One of the most surprising ideas in economics is that a market can be both powerful and imperfect at the same time. Markets coordinate millions of decisions every day: what to produce, how much to charge, and who gets what. Yet even when buyers and sellers are acting rationally, markets can still produce too much pollution, too little education, prices that are too high under monopoly, or services like national defense that private firms have little reason to provide. That gap between what markets do and what society needs is where government intervention becomes important.

In a mixed economic system, most production and exchange happen through markets, but government also plays a major role. It writes and enforces laws, protects property, regulates firms, provides public services, redistributes income, and responds when markets fail. The big question is not whether government should play a role in the economy. The real question is when intervention improves outcomes and when it creates new problems.

A market failure happens when the market, left on its own, does not allocate resources efficiently. In simple terms, society could be made better off if output, prices, or distribution changed. Economists often connect efficiency to the idea that resources should go where they create the greatest total benefit. If a market produces too little of something valuable or too much of something harmful, it is not reaching the best outcome.

Market failure is a situation in which a free market does not produce the socially optimal amount of a good or service.

Efficiency means resources are used in a way that maximizes total benefits relative to total costs.

Equity refers to fairness in how income, wealth, opportunities, or access to goods and services are distributed.

Some market failures happen because firms gain too much power. Others happen because some costs or benefits spill onto people who are not part of a transaction. In still other cases, markets fail because nobody can be easily excluded from using a good, so private firms cannot collect enough payment to supply it. These problems help explain why even economies built on competition still need public rules and institutions.

Government intervention is not automatically good. Officials may have incomplete information, political pressure, or weak enforcement. Economists sometimes call this government failure, which means government action creates inefficiency or unintended harm. A thoughtful evaluation asks two questions at once: What is wrong with the market? and Will this policy actually improve it?

