A surprising fact about money is that a dollar does not stay equally powerful forever. A snack that costs $1 today might have cost far less years ago, and a wage that sounded great in one decade might not stretch very far in another. That is because the value of money changes over time. To understand earning, spending, borrowing, and investing, we need to understand not just how much money a person has, but what that money can actually do.

When economists talk about the value of money, they often mean its purchasing power, or how many goods and services a certain amount of money can buy. If prices rise, the same amount of money buys less. If prices stay low or fall, that money buys more. This is why two people who each have $100 may not be equally well off if one lives when prices are low and the other lives when prices are high.

Inflation is a general increase in prices over time. It does not mean every single price rises by the same amount, but it does mean that, on average, money buys less than before. A recession, on the other hand, is a period when economic activity slows down. Businesses sell less, workers may lose jobs, and families often spend more carefully. Inflation and recession are different, but both strongly affect financial decisions.

Value of money means how useful money is in buying goods and services.

Inflation is a rise in average prices over time, which reduces purchasing power.

Recession is a period of economic decline marked by weaker business activity, lower spending, and often higher unemployment.

These ideas matter in personal finance because people make choices in markets every day. They decide what to buy, whether to save, whether to borrow, and where to invest. Governments also collect taxes and spend money, which can shape the economy. In early American history, taxes, debt, and unstable money supplies affected colonists and the new nation. Those same kinds of forces still matter today.

