A single car crash, house fire, or hospital stay can cost more than many families save in years. That is why insurance matters: it helps transfer part of financial risk from an individual to a company in exchange for a regular payment. For teenagers approaching adulthood, insurance may seem like something only adults deal with. But once you begin driving, working, renting an apartment, or owning valuable property, insurance becomes part of real financial decision-making.

Life includes risks that are hard to predict. A person may stay healthy for years and then suddenly need surgery. A careful driver may still be hit by someone else. A family may maintain a home responsibly and still face damage from a storm. These events are uncertain, but their financial impact can be enormous. Insurance is one of the main risk management strategies people use to reduce the danger of a catastrophic loss.

Without insurance, a person must pay the full cost of a major loss alone. With insurance, that cost is shared. This does not remove the loss itself, but it can prevent one event from causing long-term debt, bankruptcy, or the loss of financial stability.

Insurance is a financial agreement in which a person or business pays for protection against certain losses. A premium is the amount paid for coverage. A claim is a request for payment after a covered loss. A deductible is the amount the policyholder pays before the insurer begins paying.

Insurance is especially important because many financial risks are low-frequency but high-cost. That means they do not happen often, but when they do happen, the bill can be huge. For example, a healthy person may rarely need emergency care, but one emergency room visit and follow-up treatment could cost thousands of dollars.

