Choosing a lower monthly payment can sometimes lead to one of the most expensive financial outcomes a person faces. That sounds backward, but it is often true. When people choose between leasing and purchasing a car, a home, or another major item, the decision is not just about what feels affordable this month. It is about what happens over months and years: who owns the item, who takes the risk, who builds value, and how much money leaves your budget in total.

Big purchases shape personal finances because they affect budget, saving, borrowing, insurance, and future choices. A teenager comparing first-car options, a family deciding whether to rent or buy a home, or a business owner choosing equipment all face the same basic question: is it better to pay for temporary use or to pay for ownership?

Leasing and buying are both legal agreements for using something valuable, but they work very differently. A person who buys usually works toward ownership. A person who leases usually pays for the right to use the item for a set period of time. This difference affects flexibility, long-term cost, and wealth-building.

For example, a car buyer may make payments for several years and then own the car outright. A car lessee may make lower payments during the same period, but at the end of the lease the car is returned unless the contract allows a buyout. With housing, people usually do not use the word "lease" in everyday conversation. Instead, they say renting. But financially, renting a home is still a form of leasing: the tenant pays for the right to use the property for a limited time.

Lease means a contract that allows someone to use a car, home, or other item for a set time in exchange for payments, usually without ownership at the end.

Purchase means buying an item, either with cash or borrowed money, in order to own it.

Down payment is an upfront amount paid at the beginning of a purchase.

Equity is the portion of a property or asset that a person truly owns.

Depreciation is the loss of value over time, especially important for automobiles and technology.

These terms matter because the smartest choice is not always the one with the cheapest monthly payment. A decision should be based on total cost, expected use, financial stability, and long-term goals.

Three ideas help explain almost every lease-versus-buy choice. First is depreciation. Many big purchases, especially cars and electronics, lose value as they age. Second is equity. When a person buys a home or pays off a loan, part of that spending can build ownership. Third is opportunity cost, which is what you give up by choosing one option over another. Money used for a big down payment cannot be used somewhere else, such as saving or investing.

Consumers also need to compare visible costs and hidden costs. A visible cost might be a monthly payment. A hidden cost might be extra lease fees, repair requirements, interest, property taxes, insurance, or penalties for ending a contract early. Strong consumer skills mean reading beyond the advertised number.

A new car often loses value quickly in its first years. That is one reason leased cars may seem cheaper each month: the contract is often designed around the period when depreciation is greatest.

In general, leasing tends to favor short-term use and flexibility, while purchasing tends to favor long-term ownership and value retention. But that pattern changes depending on the item and the contract details.

