Two people can earn the same amount of money and still have very different financial lives. One gets approved quickly for an apartment, qualifies for a lower car payment, and pays less in interest. The other gets denied, needs a larger deposit, or ends up paying hundreds or even thousands more over time. One major reason is credit.

If you understand credit early, you give yourself more options later. That matters because financial opportunity is really about choices: where you can live, what you can afford, how expensive borrowing becomes, and how much stress money causes in your life. Credit scores do not measure your worth as a person, but they do affect how many doors open when you need to borrow money or sign up for certain services.

You may not have a credit score yet, but adulthood arrives fast. A first car, a student loan, an apartment application, a mobile phone plan, or even being added as an authorized user on a family credit card can connect you to the credit system. Learning the rules before you use credit is much smarter than learning after a mistake.

Think of credit like a reputation for borrowing. If you borrow and repay responsibly, that reputation becomes stronger. If you miss payments or take on more debt than you can handle, your reputation weakens. Financial opportunity often depends on that reputation.

Credit is the ability to borrow money now and pay it back later. A credit score is a number that helps lenders judge how risky it may be to lend to you. A credit report is the record of your borrowing and repayment history. A lender is a business, bank, or organization that gives loans or credit.

That is why credit is not just about debt. It is also about trust. When a company lets you pay later, it wants evidence that you are likely to pay as promised.

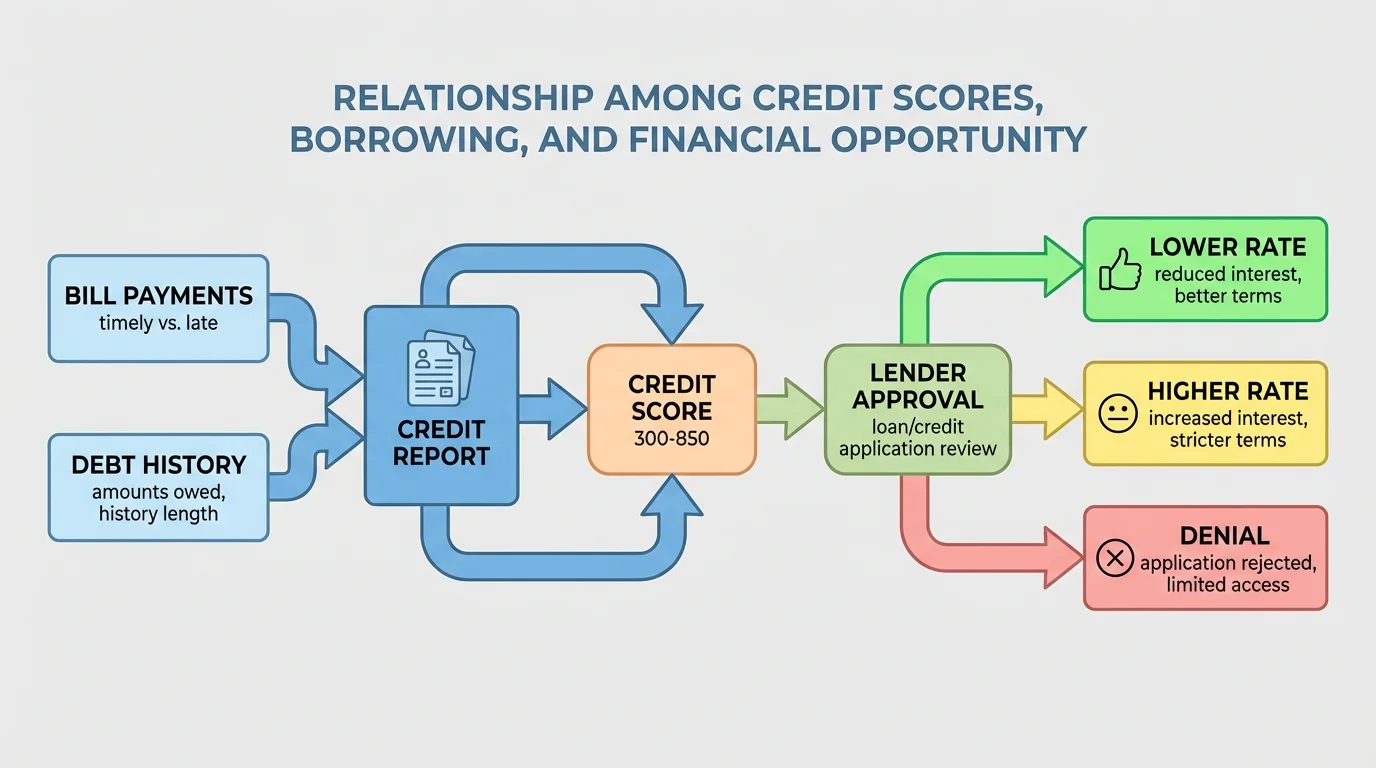

A credit score is a quick summary of your borrowing behavior, and lenders use it to make decisions, as shown in [Figure 1]. Instead of reading every detail of your financial past one by one, a lender often starts with that score to estimate risk.