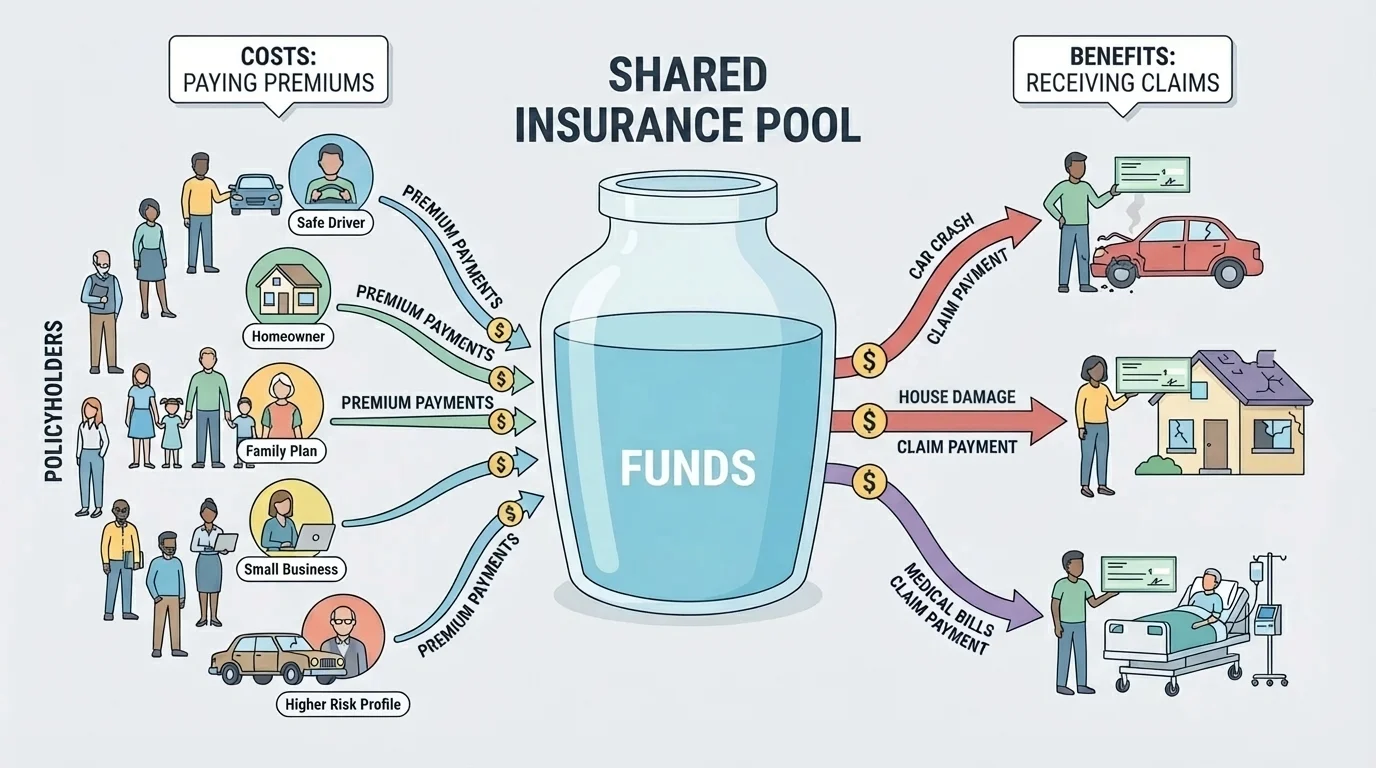

Insurance works by spreading risk across a large group, as [Figure 1] illustrates. Many people pay premiums into a shared system, and the insurance company uses that money to pay the claims of the smaller number of people who experience covered losses. This process is called risk pooling.

Insurance companies do not choose prices randomly. They study data to estimate how likely a loss is and how expensive that loss might be. If a company expects higher costs, it usually charges higher premiums. If it expects lower costs, it can charge less.

Suppose 10,000 drivers each pay $1,200 per year for auto insurance. The company collects $12,000,000 in premiums. If only a portion of those drivers file claims, the insurer can pay those losses from the pool. The basic financial idea is that many people pay a smaller predictable amount to avoid a much larger unpredictable amount.

Insurance policies have limits and conditions. A policy may cover some events but not others. For example, standard homeowners insurance often covers fire and wind damage, but flood damage may require separate insurance. Reading the policy carefully matters because the benefit of insurance depends on what is actually covered.

Some lenders and governments require insurance. For example, drivers in most states must carry auto liability insurance, and mortgage lenders usually require homeowners insurance on the property they finance.

Different types of insurance protect against different risks. Health insurance helps with medical costs. Auto insurance can cover damage, injuries, and liability. Renters or homeowners insurance protects property and may include liability protection. Disability insurance helps replace income if someone cannot work because of illness or injury. Identity theft protection services may help with fraud recovery, though people should compare those services carefully before paying for them.

The first major benefit is financial protection. Insurance can prevent a single event from destroying a person's finances. Paying a premium each month may feel expensive, but it is often much smaller than paying the full cost of a major loss.

The second benefit is predictability. Premiums are usually known in advance, so insurance turns an uncertain large expense into a smaller, more predictable expense. This makes budgeting easier. A family may plan for a $150 monthly premium much more easily than for a surprise $15,000 repair bill.

The third benefit is protection from liability. If a person causes injury or damage to someone else, liability coverage can help pay legal or medical costs. This matters because a lawsuit or a serious injury claim can be financially devastating.

The fourth benefit is peace of mind. Although peace of mind is not a number on a spreadsheet, it is still real. People may sleep better knowing that a major illness, accident, or disaster is less likely to ruin their financial future.

Insurance is not designed to make people richer. Its purpose is to reduce the financial shock of loss. In most cases, the best insurance decision is not the policy that pays the most in every situation, but the policy that gives strong protection against losses large enough to seriously harm your finances.

Insurance also supports long-term goals. Someone saving for college, a car, or a future apartment can lose progress quickly if a major bill appears. By limiting large losses, insurance helps protect other financial plans.

Insurance is not free protection. The most obvious cost is the premium, but that is only one part of the total cost. People also need to consider deductibles, copays, coinsurance, uncovered losses, and the possibility that they may pay premiums for years without filing a claim.

A premium is the regular amount paid to keep a policy active. It may be monthly, quarterly, or yearly. A higher premium often means lower out-of-pocket costs when a claim happens, while a lower premium often means higher costs later.