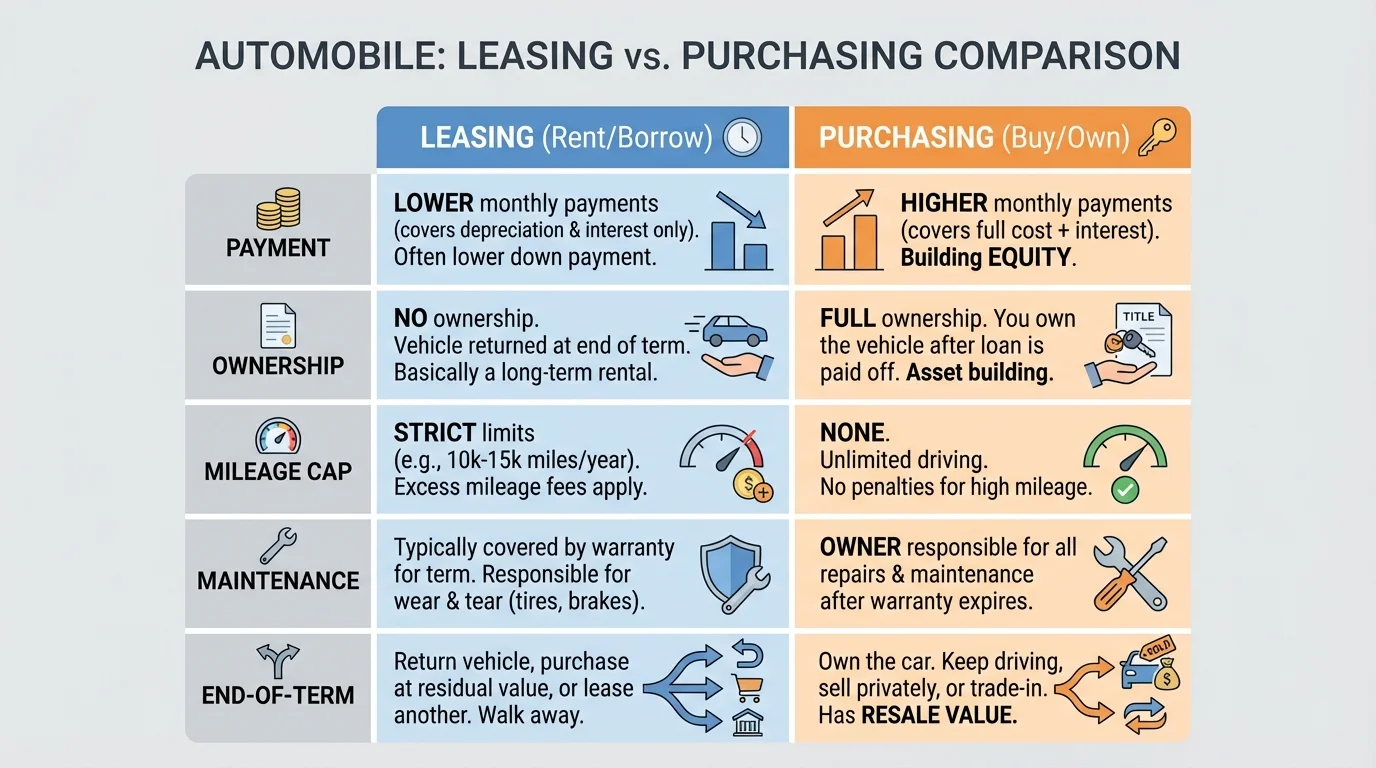

With automobiles, the trade-off is especially clear, as [Figure 1] shows through the contrast between lower short-term payments and long-term ownership. A car lease usually lasts for a fixed period, often about two to four years. The driver makes monthly payments to use the car, but does not automatically own it at the end. A purchase means paying cash or taking out an auto loan and making payments until the loan is paid off.

Leasing a car often has several advantages. Monthly payments are frequently lower than loan payments for the same car. A leased car may be newer, have modern safety features, and still be under warranty, which can reduce repair costs for a while. Leasing may appeal to people who want a new car every few years or who do not want to commit to long-term ownership.

However, leasing a car also has important disadvantages. Many leases include mileage limits. If a driver goes over the limit, extra fees may apply. Leases may also charge for unusual wear and tear. Ending a lease early can be expensive. Most importantly, after years of payments, the driver may own nothing unless they pay an additional buyout price.

Buying a car has different strengths. The biggest advantage is ownership. Once the loan is fully paid, the owner can continue driving the car without monthly loan payments. The car can also be sold or traded in later, which means it still has some value. Buyers are generally not restricted by mileage limits in the same way leaseholders are.

The disadvantages of buying usually appear earlier in the process. Loan payments may be higher than lease payments. Buyers often need a larger down payment. They also take on the risk that the car may lose value quickly. If the car's value falls faster than the loan balance, the borrower may owe more than the car is worth. This is sometimes called being "upside down" on the loan.

Maintenance matters too. A leased car may be cheaper to repair at first because it is newer, but a buyer who keeps a car for many years may save money overall by avoiding endless lease cycles. In that way, [Figure 1] highlights a key point: leasing can reduce short-term cost, while buying can reduce cost over a long period if the car is kept after the loan ends.

| Option | Common Advantages | Common Disadvantages |

|---|---|---|

| Lease a car | Lower monthly payments, newer vehicle, possible warranty coverage, easier short-term flexibility | No ownership, mileage limits, wear fees, early termination penalties |

| Buy a car | Ownership, no mileage cap, can sell later, long-term value after loan payoff | Higher monthly payments, depreciation risk, repair costs as car ages, possible larger down payment |

Table 1. Comparison of common advantages and disadvantages of leasing and buying an automobile.