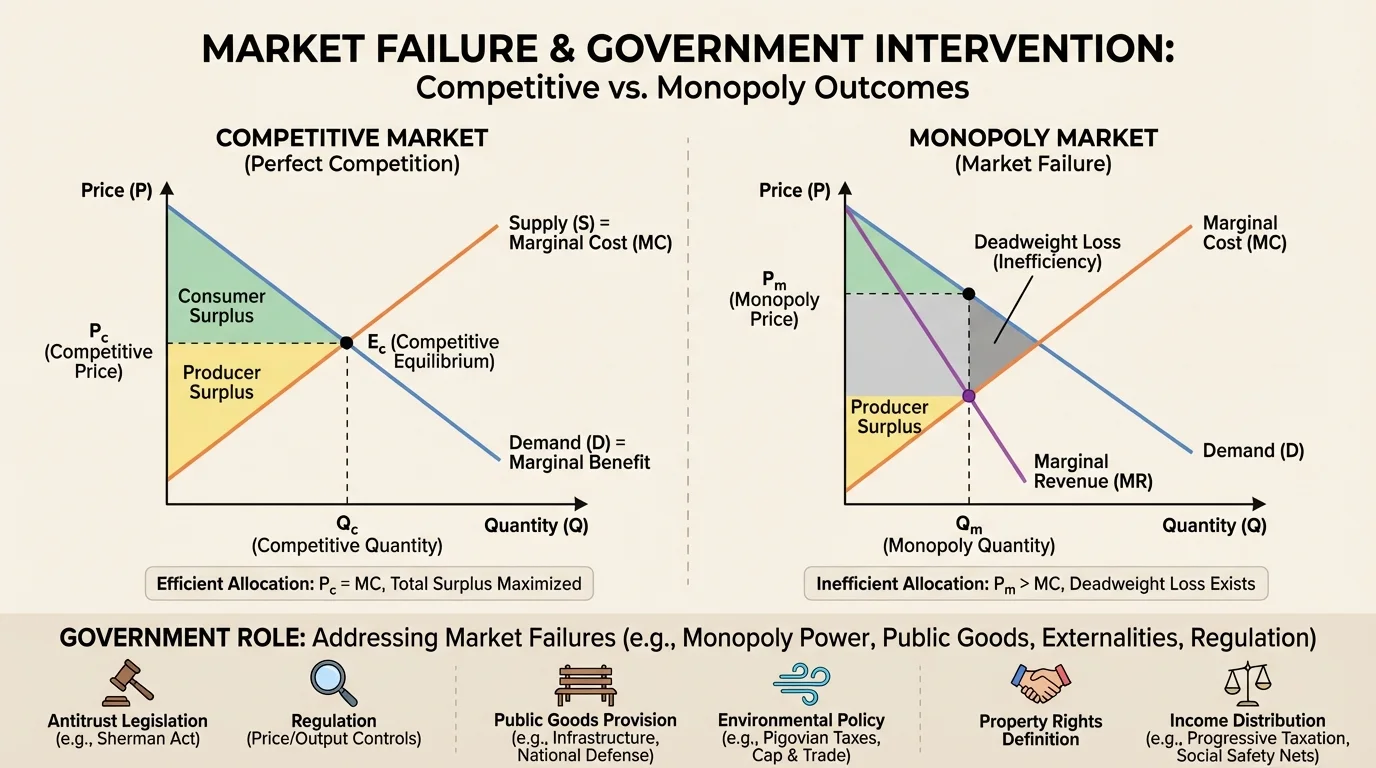

A monopoly exists when one seller dominates a market and faces little direct competition. Because the monopolist controls supply, it can often restrict output and charge a higher price than would exist in a competitive market. Consumers pay more, buy less, and have fewer choices. This is one reason economists worry about monopoly power: the firm may maximize its own profit without maximizing social welfare.

Monopolies can arise for several reasons. A company may own a key resource, hold an important patent, benefit from massive economies of scale, or face legal protections that keep rivals out. In some industries, especially utilities such as water or electricity distribution, one firm may be able to serve the market at lower cost than many competing firms. That situation is called a natural monopoly.

Because monopoly can harm consumers, governments use antitrust legislation to promote competition. Antitrust laws can block mergers that would reduce competition, break up firms that abuse market power, and punish practices such as price fixing. Price fixing happens when competing firms secretly agree to raise prices instead of competing. That turns a market that appears competitive into one that behaves more like a monopoly.

History provides powerful examples. In the early twentieth century, the U.S. government broke up Standard Oil because it had grown so dominant that it could crush rivals and control prices. More recently, governments around the world have investigated large technology companies over app stores, search engines, digital advertising, and data control. The details are modern, but the core issue is old: when one company becomes too powerful, the market may stop working competitively.

Still, not every large company is harmful. Some firms become big because they are innovative and efficient. That is why antitrust policy must be careful. It should protect competition, not punish success. As seen earlier in [Figure 1], the economic concern is not simply firm size, but whether market power leads to higher prices, lower output, reduced innovation, or barriers that block new entrants.