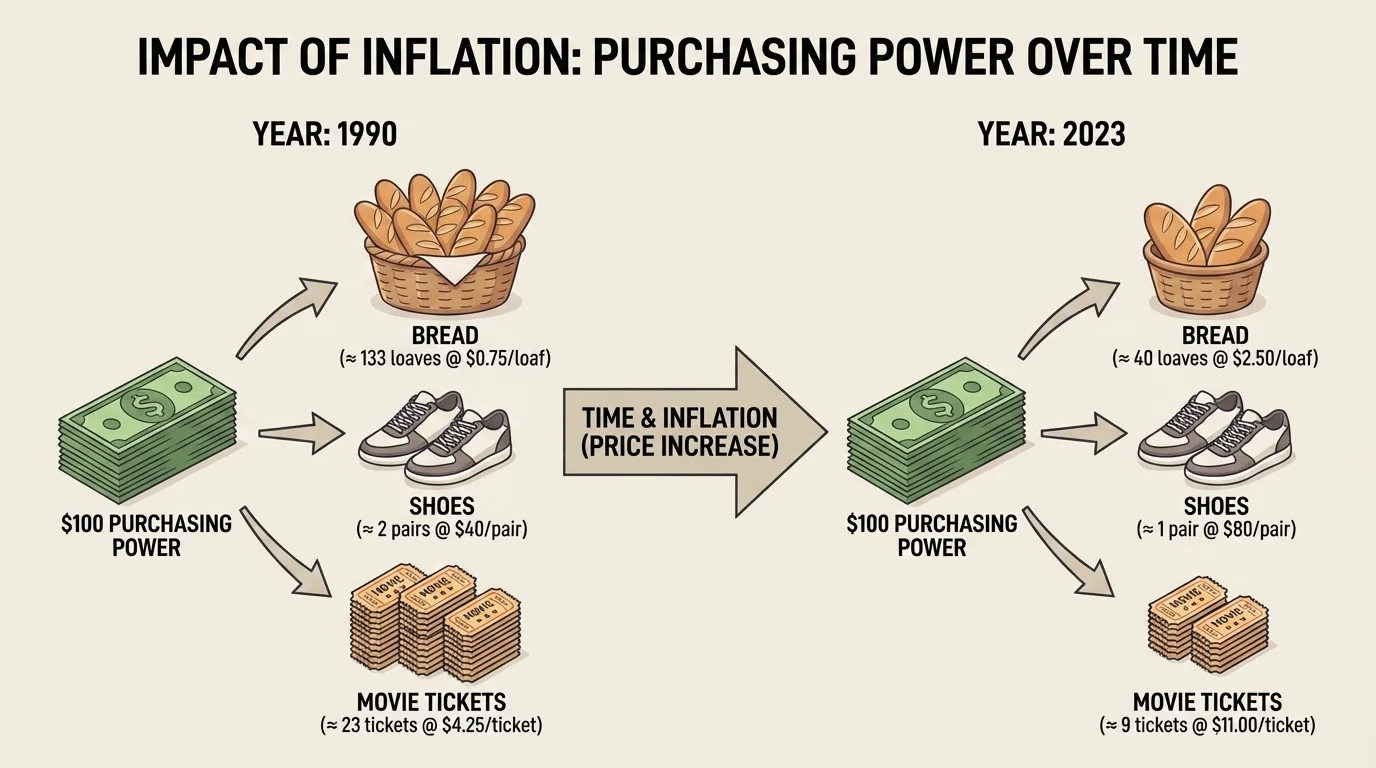

To compare money across time, we often compare prices, as [Figure 1] shows with everyday items that cost different amounts in different years. The key question is not only, "How much money is this?" but also, "What can it buy?" If a movie ticket rises from $8 to $10, the ticket costs more, so the buying power of each dollar has fallen for that purchase.

A common way to measure price change is percent change. The formula is

\[\textrm{Percent change} = \frac{\textrm{new value} - \textrm{old value}}{\textrm{old value}} \times 100\%\]

If the result is positive, the price increased. If the result is negative, the price decreased. This formula helps us measure inflation for one item or compare wages and returns over time.

Economists often use broad price indexes to track inflation in the whole economy. A price index is a measure built from a basket of commonly purchased goods and services. Even if students do not calculate a full national index, understanding the idea is useful: if the basket gets more expensive, the value of money is falling.

Worked example: calculating inflation for one item

A backpack cost $40 last year and $46 this year. Find the percent increase in price.

Step 1: Write the formula.

Use \(\dfrac{\textrm{new} - \textrm{old}}{\textrm{old}} \times 100\%\).

Step 2: Substitute the values.

\(\dfrac{46 - 40}{40} \times 100\% = \dfrac{6}{40} \times 100\%\).

Step 3: Simplify.

\(\dfrac{6}{40} = 0.15\), so \(0.15 \times 100\% = 15\%\).

The backpack price increased by 15%.

This kind of calculation helps families notice whether their costs are rising slowly or quickly. It also helps people judge whether a pay raise, an interest rate, or an investment gain is really keeping up with changing prices.

Money earned from work is called income. But workers care not only about the number on a paycheck; they care about what that paycheck can buy. If a person gets a raise from $12 per hour to $13 per hour, that sounds better. Yet if prices rise even faster, the worker may actually be worse off in real terms.

This leads to the idea of real income. Real income is income adjusted for inflation. If wages rise by less than prices rise, real income falls. If wages rise faster than prices rise, real income increases.

Nominal income and real income

Nominal income is the amount of money a person receives. Real income is what that income can actually buy after considering inflation. A person may earn more dollars but have less buying power if prices rise too much.

Suppose a student works a summer job and earns $1,200 one year. The next year, the student earns $1,260. That is a gain of $60, which seems positive. But if overall prices rose by more than that percentage, the student's earnings may not stretch as far for clothes, transportation, or school supplies.

Worked example: comparing wage growth to inflation

A worker's hourly pay rises from $10 to $10.50, while prices rise by 8%. Did the worker keep up with inflation?

Step 1: Find the wage increase percent.

\(\dfrac{10.50 - 10}{10} \times 100\% = \dfrac{0.50}{10} \times 100\% = 5\%\).

Step 2: Compare the results.

The wage rose by \(5\%\), but prices rose by \(8\%\).

Step 3: Interpret.

