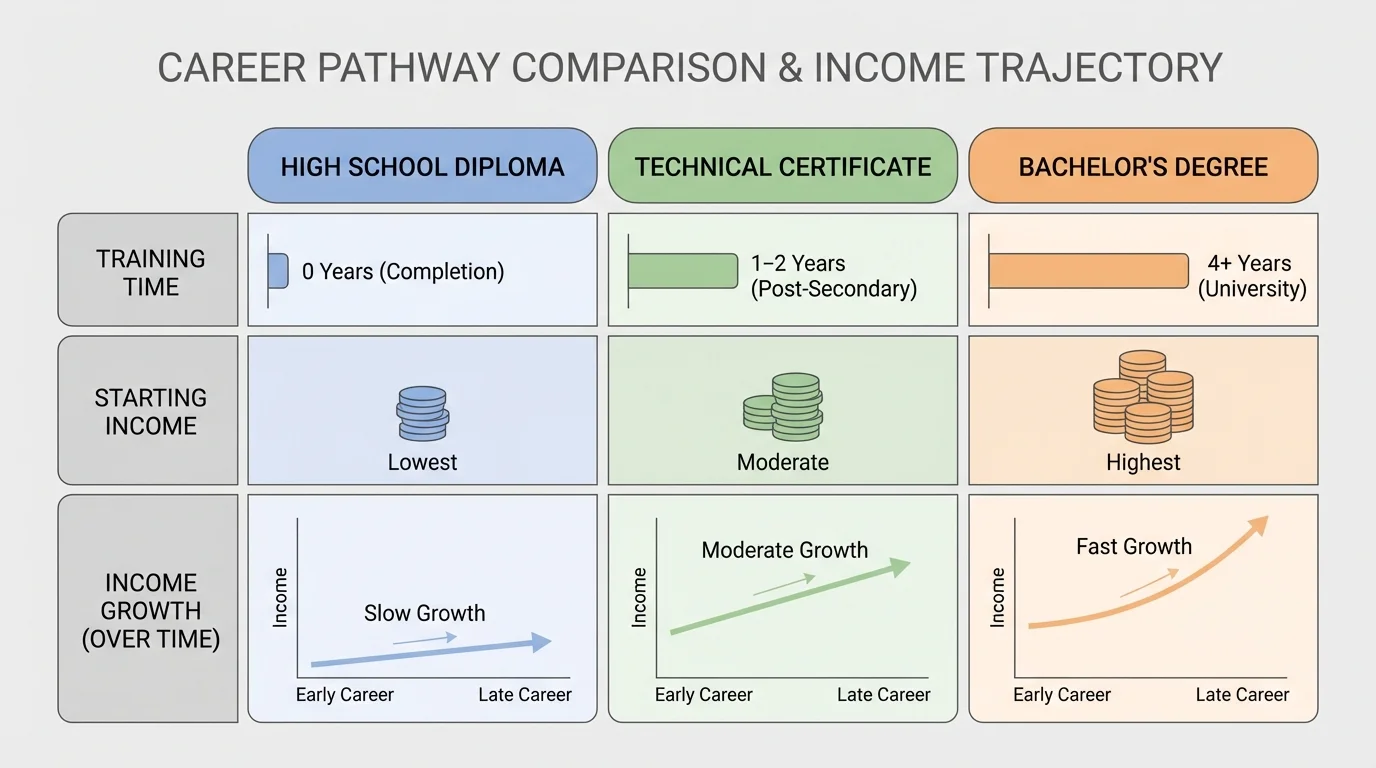

Your lifetime earning potential is the total amount of money you are likely to earn over your working life. It depends on many factors, including occupation, work experience, location, economic conditions, and the level of education or training you complete. Career preparation changes both starting pay and the opportunities for future growth, as shown in [Figure 1].

Income can come from different sources: hourly wages, salaries, tips, commissions, freelance work, business profits, investment income, and government benefits. For most households, earned income from work is the main source. Understanding how work translates into income is essential when building a realistic budget.