Example: Comparing total automobile payments

A student's family is choosing between leasing and buying the same car for three years.

Step 1: Find the total lease cost.

The lease requires $299 per month for 36 months and a $2,000 amount due at signing.

The payment total is $299 multiplied by 36, which is \(299 \times 36 = 10,764\).

Total lease cost is $10,764 plus $2,000, so \(10,764 + 2,000 = 12,764\).

Step 2: Find the total loan payments over the same period.

The purchase loan requires $410 per month for 36 months and a $3,000 down payment.

The payment total is \(410 \times 36 = 14,760\).

Total paid over three years is \(14,760 + 3,000 = 17,760\).

Step 3: Compare what each option leaves the family with.

After three years, the lease ends and the car is returned unless bought out. After three years of loan payments, the family still has a car with resale value.

The lease costs less during the three-year period, but the purchase may create more long-term value because the family is paying toward ownership.

This example shows why consumers should ask not only, "Which option costs less now?" but also, "What do I have when the payments stop?"

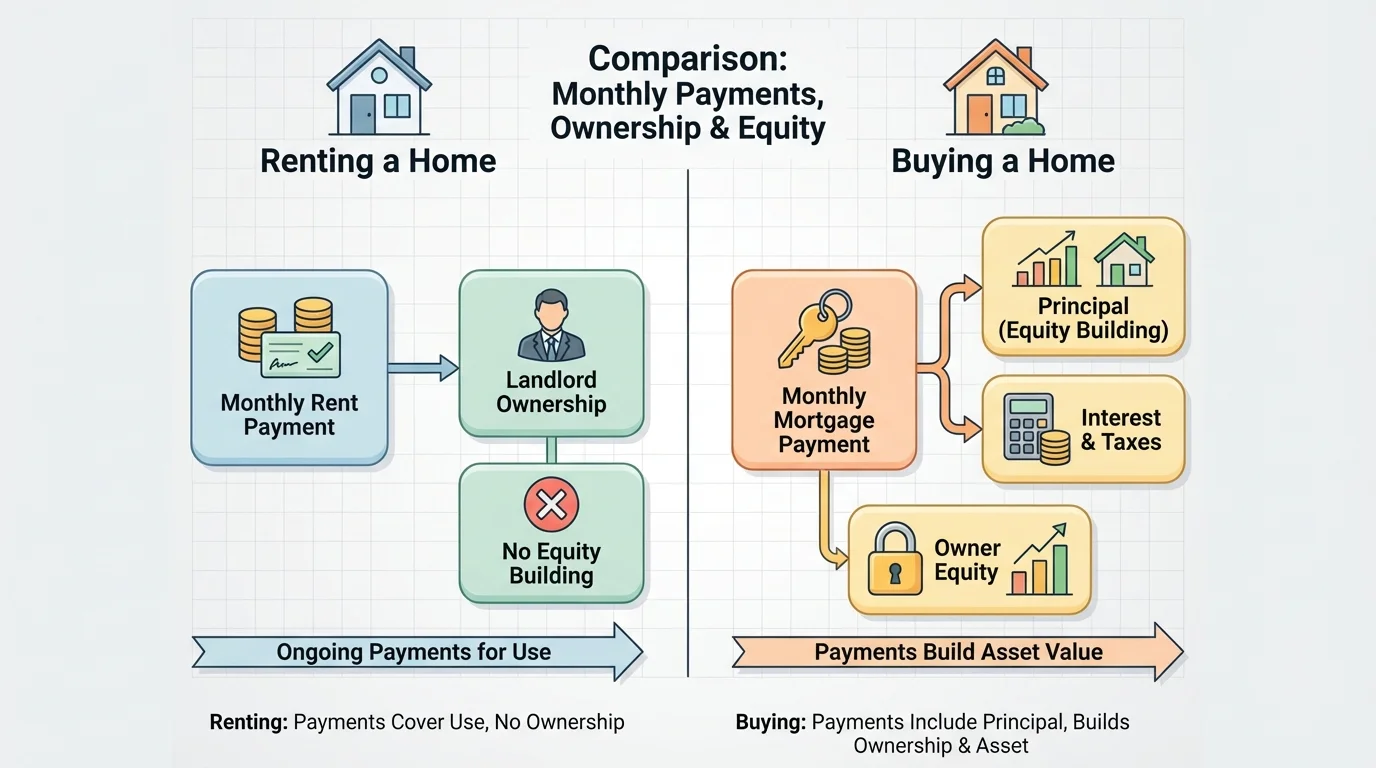

Housing choices shape both daily life and long-term wealth, and [Figure 2] illustrates that the difference between renting and buying is really a difference between paying for use and building ownership. In housing, leasing usually means renting. A renter signs a lease agreement for an apartment or house and pays monthly rent to live there for a set term. A buyer purchases a home, usually with help from a mortgage, which is a long-term loan used to buy property.

Renting has clear advantages. It usually requires less money upfront than buying a home. Renters often avoid large repair bills because major maintenance may be the landlord's responsibility. Renting can also provide mobility. If a student's family may move for a job in a year, renting can be more practical than buying and then quickly reselling.

But renting also has disadvantages. Monthly rent payments do not build ownership in the property. Rent may increase over time. The renter usually has less control over the property, including rules about pets, remodeling, or long-term changes. When the lease ends, the renter may need to move or sign a new agreement at a different price.

Buying a home offers the possibility of stability and equity. Part of each mortgage payment may reduce the loan principal, increasing the owner's share of the home. If the home value rises, the owner may gain financially. Owners can also make more decisions about the property, such as renovations or landscaping, as long as local laws and neighborhood rules are followed.