Because \(5\% < 8\%\), the worker did not keep up with inflation.

The worker earns more money in dollars, but that money has less buying power than before.

As we saw earlier in [Figure 1], changing prices can make the same paycheck feel very different from one year to another. This is one reason workers, families, and governments all pay attention to inflation.

Inflation changes the way households spend money. Families often divide spending into needs, such as food, housing, and transportation, and wants, such as entertainment or extra purchases. When prices rise, more of a budget may have to go toward needs. That leaves less money for wants.

This can change consumer behavior in market economies. Shoppers may compare prices more carefully, choose store brands, delay large purchases, or buy less. Businesses respond too. If customers pull back, companies may lower prices, offer sales, or redesign products to be cheaper to make.

Taxes also matter because they affect how much money consumers actually have to spend. Sales taxes increase the final price of purchases, and income taxes reduce take-home pay. In both early American history and modern life, taxes influence decisions about what people buy, what they avoid, and how much they can save.

Small price increases can feel minor at first, but repeated increases across food, fuel, clothing, and housing can add up to a major budget squeeze over time.

Inflation does not affect all families equally. A family already spending most of its income on necessities may feel inflation more sharply than a wealthier family with more room in its budget. That is why price changes are both an economic issue and a personal decision-making issue.

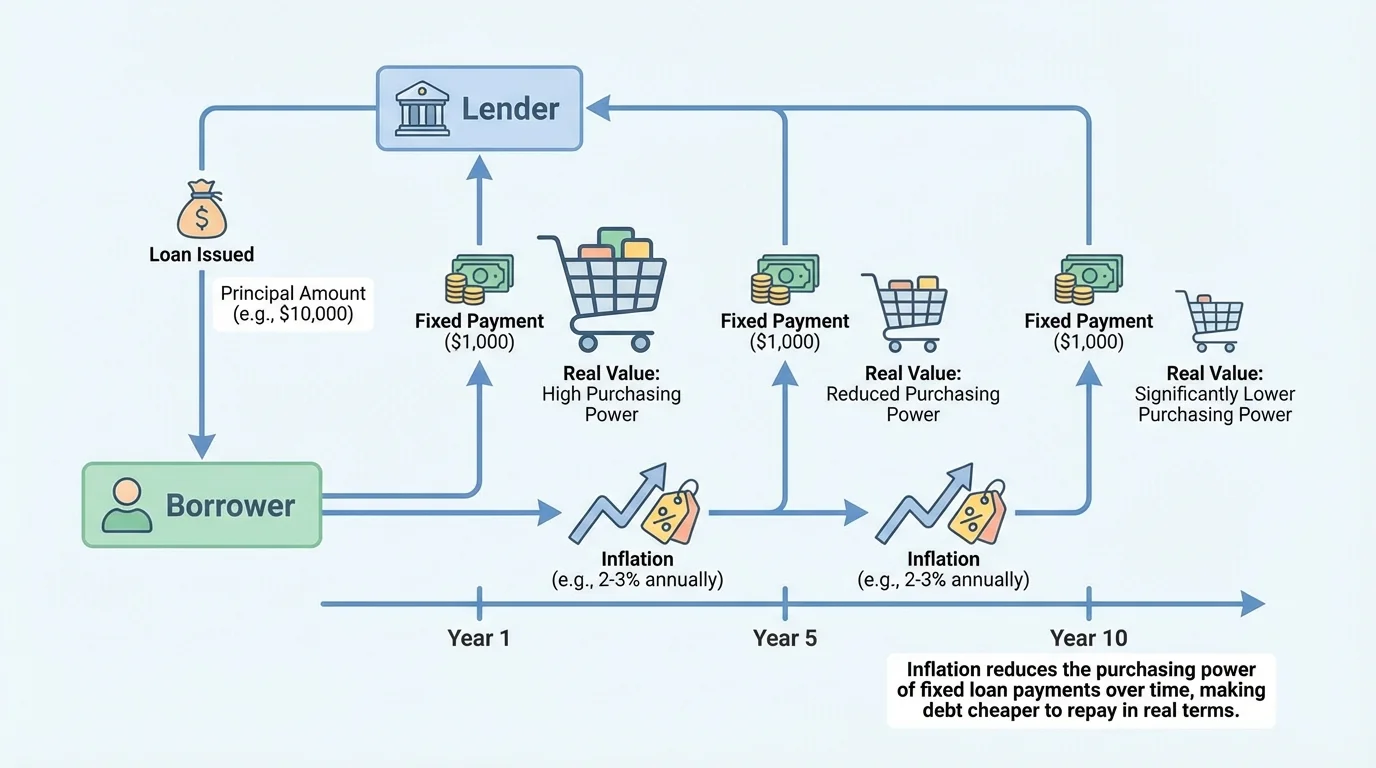

Borrowing means using money now and paying it back later, usually with interest. As [Figure 2] shows, inflation matters here because the dollars paid back in the future may not have the same value as the dollars borrowed today. This relationship helps explain why inflation can sometimes make fixed loan payments feel easier over time.

If someone borrows $1,000 with a fixed payment plan, the amount written in the loan contract does not change. But if wages and prices rise during the loan period, each later payment may take a smaller share of the borrower's income. In that sense, inflation can help borrowers with fixed-rate debt. However, lenders know this risk, so they often charge interest to protect themselves.

There is also a difference between the interest rate written on a loan and the loan's real cost after inflation. A high inflation rate can reduce the real burden of paying back a fixed amount. A low inflation rate means future dollars keep more of their value, so repayment feels heavier in real terms.