Education and training often involve a trade-off. More preparation can mean spending more time and money before entering full-time work. However, it can also lead to higher pay, better benefits, more stability, and greater opportunities for advancement. This is not automatic. Some careers require expensive degrees but offer modest income, while some skilled trades provide strong earnings with shorter training periods.

Continuing education matters too. A worker who updates skills, earns certifications, or learns new technology may become more valuable in the labor market. In many fields, income growth is tied not only to years worked but also to proof of new competence. For example, a person in information technology who gains cybersecurity credentials may qualify for a higher-paying role. A nurse who earns advanced training may take on more responsibility and earn more.

This means a budget should not only track current income. It should also leave room for future growth. Paying for a certification course, professional tools, or additional classes can be an investment if it increases long-term earning power. That same idea appears in [Figure 1], where more preparation can create different income trajectories over time.

Many workers do not stay in the same job for life, but the skills they build can keep increasing their value. A single certification or specialized training program can sometimes raise earnings faster than people expect.

When evaluating a career, students should ask several questions: What is the starting pay? What benefits are included? How much training is required? Will I need to borrow money? How likely is pay to rise with experience? Those answers affect a budget just as much as the number on a first paycheck.

A sustainable budget simulation should begin with a clear picture of your future goals. Suppose you want to become an automotive technician, an elementary teacher, a dental hygienist, or a web developer. Each path has different training requirements, likely income ranges, and lifestyle patterns.

Start by choosing realistic assumptions. Decide on a possible career, location, and living situation. Will you live alone, with roommates, or with family at first? Will you need a car, or can you use public transportation? Are you aiming to save for college, pay off loans, or build an emergency fund? A budget becomes more accurate when it is linked to a specific scenario.

Budget simulation as decision-making

A budget simulation is not about predicting the future perfectly. It is about testing whether a future plan is financially workable. If the numbers do not fit, that does not mean the dream is impossible. It means some part of the plan must change: the career path, the timeline, the living arrangement, the amount of training debt, or the spending habits.

For example, a student planning to become a physical therapist should not only look at the final salary. That student should also consider years of schooling, possible student debt, and the delayed start of full-time earnings. By contrast, a student entering an apprenticeship may start earning sooner, even if long-term income grows differently.

To build a monthly budget, you need monthly net income. A common mistake is to budget using gross income instead of take-home pay. But taxes and deductions reduce what actually reaches your bank account.

A simple estimate uses this relationship:

\[\textrm{Net Income} = \textrm{Gross Income} - \textrm{Taxes} - \textrm{Deductions}\]

If a job pays an annual salary, convert it to monthly gross income first:

\[\textrm{Monthly Gross Income} = \frac{\textrm{Annual Salary}}{12}\]

Worked example: estimating take-home pay from a salary

A student is exploring a career with an annual salary of $42,000. Suppose taxes and deductions are estimated at $9,240 per year.

Step 1: Find annual net income.

\[42{,}000 - 9{,}240 = 32{,}760\]

Step 2: Convert annual net income to monthly net income.

\[\frac{32{,}760}{12} = 2{,}730\]

The estimated monthly take-home pay is $2,730.

Hourly jobs require a different calculation. If someone earns $18 per hour and works an average of 40 hours per week, then weekly gross income is $720 because:

\[18 \times 40 = 720\]

Annual gross income can be estimated by multiplying by 52 weeks:

\[720 \times 52 = 37{,}440\]

After estimated taxes and deductions, the monthly take-home pay may be much lower than students expect. That is why realistic budgeting depends on careful calculation, not guesswork.