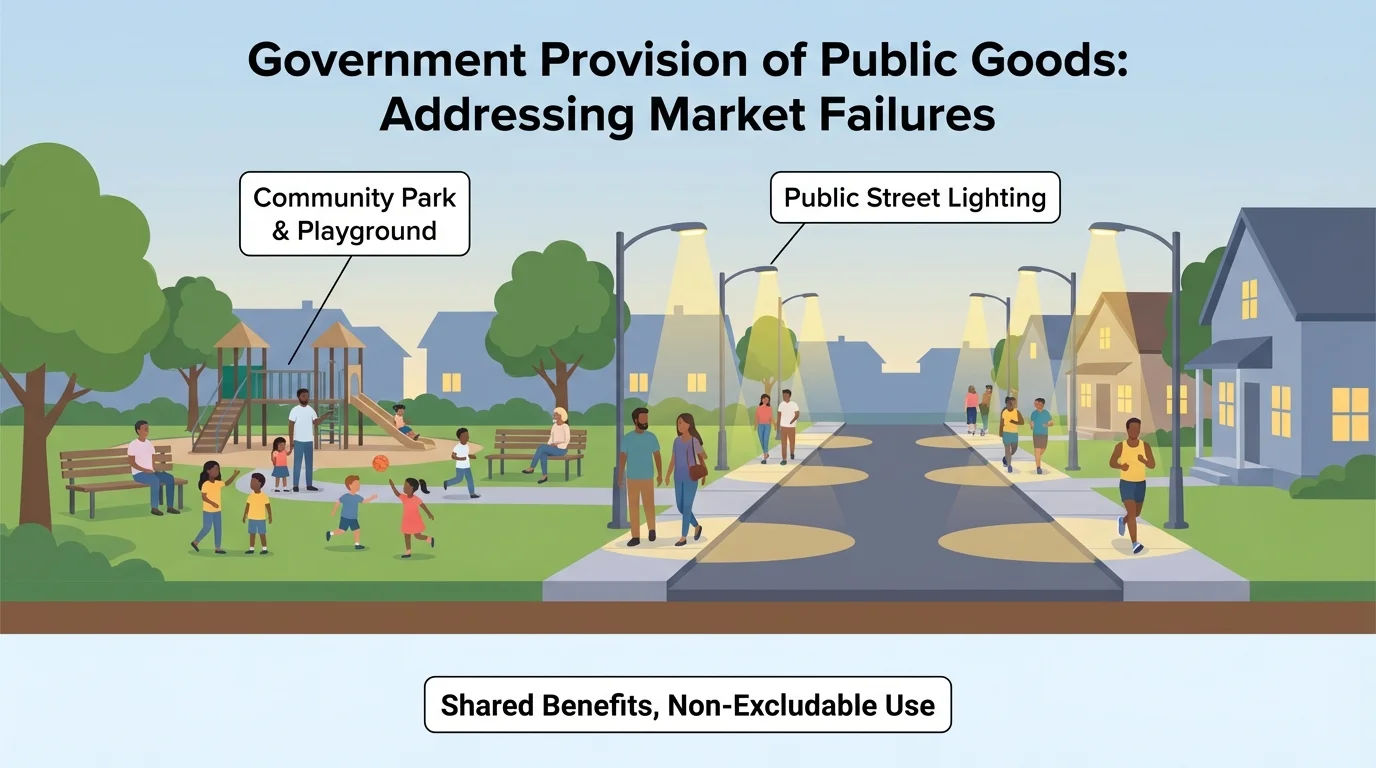

Some goods create a different problem. A public good is a good or service that is both nonrival and nonexcludable. Nonrival means one person's use does not significantly reduce another person's use. Nonexcludable means it is difficult or impossible to keep non-payers from benefiting. This creates the free-rider problem: people may enjoy the benefit whether or not they pay.

National defense is a classic example. If a country is defended from attack, all residents benefit. It would be extremely difficult to defend only those households that paid a fee. Street lighting, lighthouse signals, and some forms of flood control work in a similar way. Private firms often struggle to profit from public goods because too many people can free ride.

As a result, governments often provide or finance public goods using tax revenue. This does not mean every publicly funded service is a pure public good. A public school, for example, is valuable and publicly provided, but it is not perfectly nonrival or nonexcludable. Class size matters, and enrollment rules exist. Economists distinguish between pure public goods and services that government chooses to provide because they create large social benefits.

Public goods show why markets alone may underprovide something society clearly wants. The issue is not that people do not value the good. The issue is that the payment system breaks down. The neighborhood scene in [Figure 2] captures the logic: once lighting or public safety is available, many people can benefit at the same time, including those who did not directly pay.