However, buying a home also has major costs and risks. Buyers often need a down payment, closing costs, property taxes, homeowners insurance, and money for repairs. If home values fall or the owner must move suddenly, selling may be difficult. Homeownership can build wealth, but it also requires responsibility and financial stability.

A mortgage payment itself may contain different parts. A simplified way to think about it is: one part pays interest to the lender, and another part pays down the loan balance. As that balance falls, the owner's equity grows. Over time, this is one reason buying can be powerful. As [Figure 2] shows, rent usually flows entirely to the property owner, while mortgage payments can gradually increase the buyer's ownership stake.

| Option | Common Advantages | Common Disadvantages |

|---|---|---|

| Rent a home | Lower upfront cost, flexibility, fewer repair responsibilities, easier to move | No equity, possible rent increases, less control, no ownership |

| Buy a home | Equity growth, stability, ownership, possible value appreciation | High upfront costs, repair responsibility, taxes and insurance, less flexibility if moving |

Table 2. Comparison of common advantages and disadvantages of renting and buying a home.

Why equity changes the housing decision

When people rent, they are paying for a place to live. When they buy, they are paying both for shelter and for an ownership claim in the property. That does not mean buying is always better. It means the decision includes an investment element that renting usually does not. A person who plans to stay in one place for many years may benefit more from building equity than a person who expects to move soon.

For teenagers, one useful lesson is that housing costs are not just "rent versus mortgage." They also include utilities, maintenance, insurance, and unexpected expenses. A smart budget must consider all of them.

The same ideas apply to furniture, appliances, computers, musical equipment, farm equipment, and business tools. Some stores advertise "lease-to-own" programs. These can look attractive because the initial payment is small. But consumers must read carefully. In some cases, the total amount paid over time is much higher than the cash price.

A store might offer a laptop for $900 if purchased today, or for $55 per month over 24 months through a lease-to-own plan. The total paid would be \(55 \times 24 = 1,320\). That means the customer pays $420 more than the cash price, not counting extra fees. For some consumers, spreading out payments may be necessary, but it is still important to recognize the higher total cost.

Example: Lease-to-own furniture

A couch has a cash price of $1,200. A lease-to-own contract charges $70 per month for 24 months.

Step 1: Calculate the total paid.

Multiply the monthly payment by the number of months: \(70 \times 24 = 1,680\).

Step 2: Compare total paid with the cash price.