A deductible is what the policyholder pays before the insurer starts paying on a covered claim. If a driver has a $1,000 deductible and repair costs are $4,500, the driver pays $1,000 and the insurer pays $3,500, assuming the claim is covered.

Another cost is opportunity cost. Money spent on premiums cannot be used for other goals, such as savings, investing, or daily expenses. This does not mean insurance is a bad purchase. It means every insurance decision involves tradeoffs.

There are also coverage limits and exclusions. A policy might refuse to cover certain events, certain types of damage, or amounts above a limit. If a home insurance policy covers up to $250,000 in structural damage but rebuilding costs $320,000, the owner may still face a large uncovered loss.

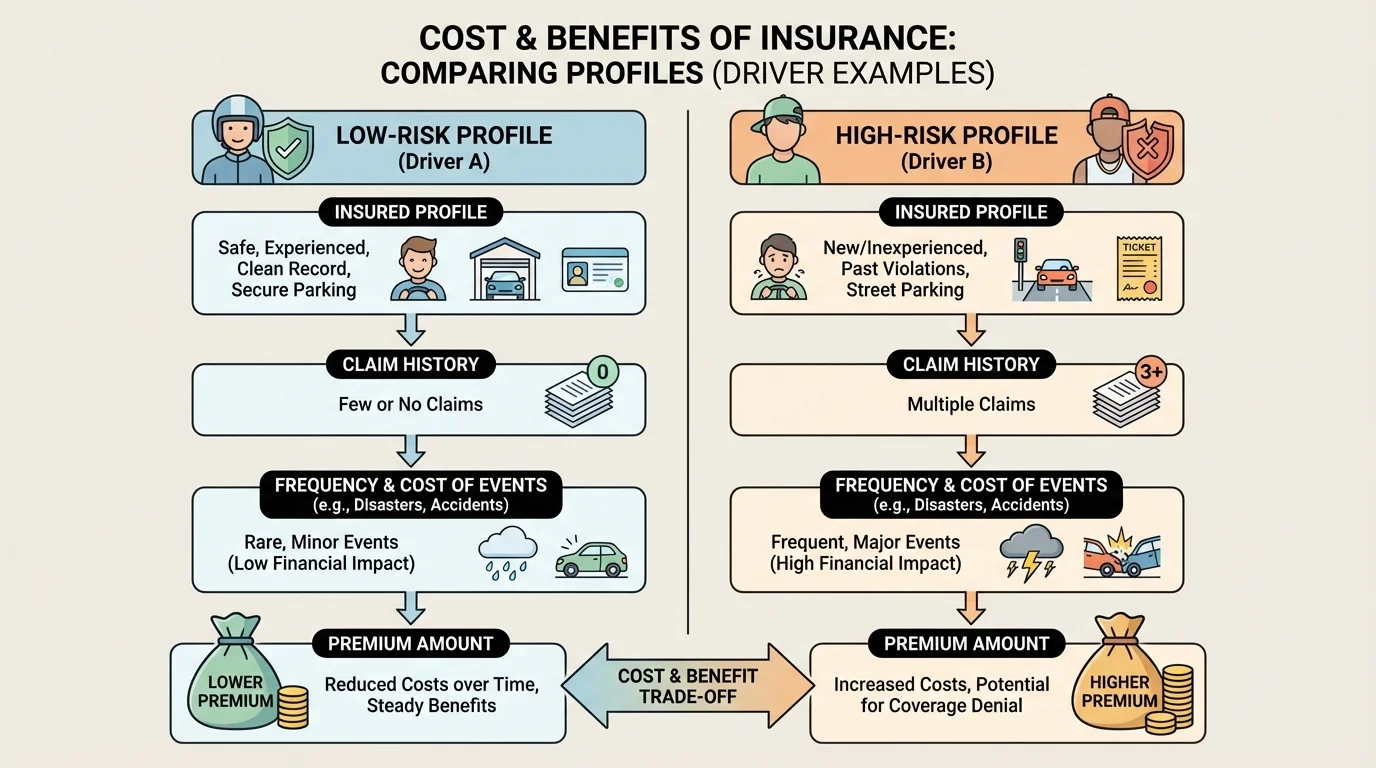

Insurance companies estimate both the probability of loss and the likely size of loss, as [Figure 2] shows through different insured profiles. The cost of insurance is strongly affected by who is being insured, what is being insured, where the person lives, and what claims history already exists.