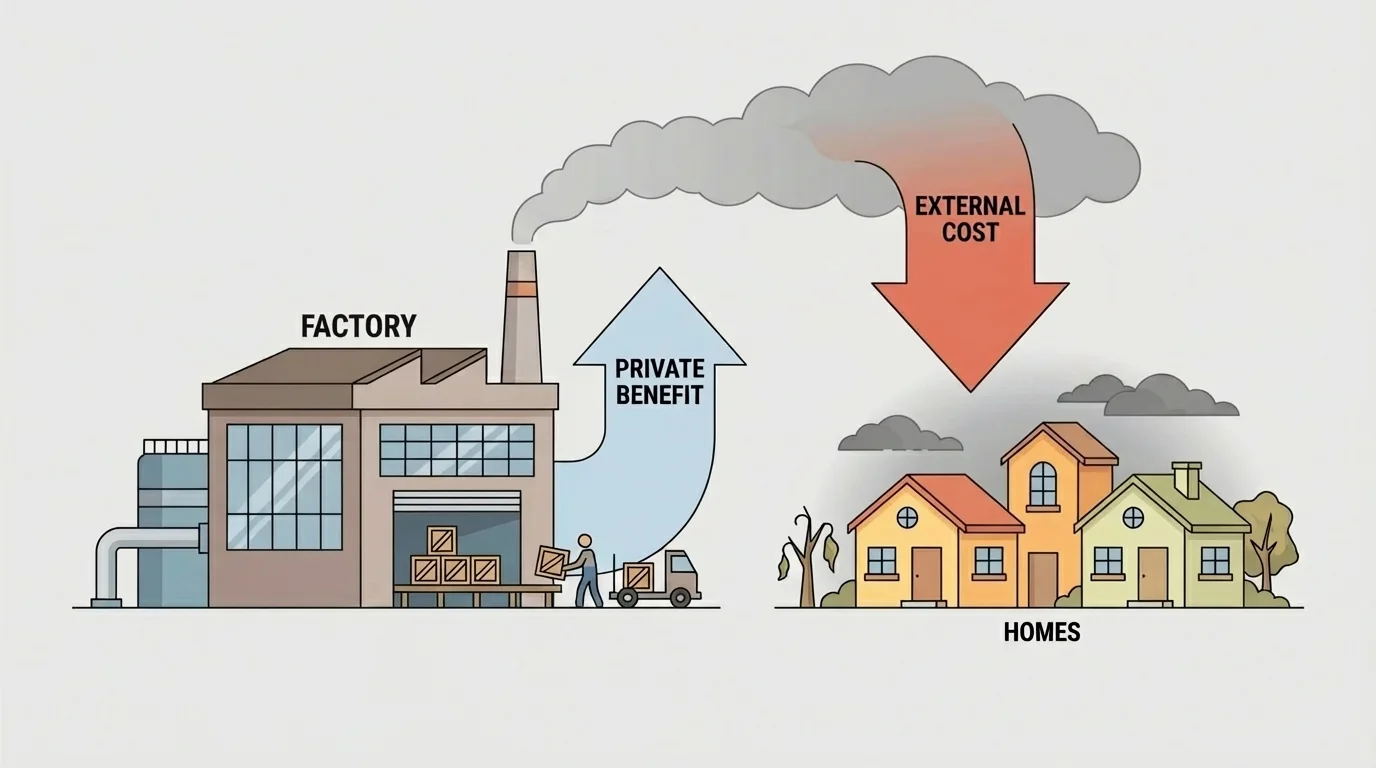

Sometimes a market transaction affects people who are not part of the exchange. That spillover is called an externality. If the spillover is harmful, it is a negative externality. If it is beneficial, it is a positive externality.

Pollution is the standard example of a negative externality. A factory that produces steel may earn profits and pay workers, but if it releases smoke or waste into the air or water, nearby families bear health and cleanup costs. Those outside costs are not fully included in the market price of steel. As a result, the market may produce too much steel from society's point of view.