Worked example: finding total repayment on a simple loan

A student borrows $500 and must repay the loan plus 10% interest. How much must be repaid?

Step 1: Find the interest amount.

\(10\%\) of $500 is \(0.10 \times 500 = 50\).

Step 2: Add the interest to the amount borrowed.

\(500 + 50 = 550\).

Step 3: State the result.

The total amount to repay is $550.

If prices and wages rise during the time of the loan, that $550 may feel different at repayment than it did when the money was first borrowed.

Borrowing still carries risks. If a recession causes job loss or lower work hours, even fixed loan payments can become hard to manage. That is why people should think not only about interest rates, but also about economic conditions and income stability.

Saving protects money for future use, while investing tries to grow money over time. The challenge is that inflation reduces the value of money that sits still. If a person hides cash in a drawer for years, the number of dollars stays the same, but the buying power usually falls.

This is why people pay attention to real return. Real return is the gain on savings or investments after accounting for inflation. If a savings account earns 2% interest but prices rise by 4%, the saver is losing buying power, even though the account balance is increasing.

Percent change helps compare growth and loss. The same basic math can compare prices, wages, taxes, savings growth, and investment gains.

Investing can sometimes help money grow faster than inflation, but it also involves risk. Stocks, bonds, and businesses can rise or fall in value. Young people do not need to master every investment type yet, but they should understand the basic rule: money should be judged by what it can buy later, not just by the number printed on a statement.

Worked example: estimating real gain after inflation

An account grows from $200 to $212 in one year, while inflation is 4%. Did the account keep ahead of inflation?

Step 1: Find the account growth rate.

\(\dfrac{212 - 200}{200} \times 100\% = \dfrac{12}{200} \times 100\% = 6\%\).

Step 2: Compare growth to inflation.

The account grew by \(6\%\), while inflation was \(4\%\).

Step 3: Interpret the result.

Because \(6\% > 4\%\), the account stayed ahead of inflation.

The saver had a positive real gain in buying power.

A useful shortcut for simple comparisons is to subtract inflation from the gain rate. Here, \(6\% - 4\% = 2\%\), so the real gain is about \(2\%\). This is a simplified estimate, but it works well for understanding the idea.