An insured profile includes characteristics that help insurers estimate risk. In auto insurance, this may include age, driving record, type of car, location, and mileage. In health insurance, age and plan type matter. In homeowners insurance, the age of the home, construction materials, and local hazards matter.

The claim history of the person or property also matters. If someone has filed many claims in the past, insurers may conclude that future claims are more likely. This can raise premiums or even make coverage harder to get.

Claim frequency refers to how often claims occur. If claims happen often, the insurer expects more total payouts. Claim severity refers to how large the claims tend to be. Even if claims are rare, very expensive claims can still lead to high premiums.

Consider two drivers. Driver A has no accidents, drives a safe sedan, and lives in an area with low crash rates. Driver B has two recent accidents, drives a sports car, and lives in a crowded city. Even if they want the same level of coverage, Driver B will usually pay more because the insurer expects a higher chance of future claims and possibly larger losses.

The value of the item being insured matters too. A newer car costs more to repair or replace than an older one. A home with expensive custom features costs more to rebuild. A smartphone insurance plan may cost more for a high-end device than for a basic model.

Fraud also affects costs. When people file false or exaggerated claims, insurers lose money and may raise premiums for everyone in that risk group. This is one reason insurance companies investigate suspicious claims.

| Factor | How it affects insurance cost | Example |

|---|---|---|

| Insured profile | Changes estimated risk level | Teen drivers often pay more than experienced adult drivers |

| Number of claims | More past claims may increase premiums | Three water-damage claims can raise home insurance cost |

| Size of claims | Larger losses raise expected insurer payouts | A severe collision costs more than a minor dent |

| Claim frequency | Frequent claims mean more regular payouts | Repeated small health claims add up over time |

| Natural disaster exposure | Higher disaster risk usually raises premiums | Coastal hurricane zones often cost more to insure |

Table 1. Major factors that influence the price of insurance policies.