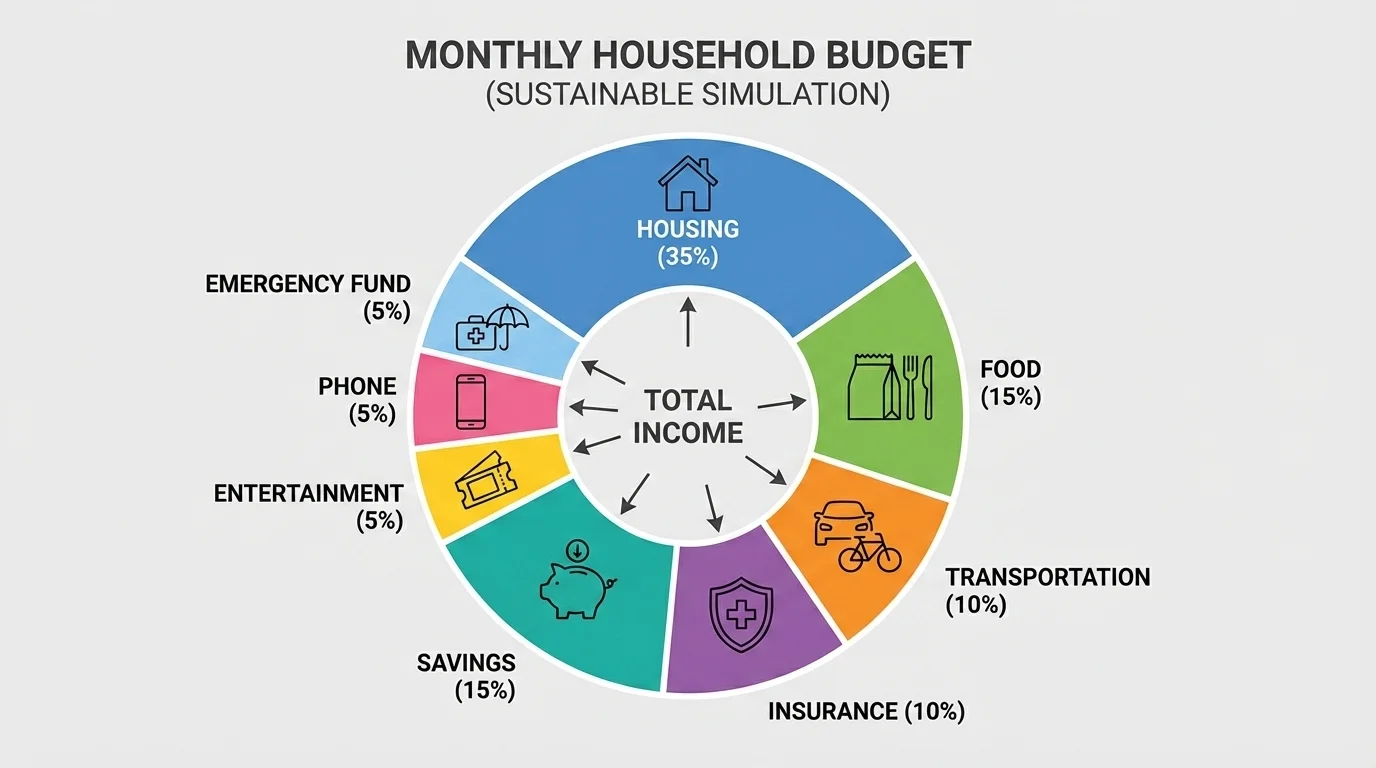

A sustainable budget assigns every dollar a purpose through the balance among housing, food, transportation, insurance, savings, and flexible spending. The goal is not to spend every cent, but to make sure income covers needs, protects against emergencies, and supports future plans.

Most monthly budgets include these categories, as shown in [Figure 2]: housing, utilities, food, transportation, insurance, phone and internet, debt payments, savings, health costs, personal spending, and entertainment. Some expenses are monthly, while others are irregular. For example, car registration or holiday spending may happen once or twice a year, but they should still be planned for monthly.

One useful formula is:

\[\textrm{Money Left Over} = \textrm{Net Income} - \textrm{Total Expenses}\]

If the result is negative, the budget is not sustainable. If it is positive, that leftover amount can go toward extra savings, debt repayment, or long-term goals.

Students should also separate fixed expenses from variable expenses. Rent, insurance, and loan payments are usually fixed. Groceries, gas, clothing, and entertainment are more variable. Variable expenses are often the first place to adjust when money gets tight.

| Category | Example Monthly Cost | Type |

|---|---|---|

| Rent and utilities | $1,050 | Mostly fixed |

| Groceries | $300 | Variable |

| Transportation | $220 | Variable |

| Phone and internet | $110 | Fixed |

| Insurance | $180 | Fixed |

| Savings | $250 | Planned |

| Entertainment and personal | $150 | Variable |

| Miscellaneous | $120 | Variable |

Table 1. A sample set of monthly budget categories showing common household expenses and whether they are fixed or variable.