Economists often compare private cost and social cost. Private cost is what the firm directly pays. Social cost includes private cost plus the external cost imposed on others. In simple form, \(\textrm{social cost} = \textrm{private cost} + \textrm{external cost}\). When social cost is greater than private cost, the market price is too low to reflect the true cost to society.

Governments can respond in several ways. They may set pollution limits, require cleaner technology, fine firms that violate standards, or impose a tax on the harmful activity. A tax designed to make firms account for an external cost is often called a Pigovian tax. If a factory pays for each ton of pollution, the firm has a stronger incentive to reduce emissions.

Positive externalities create the opposite problem: the market may produce too little. Vaccinations protect the person receiving the shot, but they also reduce the spread of disease to others. Education raises a student's future earnings, but it also benefits society through higher productivity, lower crime in many places, and greater civic participation. Because the social benefit is larger than the private benefit, governments often subsidize education, research, and public health.

Why taxes and subsidies change behavior

If an activity creates outside harm, a tax raises the private cost so decision-makers consider more of the true social cost. If an activity creates outside benefits, a subsidy lowers the private cost or increases the reward, encouraging more of that activity. The goal is to move production or consumption closer to the socially efficient level.

The factory example in [Figure 3] also explains why debates about pollution are often debates about hidden costs. When prices ignore asthma, contaminated water, or climate damage, the market signal is incomplete rather than neutral.

Environmental issues are among the clearest examples of market failure. Air and water pollution, deforestation, overfishing, and greenhouse gas emissions all involve costs spread across large groups of people and often across generations. A driver burning gasoline gains a private benefit from travel, but the released CO2 contributes to climate change, which affects people far beyond the individual purchase of fuel.

Governments use different tools to address environmental problems. Command-and-control regulation sets direct rules, such as maximum pollution levels or required technology. Market-based policies use incentives instead. A carbon tax charges for emissions. A cap-and-trade system sets an overall pollution cap and allows firms to buy and sell emission permits. In both cases, government tries to force environmental costs into economic decisions.

These policies involve trade-offs. Strict rules can protect health and ecosystems, but they may also raise prices or reduce jobs in some industries. On the other hand, weak rules may allow economic activity today while creating much larger costs later. Economics does not say the environment should be ignored for growth. It asks how to compare present benefits with future costs and how to design policies that reduce harm efficiently.

Air pollution has measurable economic effects beyond health. It can lower worker productivity, damage crops, and increase healthcare costs, which means environmental policy often affects output and living standards at the same time.

Environmental policy also raises questions of fairness. Low-income communities are often more exposed to pollution even though they may contribute less to the problem. This means environmental policy is not only about efficiency but also about who bears costs and who receives protection.