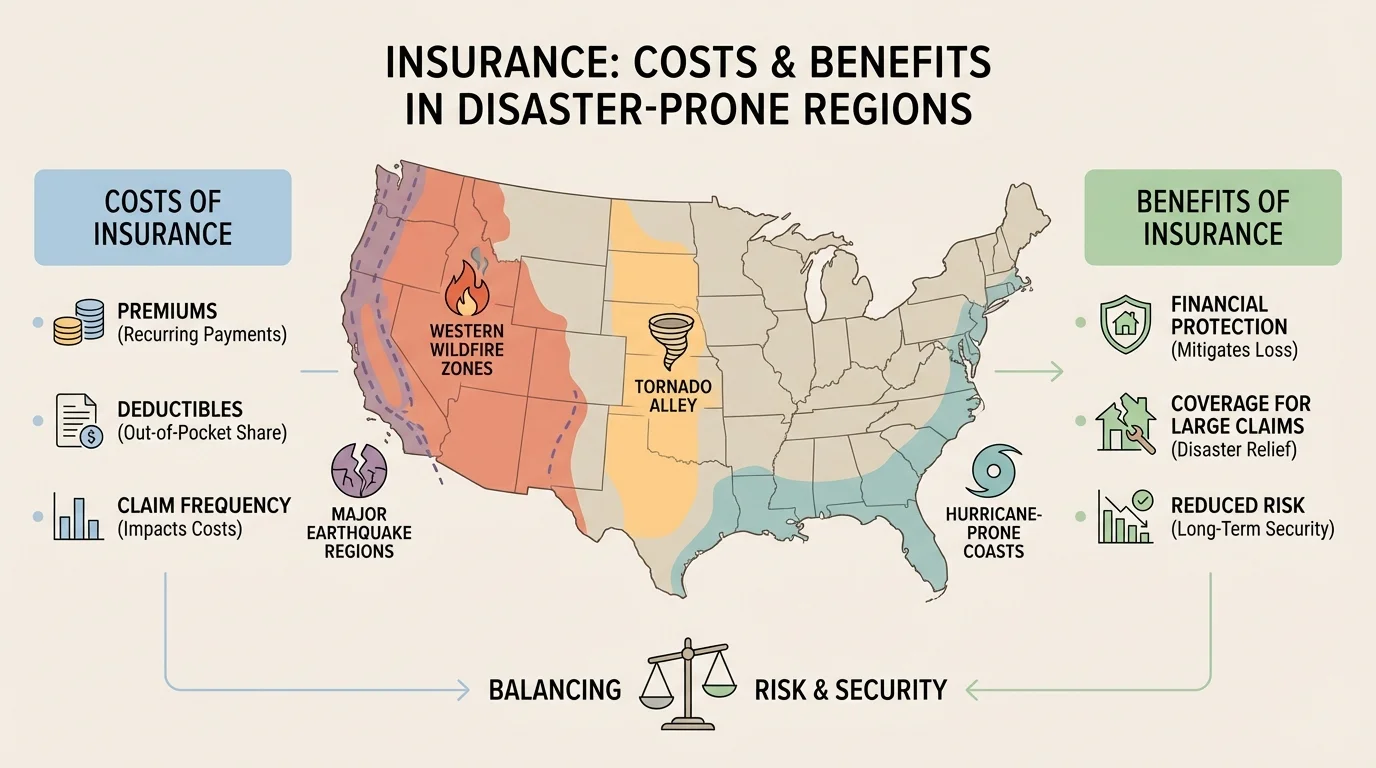

Insurance prices can rise sharply in places exposed to major disasters, as [Figure 3] makes clear by comparing different regional hazards. A house on a hurricane-prone coast, in a wildfire zone, or near an earthquake fault faces a different level of risk than a house in a milder area.

Natural disasters affect both how often losses happen and how severe they are. A small storm might damage one roof. A major hurricane might damage thousands of homes at once. That means insurers are not only paying many claims, but often very large claims at the same time.

For example, flood insurance is especially important in areas near rivers, coasts, and low-lying land. Yet many people discover too late that standard homeowners insurance may not cover flood damage. In wildfire regions, insurers may charge more or reduce coverage options because rebuilding costs and total losses can be high.

Climate patterns, population growth, and rising repair costs can also affect premiums. If a disaster-prone area becomes more populated, there are simply more homes, cars, and businesses at risk. If construction materials and labor become more expensive, each claim costs more to settle.

Case study: coastal home risk

A family compares two similar houses. House X is inland, while House Y is on the coast in an area with frequent hurricane damage. Even if both houses are worth about $300,000, House Y will likely have higher insurance premiums because the probability of storm loss is higher and storm losses can be severe.

This is why location matters so much in insurance. As we saw earlier in [Figure 2], insurers build prices from risk data. Regional natural-disaster data is one of the strongest examples of that principle.