Worked example: testing whether a monthly budget is sustainable

Suppose monthly net income is $2,730. The planned expenses are: housing $1,050, groceries $300, transportation $220, phone and internet $110, insurance $180, savings $250, entertainment and personal $150, and miscellaneous $120.

Step 1: Add total expenses.

\[1{,}050 + 300 + 220 + 110 + 180 + 250 + 150 + 120 = 2{,}380\]

Step 2: Subtract total expenses from net income.

\[2{,}730 - 2{,}380 = 350\]

This budget leaves $350 each month. That surplus could strengthen the emergency fund, pay debt faster, or save toward a future goal.

A sustainable household budget should usually include an emergency fund, which is money set aside for unexpected costs such as repairs, medical bills, or lost income. Without it, one emergency can force a household into debt.

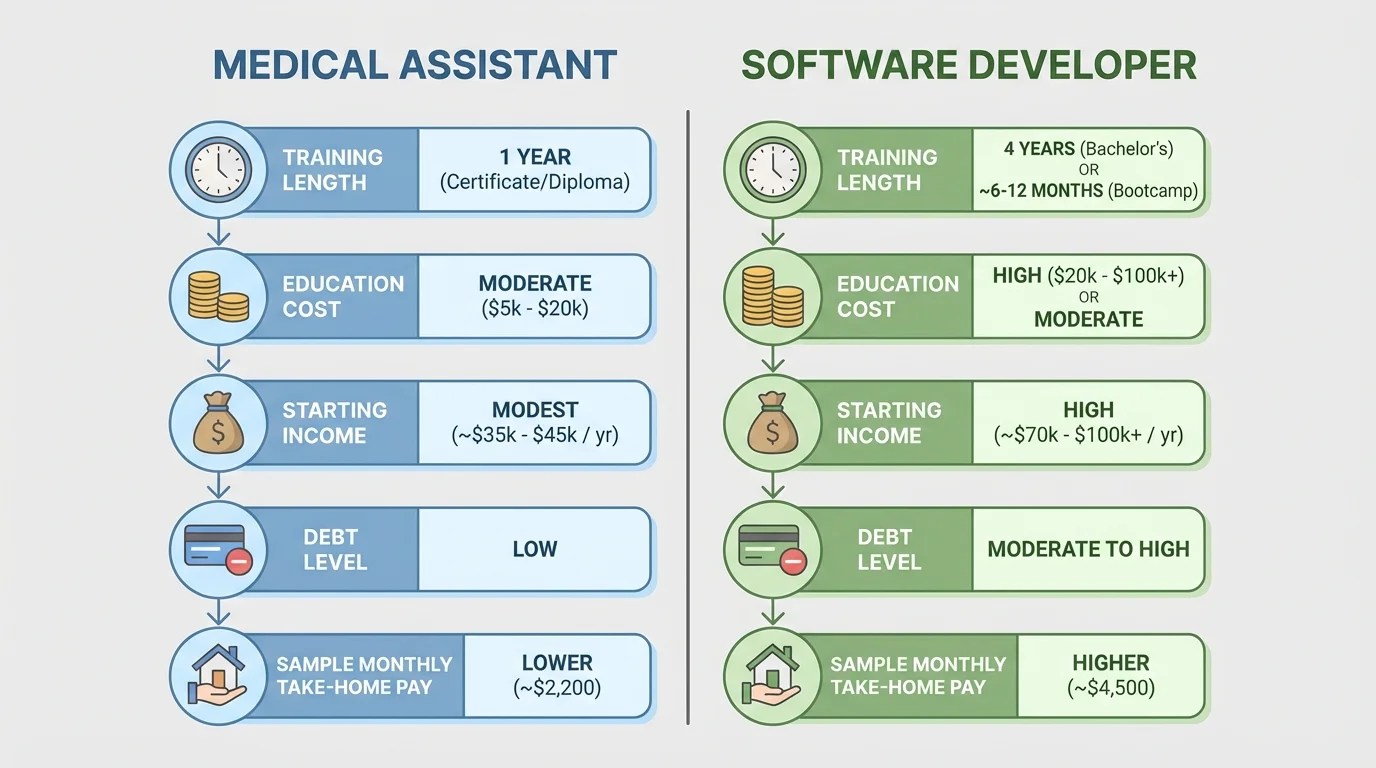

Students should compare not only salary, but also training cost, time before full earnings begin, possible debt, and room for advancement. Two jobs may have similar starting budgets but very different long-term financial outcomes.