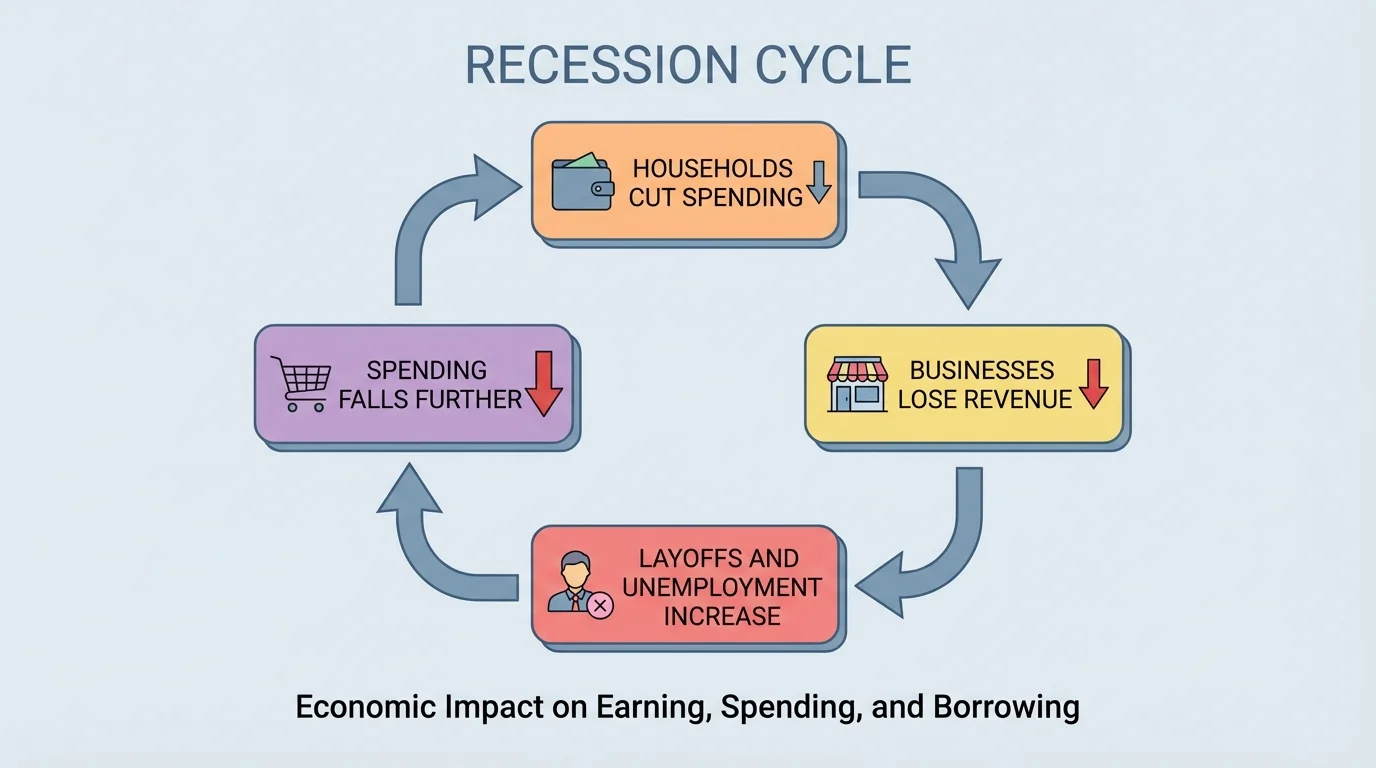

As [Figure 3] illustrates, a recession affects families through a chain reaction. When people worry about jobs or income, they often spend less. When spending falls, businesses earn less revenue. Businesses may then cut worker hours, delay expansion, or lay off employees. Those workers then spend less too, which can deepen the slowdown.

In a recession, prices do not always rise quickly. Sometimes inflation slows down, and some prices may even fall. But that does not automatically make life easier. A lower price matters less if someone has lost a job or seen wages cut.