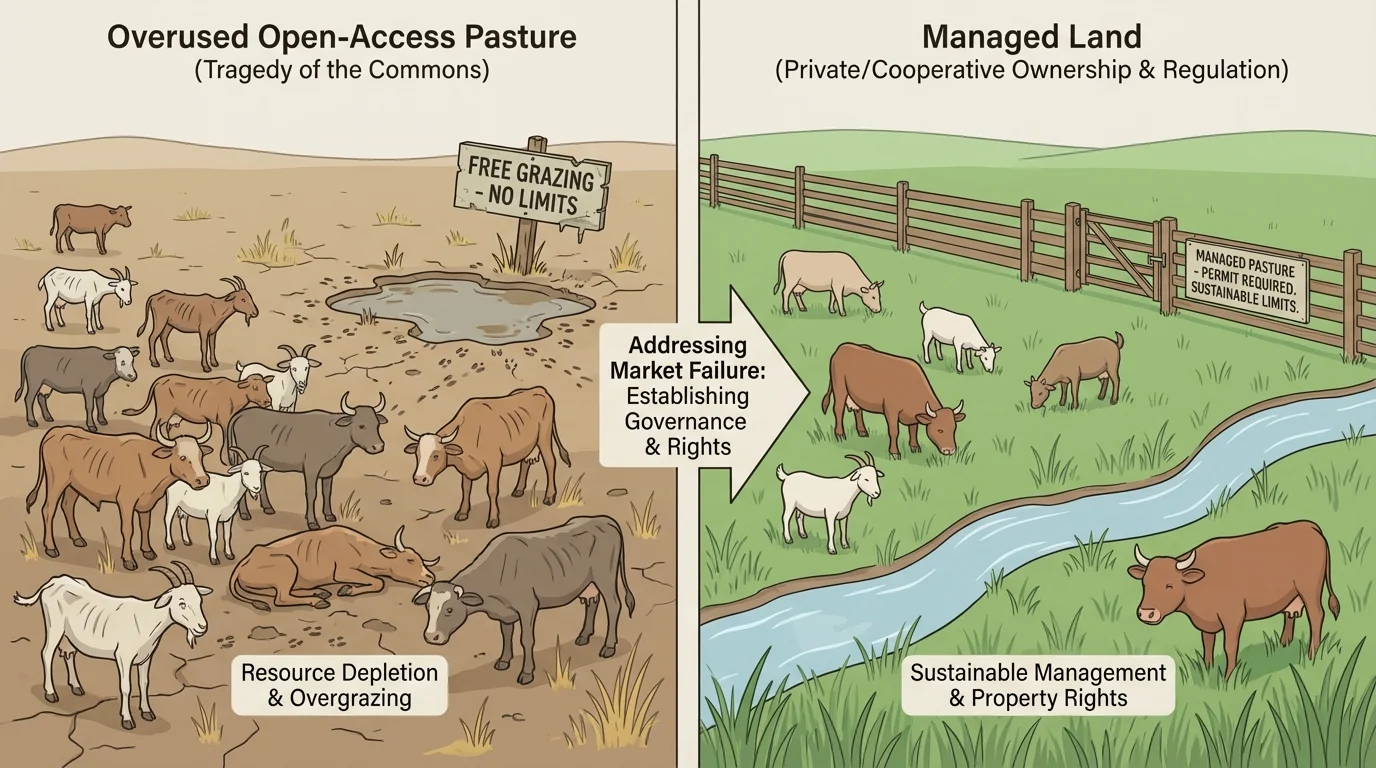

Markets depend on rules. Clear property rights tell people what they own, what they may use, and how they can transfer it. Without secure ownership and enforceable contracts, buyers and sellers face uncertainty, investment becomes risky, and trade slows down. Resources that belong to everyone in an undefined way can be overused because each person has an incentive to grab benefits before someone else does.

This problem is often called the tragedy of the commons. If no one owns a pasture, each herder may add more cattle because the personal gain is private while the overgrazing cost is shared by all. The result is depletion. Similar problems can occur with fisheries, groundwater, forests, and public spaces when rules are weak.

Government can improve outcomes by defining and enforcing property rights, setting usage limits, or managing shared resources collectively. For example, fishing quotas can prevent collapse of fish populations. Water rights can reduce conflict over scarce rivers. Patent law gives inventors temporary rights to profit from ideas, which can encourage innovation.

Economists sometimes note that if property rights are clear and negotiation is easy, people may bargain to reduce externalities on their own. But in real life, bargaining can be difficult when many people are affected, information is incomplete, or power is unequal. That is why law and regulation remain important.

The comparison in [Figure 4] highlights the incentive problem. When no one is clearly responsible, overuse becomes rational for individuals even though it is damaging for the group.

Government also intervenes to protect consumers and ensure basic standards. Firms may know more than buyers about product quality or safety. A drug company understands its medicine better than most patients. A bank understands its risks better than most depositors. This unequal information can lead to fraud, unsafe products, or financial instability. Regulation can require truthful labeling, safety testing, disclosure of risks, and minimum standards.