Consider two possible paths after high school. One student becomes a medical assistant after a shorter training program. Another studies computer science and becomes a software developer after a longer education path. The second path may have higher income later, but it may also involve more tuition cost and delayed full-time earnings. The first path may produce income sooner and reduce the need for debt.

Worked example: comparing career-path budgets

Path A has monthly net income of $2,600 and monthly expenses of $2,350. Path B has monthly net income of $3,900 and monthly expenses of $3,450, including student loan payments.

Step 1: Find the monthly surplus for Path A.

\[2{,}600 - 2{,}350 = 250\]

Step 2: Find the monthly surplus for Path B.

\[3{,}900 - 3{,}450 = 450\]

Step 3: Compare flexibility.

Path B leaves more monthly surplus, but if loan payments are large, it may be less flexible during a job loss. Path A leaves less surplus, but it may involve less debt and earlier workforce entry.

The better choice depends on goals, risk tolerance, interests, and long-term opportunities.

This comparison teaches an important lesson: higher income does not automatically mean stronger financial health. If higher income comes with much higher debt, housing costs, or lifestyle spending, the budget may still feel tight. A realistic budget looks at the full picture.

The same side-by-side thinking shown in [Figure 3] can help students compare trade school, military service, community college, university, or direct employment. What matters is not only what you earn, but when you start earning, what it costs to prepare, and how that affects your future choices.