Recessions change financial decisions in important ways. Families may avoid new debt, build emergency savings, or postpone major purchases. Businesses may reduce hiring. Governments may collect less tax revenue because incomes and sales are lower, which can make public budgeting harder.

Why recession and inflation feel different

Inflation usually hurts by making money buy less. Recession usually hurts by making income less certain. Sometimes both happen close together, which creates especially difficult choices for workers, consumers, and governments.

The recession cycle in [Figure 3] also helps explain why confidence matters in economics. If people expect hard times, they may cut spending early, and that can help cause the slowdown they fear.

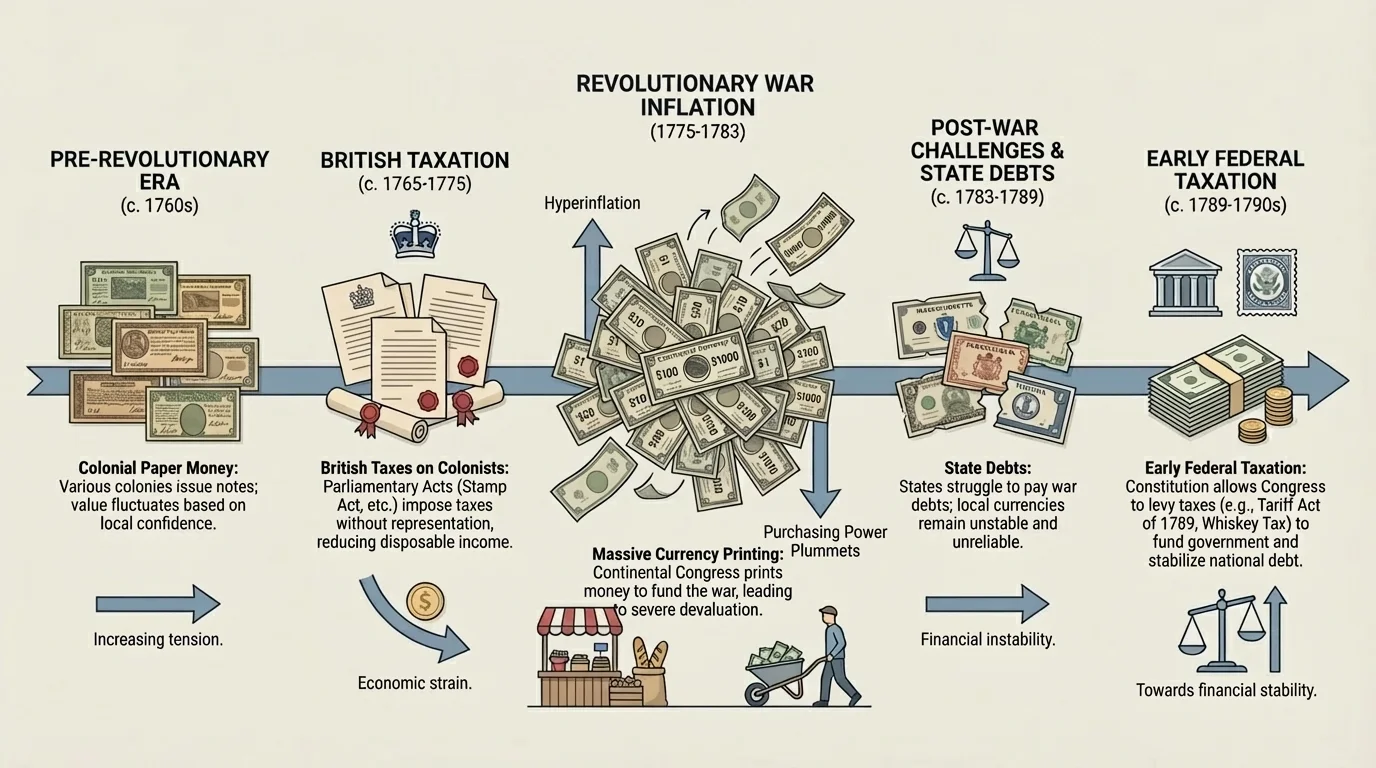

As [Figure 4] shows across a short historical timeline, questions about the value of money are not new. In early American history, colonists and the new United States faced shortages of coins, disagreements over taxes, war debts, and unstable paper money. These problems shaped consumer decisions and government policy from the colonial period into the early republic.