Your score usually comes from information in your credit report. That report may include whether you paid bills on time, how much debt you owe, how long your accounts have been open, and whether you recently applied for lots of new credit. Higher scores generally suggest lower risk. Lower scores suggest greater risk.

That does not mean a score tells the whole story. It does not measure kindness, intelligence, or work ethic. It is a tool used by businesses to predict whether a borrower will repay on time.

Because credit scores are about risk, they influence both approval and price. You might still qualify for a loan with a lower score, but the loan may cost more. A lender may charge a higher interest rate because it believes there is a greater chance of late payment or default.

Why lenders care about scores

Lenders make money when borrowers repay with interest. They lose money when borrowers do not repay. A credit score helps them sort applicants more quickly. The higher the score, the more confidence a lender usually has that payments will arrive on time. That confidence can lead to better loan terms.

You can think of borrowing like renting trust. When a lender gives you money today, it is trusting your future behavior. The stronger your history, the less worried the lender feels.

Borrowing itself is not automatically good or bad. What matters is how you handle it. If you borrow a manageable amount and pay it back on time every month, you can build a stronger credit history. If you miss payments, max out accounts, or borrow more than you can repay, your credit can be damaged.

Common types of borrowing include credit cards, auto loans, student loans, and personal loans. A credit card is a revolving account, which means you can borrow, repay, and borrow again up to a limit. A loan is usually installment debt, meaning you borrow once and repay in set monthly amounts.

Paying on time is one of the biggest habits in credit building. Even one late payment can hurt, especially if it is seriously overdue. A pattern of on-time payments helps show that you are dependable.

Another important issue is balance size. Using too much of your available credit can make you look financially stretched. For example, if a card has a $1,000 limit and you owe $900, you are using most of your available credit. If you owe $100 instead, you are using much less. Lower usage usually looks safer to lenders.

Borrowing can create opportunity when it helps you reach useful goals without becoming overwhelming. A student loan may help pay for education. A car loan may help someone get to work. But borrowing becomes harmful when the monthly payments crowd out essentials like food, housing, savings, and emergency expenses.

Case study: Same credit card, different choices

Step 1: Kai gets a starter credit card with a $500 limit and uses $50 for gas and school supplies.

Step 2: Kai pays the bill in full by the due date every month.

Step 3: Over time, Kai builds a record of low balances and on-time payments.

Kai is using credit as a tool.

Step 1: Jordan gets a starter credit card with the same $500 limit and quickly charges $480.

Step 2: Jordan misses a payment, gets hit with fees, and keeps carrying a high balance.

Step 3: The account now signals higher risk.

Jordan is using credit in a way that can shrink future options.

The main idea is simple: credit is easiest to manage when your spending is already under control. A credit card cannot fix a money problem. It can make it bigger.