Essential services raise another issue. Some goods and services are so important that societies do not want access determined only by ability to pay. These may include clean water, electricity, emergency care, basic education, sanitation, and in many places internet access. Government may provide these directly, subsidize private providers, or regulate prices to keep them affordable.

| Area | Why Markets May Fall Short | Common Government Response |

|---|---|---|

| Electricity and water | Natural monopoly, high fixed costs | Rate regulation or public ownership |

| Healthcare | Information gaps, externalities, affordability concerns | Licensing, insurance rules, subsidies, public programs |

| Education | Positive externalities, equity concerns | Public funding and attendance laws |

| Financial markets | Risk, opacity, systemic instability | Disclosure rules, capital requirements, oversight |

Table 1. Examples of why governments regulate or support essential goods and services.

At the same time, regulation has costs. Rules can be expensive to follow, and excessive bureaucracy can discourage innovation or make it harder for new firms to enter a market. A useful policy is specific enough to fix a clear problem but flexible enough to avoid unnecessary burden.

Case study: Why utility prices are often regulated

A city usually cannot support five separate water pipe systems just so companies can compete street by street. The costs are too high, and one network often serves the area most efficiently.

Step 1: Identify the market problem

Water delivery has very high fixed costs for pipes, pumps, and treatment plants, so one provider may dominate the market.

Step 2: Consider the risk

If that provider is unregulated, it may charge high prices because households cannot easily switch to another network.

Step 3: Apply a government response

A public utility commission may review rates, service quality, and investment plans to balance affordability with the company's need to cover costs.

This approach tries to keep the efficiency of one network while limiting the harm of monopoly power.

Access matters because markets do not automatically treat all goods the same. For luxury goods, limited access may be accepted. For drinking water or vaccines, societies often decide that leaving outcomes entirely to the market would be dangerous or unfair.