Before independence, many colonists objected to British taxes such as the Stamp Act and the Townshend Acts. Taxes changed what people bought and whether they bought imported goods at all. Some colonists responded with boycotts, choosing not to buy British products. That was both a political act and a consumer decision in a market economy.

During and after the Revolutionary War, governments printed paper money to help pay for war costs. When too much paper money circulated without enough confidence behind it, prices rose sharply. People sometimes lost trust in that money because it did not hold value well. This is one historical example of inflation hurting ordinary earners and savers.

After the war, debt remained a major issue. Farmers, merchants, soldiers, and governments all dealt with borrowing and repayment. Some debtors struggled because they owed fixed amounts while income was uncertain. Debates over taxation and federal financial power became central in the early republic because leaders needed ways to manage debt, support trade, and build trust in the nation's economy.

Seen this way, early American history is also a history of financial literacy. People had to judge whether money was reliable, whether taxes were fair, whether debt was manageable, and whether goods were worth buying. The same broad questions still matter now, even though the specific products and policies have changed.

"A penny saved is a penny earned."

— Benjamin Franklin

Franklin's famous saying connects directly to changing money value. Saving matters, but if inflation is high, saving alone may not protect buying power unless the money also grows over time.

Consider a colonial merchant who pays a tax on imported tea. The tax raises the final selling price. Consumers then must decide whether to buy the tea, switch to another product, or refuse to buy on principle. That is a clear example of taxes shaping market behavior.

Now consider a modern family choosing whether to finance a car during a period of high inflation. If wages are rising and the loan has a fixed rate, the future payments may feel lighter. But if a recession arrives and someone loses work, the same loan can become a burden. Economic conditions change the meaning of the same financial decision.

| Situation | Main Effect on Money | Likely Consumer Response |

|---|---|---|

| Prices rise quickly | Buying power falls | Compare prices, cut optional spending |

| Wages rise slower than prices | Real income falls | Delay purchases, revise budget |

| Fixed-rate loan during inflation | Future payments may feel lighter | Borrowing may seem easier, but risk remains |

| Recession | Income becomes less certain | Save more, borrow less, postpone major purchases |

| New tax on goods | Final price rises | Buy less, substitute goods, protest or boycott |

Table 1. Comparison of how different economic conditions affect money and consumer decisions.

Notice that no single rule solves every situation. A person needs to ask: Are prices rising? Are wages rising too? Is my income secure? What taxes apply? Is the interest rate fixed or variable? Will this decision still make sense if the economy weakens?

Understanding money over time helps people make wiser choices. Earners should compare wage increases to inflation. Shoppers should notice whether rising prices are changing their budget. Borrowers should ask whether they can repay a loan even if the economy weakens. Savers and investors should think about whether their money is growing faster than inflation.

These decisions are part of life in a market economy, where consumers, businesses, and governments constantly interact. Taxes can encourage or discourage certain purchases. Inflation can reshape budgets. Recessions can reduce income and confidence. History shows that these are not new problems; they have been part of American economic life since the beginning.

When students learn to calculate percent change and connect it to real life, they gain more than a math skill. They gain a tool for judging earnings, prices, taxes, debt, and future plans. Whether looking at a colonial boycott, a family grocery budget, or a savings account, the key idea stays the same: money's value is not fixed. It changes with time, prices, and economic conditions.