The difference is \(1,680 - 1,200 = 480\).

Step 3: Interpret the result.

The customer pays $480 more than the cash price in exchange for paying over time.

This may be useful for someone who cannot pay upfront, but it is more expensive overall.

Businesses and farmers sometimes lease equipment because technology changes quickly or because repairs and replacement are easier under a lease contract. But when an item will be used for many years and kept in good condition, purchasing may be more cost-effective.

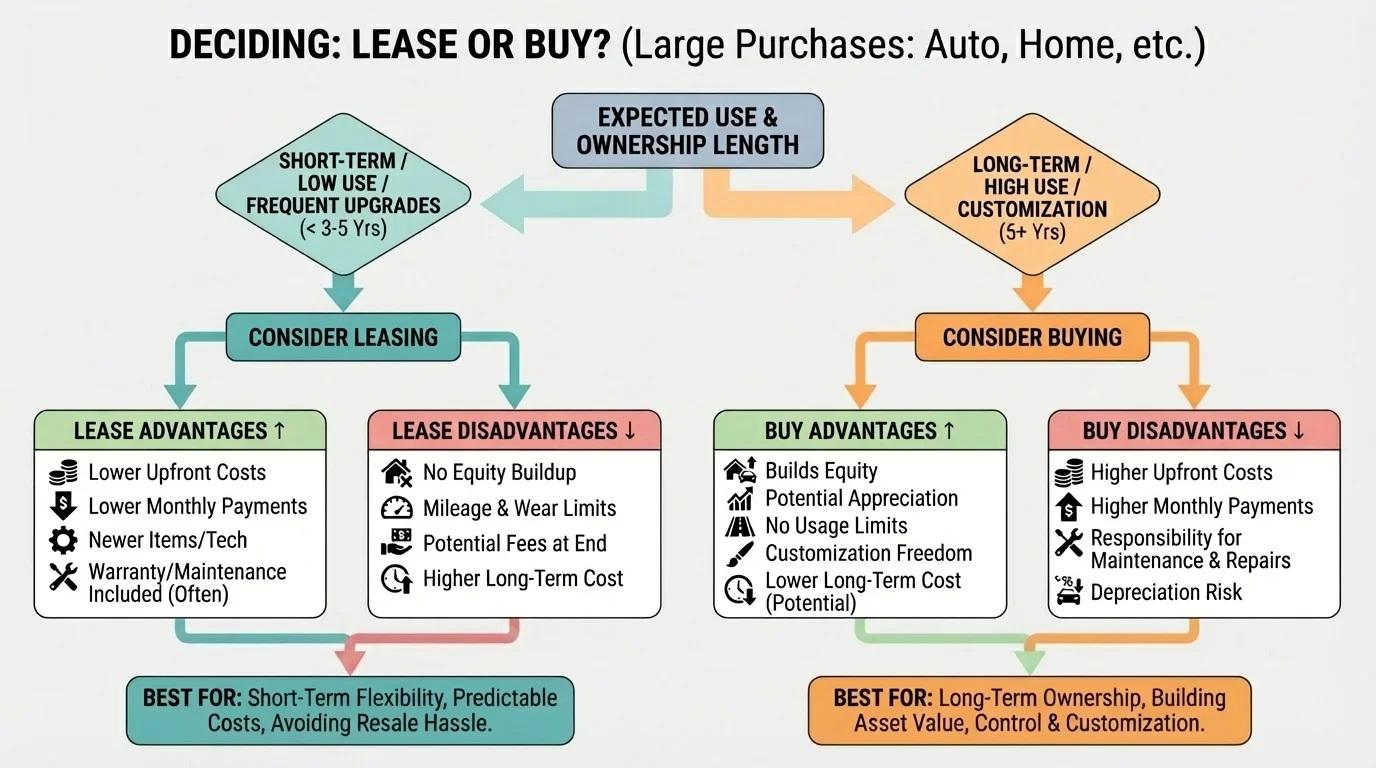

No single rule always tells a consumer whether to lease or buy, and [Figure 3] presents a decision process that helps compare the options logically. The key is to examine the full agreement, not just the advertised monthly amount.