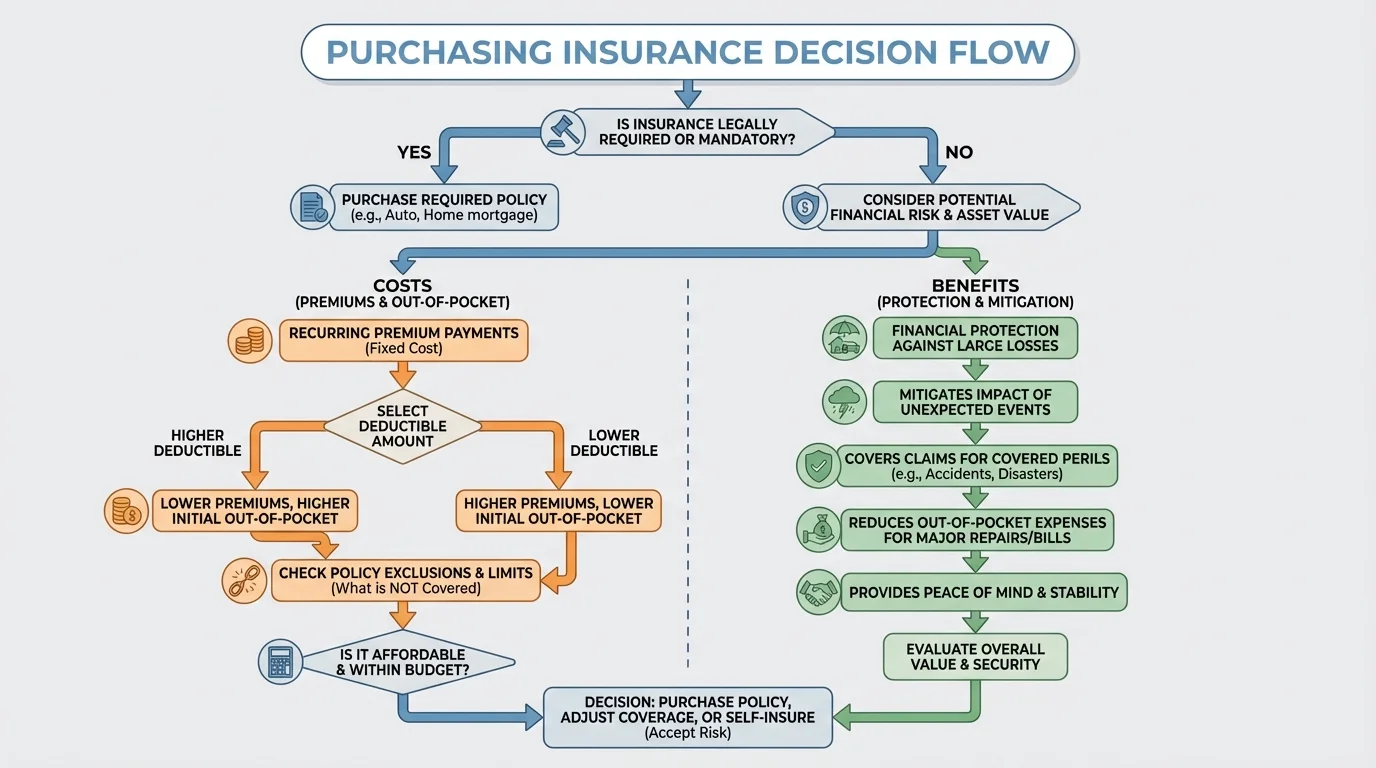

When comparing insurance choices, students should avoid focusing only on the monthly premium. A better method, outlined in [Figure 4], is to compare coverage, deductibles, exclusions, limits, and your ability to pay out of pocket if something goes wrong.

Start by asking what financial risk you are trying to protect against. If the possible loss is small and you could comfortably pay it yourself, insurance may be less necessary. If the possible loss is large enough to create debt or destroy savings, insurance is often more valuable.

Next, compare the total cost of each option. A policy with a low premium but a very high deductible may cost less each month but much more during a claim. A policy with a higher premium may be worth it if it protects you from a loss you could not handle on your own.

Also ask whether the insurance is required. Auto liability insurance is usually legally required for drivers. Health insurance may not always be required by law, depending on the place and situation, but it can still be financially important because medical costs can be very high.

Finally, check the company's reliability. A low premium means little if the company has a poor reputation for handling claims. Consumers often compare ratings, reviews, customer service, and claim response times.

Insurance decisions become clearer when you compare actual numbers. These examples show that the cheapest premium is not always the best financial choice.