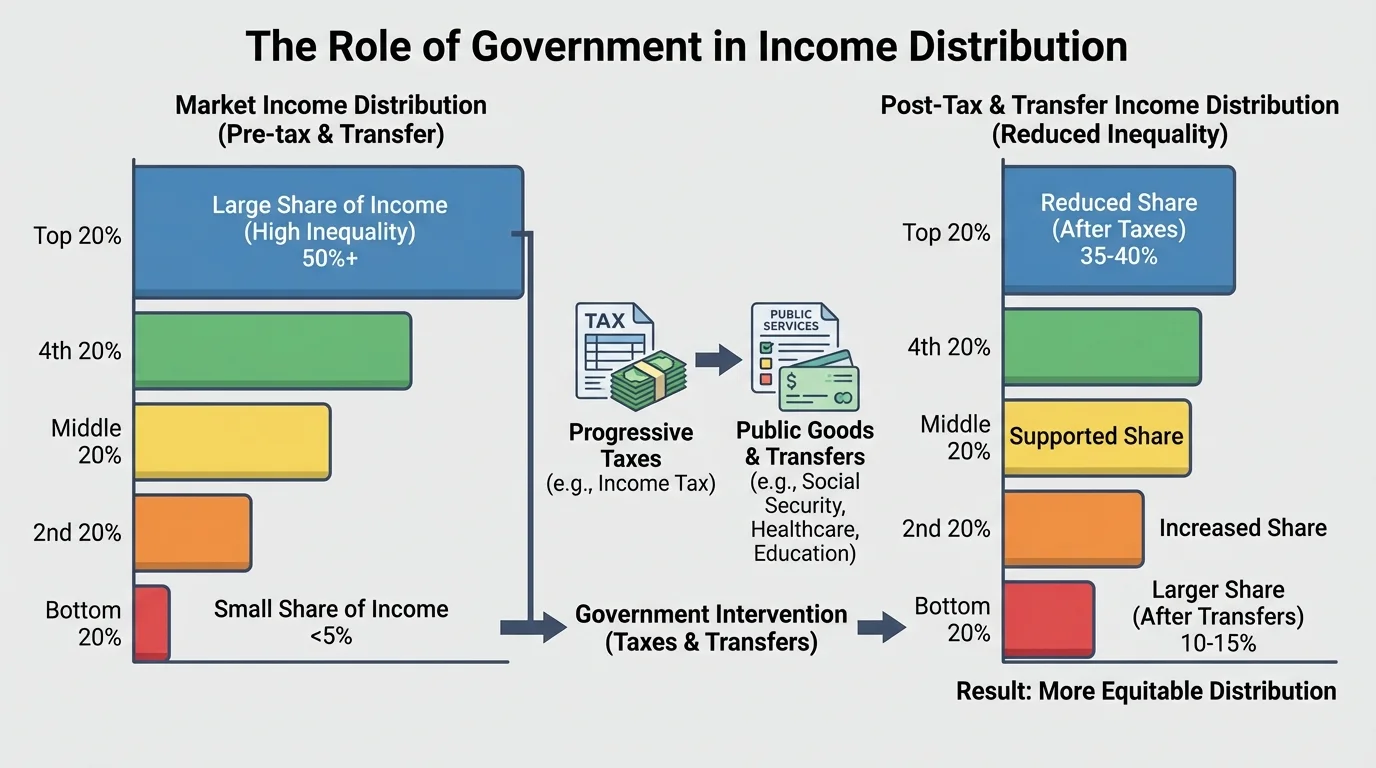

Even if a market is efficient, it may still produce a very unequal distribution of income and wealth. That is why economists distinguish between efficiency and equity. A labor market may reward workers with scarce skills more than others. An inheritance system may pass wealth across generations. A recession may hit some groups much harder than others.

Governments address income distribution through progressive taxes, transfer payments, public services, and labor market rules. A transfer payment is money the government gives to individuals without receiving a current good or service in exchange, such as unemployment benefits or some forms of income support. Public education, food assistance, housing support, and healthcare programs also affect the standard of living.

Supporters of redistribution argue that extreme inequality can reduce opportunity, weaken social mobility, and create hardship even in a growing economy. Critics worry that high taxes or poorly designed benefits can weaken incentives to work, save, invest, or start businesses. Both sides are asking an important question: how can society reduce hardship and expand opportunity without creating large efficiency losses?

Minimum wage laws offer one example of this debate. A higher minimum wage may raise incomes for some workers, but if set too high relative to productivity in a local market, it may reduce hiring in some businesses. The effects depend on the size of the increase, the structure of the labor market, and the broader economy.

The pattern shown in [Figure 5] reminds us that government does not just change total output. It also changes who receives the gains from economic activity. That is a central political and moral issue in every mixed economy.

Good economics does not assume markets are always right or governments are always wise. It compares realistic alternatives. When deciding whether government should intervene, economists often ask: What market failure exists? How large is it? Which policy tool fits best? What are the side effects? Who gains and who loses?

For example, an antitrust case may protect competition and lower prices, but it may also reduce some economies of scale. Environmental rules may reduce pollution and improve health, but they may raise production costs. Public provision of goods may solve the free-rider problem, but taxes needed to fund them can affect incentives elsewhere in the economy. Every policy involves trade-offs.

Competitive markets often work well when many buyers and sellers exist, information is good, property rights are secure, and all major costs and benefits are included in market prices. Government intervention becomes more likely when one or more of those conditions breaks down.

A strong evaluation also considers time. Some policies look costly in the short run but prevent larger long-run damage. Pollution controls can be expensive for firms today, yet much cheaper than widespread illness or environmental collapse tomorrow. Likewise, investment in education or vaccination may require public spending now while producing larger social benefits years later.

"The market is a good servant but a bad master."

— Adapted economic principle

The role of government in addressing market failures is therefore not simply to control the economy. It is to create the legal structure, incentives, protections, and public investments that help markets serve society more effectively. In a mixed economy, producers, consumers, and government are all shaping outcomes together.