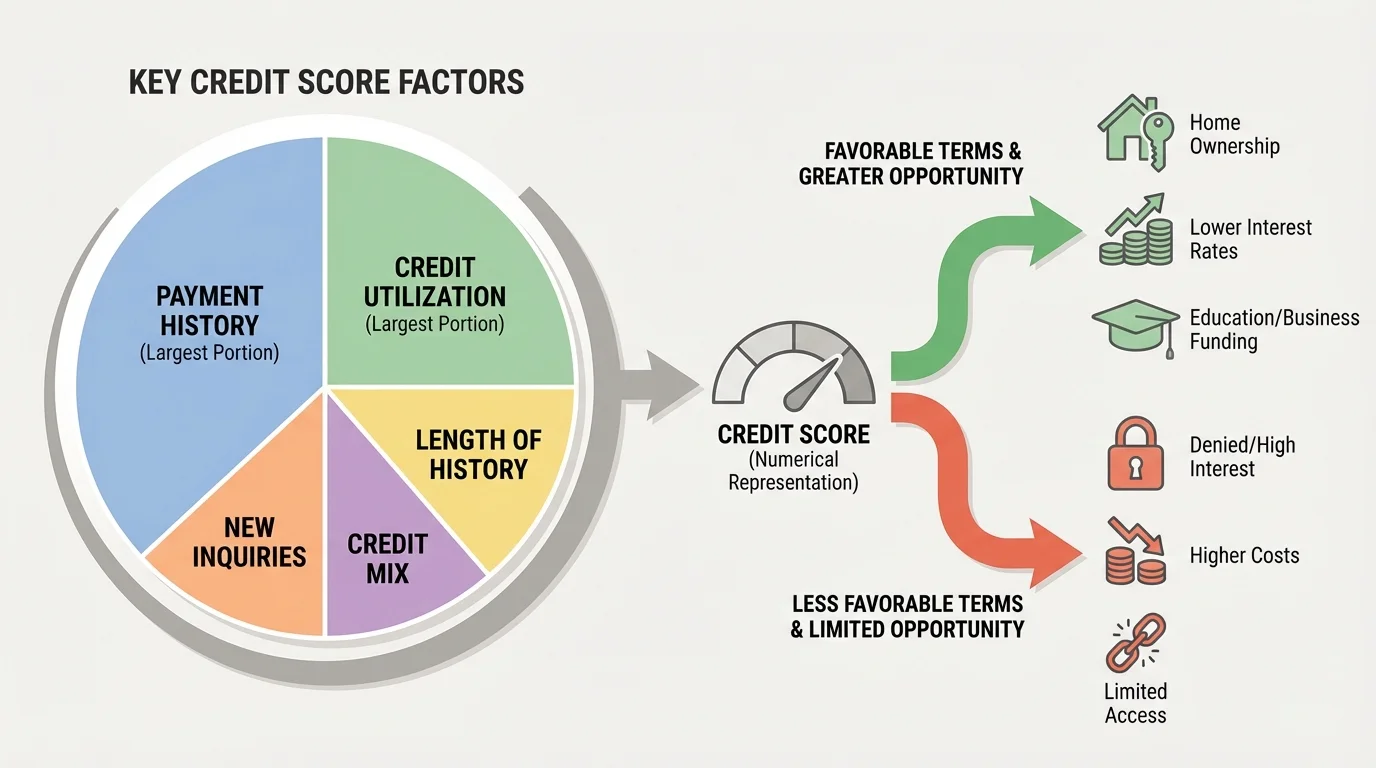

The biggest pieces of your score are the same habits that make someone look reliable with money, and [Figure 2] shows these pieces visually. Different scoring models vary, but the general idea stays similar.

Payment history matters most for many scoring systems. Businesses want to know whether you paid on time. Credit utilization, or how much of your available revolving credit you are using, also matters a lot. Then come factors like the length of your credit history, recent applications for new credit, and the mix of account types you have used.

Credit utilization is especially important for credit cards. It compares your balance to your credit limit. If you owe $300 on a card with a $1,000 limit, your utilization is \(\dfrac{300}{1000} = 0.3\), which is \(30\%\). Lower utilization is usually better than high utilization.

Hard inquiry means a lender checks your credit because you applied for new credit. A few inquiries are normal, but many applications in a short time can signal risk. It can look like someone is urgently trying to borrow money.

Credit history also matters because lenders like to see a pattern over time. A longer, positive record usually provides more confidence than a brand-new account. This is one reason people are often told not to open and close accounts carelessly.

Finally, credit mix means the variety of credit types you have managed. This is not the first thing to worry about, and you should never borrow just to improve variety. But responsibly handling different types of accounts can sometimes help show broader experience.

| Factor | What it means in everyday life | Helpful habit |

|---|---|---|

| Payment history | Whether you pay bills on time | Set reminders and autopay if possible |

| Credit utilization | How much of your card limit you use | Keep balances low |

| Length of history | How long accounts have been open | Keep older accounts in good standing when appropriate |

| Hard inquiries | Recent applications for new credit | Avoid applying for lots of accounts at once |

| Credit mix | Different kinds of credit managed well | Focus on responsible use, not collecting accounts |

Table 1. Main factors that influence a credit score and the practical habits connected to each one.

Notice that most of these factors are about behavior, not income. A person can earn a lot and still damage credit through missed payments and overspending. Another person can earn less and still maintain strong credit through consistency.