One useful comparison is total paid over the period you expect to use the item. For a lease, this may include monthly payments, upfront fees, security deposits, mileage charges, maintenance rules, and end-of-term fees. For a purchase, this may include the down payment, loan payments, interest, taxes, insurance, and repair costs. Then compare that total with what you own at the end.

A simple way to organize the thinking is this: short-term affordability versus long-term value. Leasing often wins on short-term affordability. Buying often wins on long-term value if the item is kept long enough.

Another factor is how long you expect to keep the item. If someone uses a car for only two years, leasing may fit their situation. If they expect to use a car for eight years, purchasing may be the better financial choice. [Figure 3] makes this easier to see by connecting the decision to time horizon, amount of use, and desire for ownership.

Example: Comparing home costs over one year

A family can rent an apartment for $1,400 per month or buy a small home with a monthly mortgage payment of $1,650. The home also requires $2,400 per year in property taxes and insurance, and about $1,200 per year in maintenance.

Step 1: Find the annual rent cost.

Annual rent is \(1,400 \times 12 = 16,800\).

Step 2: Find the annual home payment cost.

Annual mortgage payments are \(1,650 \times 12 = 19,800\).

Step 3: Add other annual home costs.

Taxes, insurance, and maintenance total \(2,400 + 1,200 = 3,600\).

Total annual housing cost for buying is \(19,800 + 3,600 = 23,400\).

Step 4: Compare.

Buying costs $23,400 for the year, while renting costs $16,800 for the year.

Renting costs less in this one-year comparison, but buying may still make sense if the family stays longer and builds equity.

Consumers should also ask whether the contract allows a buyout, who pays for damage, whether insurance requirements differ, and what penalties apply for late or early payments.

The best choice depends on a person's situation. A consumer should consider how stable their income is, how long they plan to use the item, how much cash they have for a down payment, and how comfortable they are with maintenance costs.

A person who values flexibility may prefer leasing or renting. A person focused on long-term ownership may prefer buying. Someone with uncertain job plans may avoid purchasing a home because moving can be costly. Someone who drives long distances every week may avoid leasing a car because mileage fees could become expensive.

Credit matters too. Interest rates on loans affect the cost of purchasing. Poor credit can make borrowing more expensive, which may change the comparison. At the same time, some lease or rent agreements may include strict requirements or high fees that also make them costly.

Good budgeting means looking at both fixed and variable costs. A monthly payment is only one part of a major purchase. Insurance, fuel, taxes, maintenance, repairs, and fees must also fit within the budget.

Another important factor is emotional pressure. Advertisements often focus on what seems affordable each month, not on the full amount paid. Smart consumers slow down, compare contracts, and ask questions before signing.

One common mistake is choosing based only on monthly payment. A lower payment does not necessarily mean a better deal. A long contract, extra fees, or lack of ownership can make a lower monthly cost more expensive overall.

Another mistake is ignoring the end of the agreement. At the end of a car lease, the driver may need to return the vehicle, pay fees, or decide whether to buy it. At the end of a rental agreement, the tenant may face a rent increase or relocation. At the end of a purchase loan, however, the buyer may own the item free and clear.

Consumers should also read the details carefully: mileage limits, maintenance rules, interest rates, security deposits, penalties, and cancellation terms. Comparing at least two or three options is a wise habit. For example, comparing a used-car purchase, a new-car lease, and a different used-car loan may reveal that the most advertised option is not the best value.

"The cost of something is what you give up to get it."

— A core economic idea

That idea applies directly here. Leasing may give up ownership in exchange for flexibility and lower short-term payments. Purchasing may give up some flexibility in exchange for ownership and potential long-term savings.

Leasing is often strongest when a person needs short-term use, wants lower payments now, expects to move, or prefers less commitment. Purchasing is often strongest when a person wants ownership, plans to keep the item for a long time, and can manage upfront and maintenance costs.

Neither choice is automatically right or wrong. The wise consumer compares total cost, contract terms, lifestyle needs, and future goals. Financial literacy means seeing beyond the sales pitch and understanding the trade-offs clearly.