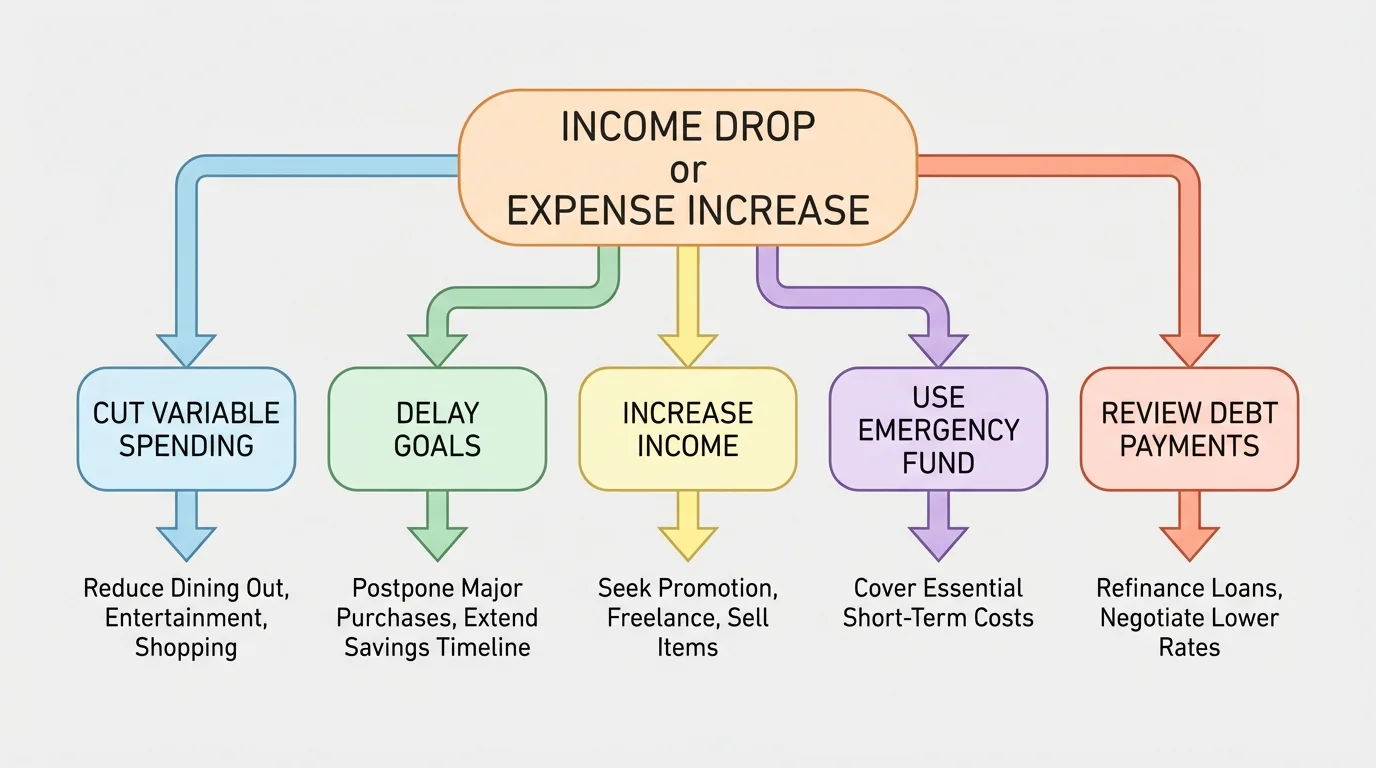

Life rarely follows a perfect plan. Rent rises, gas prices change, work hours fluctuate, and emergencies happen. A sustainable budget needs a response plan for surprises.

[Figure 4] When income drops or expenses rise, start by identifying which costs are essential and which are flexible. Essentials include housing, food, utilities, transportation to work, and health needs. Flexible areas may include subscriptions, entertainment, clothing purchases, and nonessential travel.

Another important factor is inflation. If prices rise over time, a budget that worked last year may not work now. This is one reason households revisit budgets regularly instead of making one plan and forgetting it.

Regional differences matter too. Living in a rural area, suburb, or major city can change housing and transportation costs dramatically. The same salary may feel comfortable in one place and strained in another. Students simulating a budget should choose location assumptions carefully.

Percentages and estimation skills are useful in budgeting. If you know how to find a percent of a number and how to compare totals, you already have important tools for checking whether a spending plan is realistic.

Suppose a household has monthly net income of $3,000 and expenses of $3,150. The budget gap is:

\[3{,}000 - 3{,}150 = -150\]

A negative result means the household is overspending by $150 each month. That cannot continue for long without borrowing, using savings, or missing payments.

Long-term financial stability depends on more than surviving one month. A strong budget supports future goals such as college, retirement savings, home ownership, starting a family, or changing careers. It also leaves room for growth. Workers often earn more over time through promotions, additional skills, and experience, but expenses may grow too.

A opportunity cost is the value of what you give up when you choose one option over another. If you spend money on a new phone, you may give up the chance to add that money to savings or pay down debt. If you enter the workforce immediately instead of attending college, you may gain short-term income but give up part of the higher long-term earnings that some degrees provide. On the other hand, if you borrow heavily for a degree with low payoff, the opportunity cost may work in the opposite direction.

This is why wise budgeting includes both present and future thinking. A financially sound plan asks: Can I afford my current life? Am I protecting myself from emergencies? Am I investing in a future that improves my earning power and choices?

"Budgeting is telling your money where to go instead of wondering where it went."

— A widely used personal finance principle

Continuing education often fits into this long-term view. A worker who returns for specialized training may face short-term costs but gain higher income later. In many careers, standing still is not really standing still. Skills can become outdated. Learning can be a financial strategy.

One major mistake is underestimating expenses. People often remember rent and phone bills but forget toiletries, gifts, car maintenance, fees, and occasional medical costs. Another mistake is budgeting every month as if nothing unexpected will happen. Real budgets need a margin for uncertainty.

A third mistake is increasing spending every time income rises. This is sometimes called lifestyle inflation. If each raise immediately turns into higher spending, long-term financial progress slows down. Saving part of an income increase can improve future security.

Finally, some people choose careers based only on salary and ignore personal interest, job stability, or work conditions. A sustainable financial life depends on income, but also on whether a person can realistically stay in that career and continue developing within it.