Worked example 1: choosing between two auto policies

Policy A has a yearly premium of $1,800 and a deductible of $500. Policy B has a yearly premium of $1,200 and a deductible of $1,500. A covered accident causes $4,000 in repair costs.

Step 1: Find the total yearly cost if the accident occurs under Policy A.

The driver pays the premium plus the deductible: \(1,800 + 500 = 2,300\)

Step 2: Find the total yearly cost if the accident occurs under Policy B.

The driver pays the premium plus the deductible: \(1,200 + 1,500 = 2,700\)

Step 3: Compare the results.

Policy A costs more upfront, but in a claim year it leads to the lower total cost.

The better choice depends on whether the driver is more concerned with monthly affordability or protection during a bad year.

This example shows why a lower premium does not always mean lower total cost. The more risk you keep for yourself through a high deductible, the less you pay now but the more you may pay later.

Worked example 2: expected annual disaster loss

A homeowner estimates a 2% chance of a flood in one year. If a flood happens, the average uninsured loss would be $40,000.

Step 1: Convert the percentage to a decimal.

\(2\% = 0.02\)

Step 2: Estimate the expected annual loss.

\[0.02 \times 40,000 = 800\]

Step 3: Interpret the result.

The expected annual loss is $800. If flood insurance costs less than or close to that amount, and especially if the family cannot absorb a $40,000 hit, buying insurance may be reasonable.

Expected loss does not predict exactly what will happen in one year. Instead, it helps compare a known insurance cost to an uncertain financial risk.

Worked example 3: how claims history changes cost

A renter's insurance premium is $240 per year. After two claims, the insurer raises the premium by 25%.

Step 1: Find the increase.

\[240 \times 0.25 = 60\]

Step 2: Add the increase to the original premium.

\[240 + 60 = 300\]

Step 3: State the new premium.

The new yearly premium is $300.

This example connects directly to claim frequency and claim history. More claims can make future insurance more expensive, even if each claim was relatively small.

Worked example 4: comparing whether to insure a phone

A student can buy phone insurance for $14 per month with a $99 deductible. Replacing the phone without insurance would cost $799. Assume there is a 10% chance the phone will be destroyed during the year.

Step 1: Find the yearly premium cost.

\[14 \times 12 = 168\]

Step 2: Estimate the expected uninsured loss.

\[0.10 \times 799 = 79.9\]

Step 3: Interpret the comparison.

The expected uninsured loss is about $79.90, which is less than the $168 yearly premium. Purely from an expected-value viewpoint, the insurance may not be the better deal. However, if the student could not afford a sudden $799 replacement, the insurance might still be worth buying.

That last point is crucial: insurance decisions are not based only on averages. They also depend on whether you could survive the worst-case cost.

People can lower insurance costs by improving the factors they control. A driver may keep a clean driving record. A homeowner may install smoke detectors, security systems, or storm shutters. A renter may choose only the amount of coverage actually needed. In some cases, bundling policies with one insurer can reduce premiums.

It is also wise to maintain an emergency fund. Insurance and savings work together. Insurance helps with large unexpected losses, while savings help cover deductibles, smaller losses, and everyday surprises.

Consumers should also avoid buying too little insurance. Underinsurance may seem cheaper at first, but it can leave a person dangerously exposed. As shown earlier in [Figure 4], a strong decision includes checking whether the coverage limit is high enough to protect against realistic losses.

At the same time, not every risk needs insurance. A useful rule is to insure against losses that would be hard or impossible to handle from savings alone. Small, manageable losses can sometimes be covered by an emergency fund instead.

"Insurance is most valuable when the loss would be financially overwhelming without it."

Making a good insurance decision means balancing cost, protection, and probability. The best choice depends on the size of the possible loss, your personal finances, legal requirements, your location, and the details of the policy. Insurance is neither automatically a bargain nor automatically a waste. It is a tool, and like any financial tool, it works best when used carefully and with full understanding.