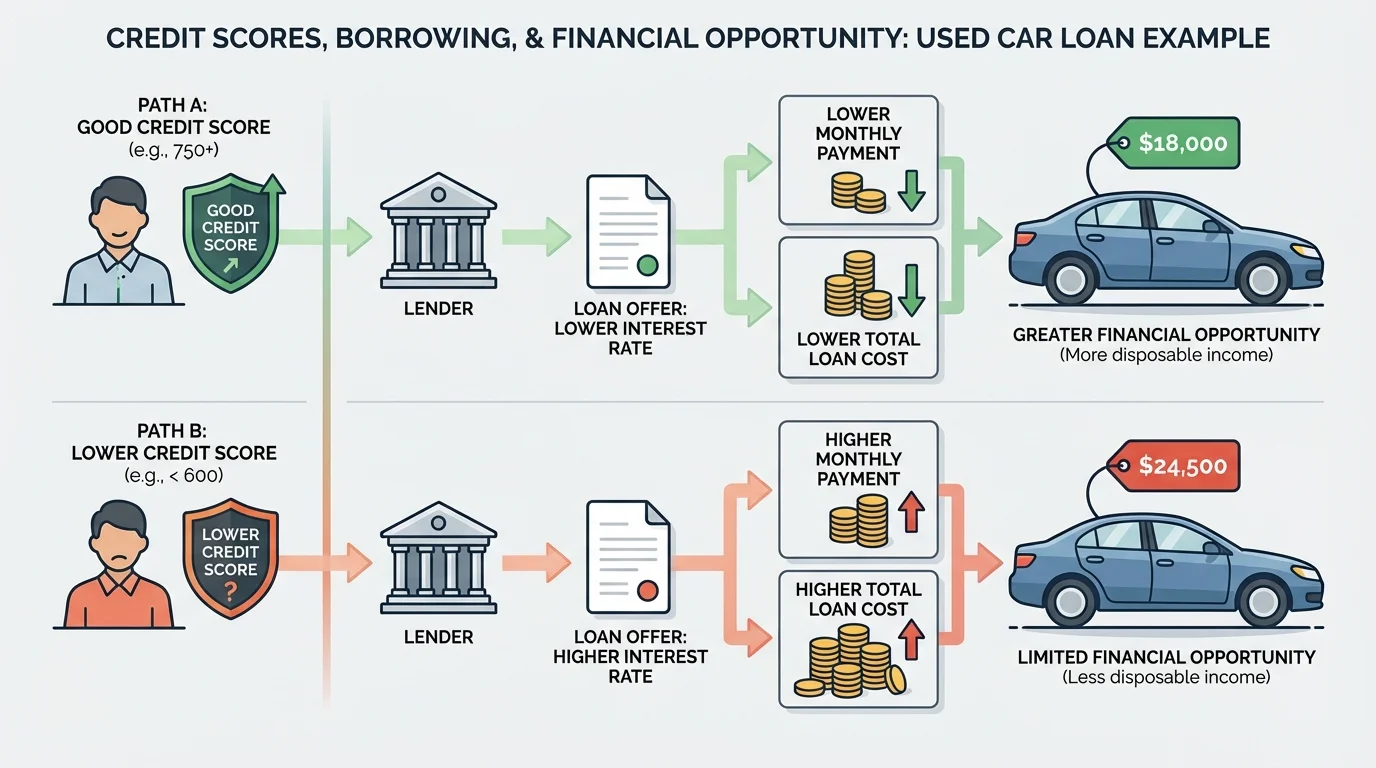

Your score affects more than loan approval. It can influence the interest rate you receive, the deposit required for housing or utilities, and sometimes whether a company is willing to work with you at all. As [Figure 3] shows, credit connects directly to financial opportunity through the cost difference between borrowers.

Interest rate is the extra cost of borrowing money, usually shown as a percentage. A lower rate means you pay less over time. A higher rate means you pay more for the same item.

Real-world example: same car, different credit

Suppose two people each finance a used car costing $12,000.

Step 1: Borrower A has stronger credit and qualifies for a lower rate.

The monthly payment might be around $230.

Step 2: Borrower B has weaker credit and gets a higher rate.

The monthly payment might be around $290.

Step 3: Compare the effect over about four years.

The difference is roughly $60 each month. Over about \(48\) months, that is \(60 \times 48 = 2,880\).

For the same car, weaker credit could cost about $2,880 more.

This is why people say poor credit is expensive. It can turn an ordinary purchase into a much larger total cost. This effect is not just about a number on a screen. It affects your monthly budget, your stress level, and how much money remains for savings or emergencies.

Credit can also affect housing. A landlord may review your credit before approving a lease. A weak record may lead to a denial, a larger security deposit, or a requirement for a co-signer. Utility companies may also charge deposits when they think a customer is riskier.

Insurance companies in some places use credit-based information when setting prices. Some employers also review credit reports for certain jobs, especially roles involving money, security, or sensitive information. Rules vary by location, but the big idea stays the same: your financial habits can shape opportunities beyond borrowing.

Some people think credit only matters when buying a house, but it can affect everyday adult life much earlier through car loans, apartment applications, phone plans, and utility deposits.

Good credit does not guarantee wealth, and poor credit does not guarantee failure. But strong credit often makes progress cheaper and easier. Weak credit often makes progress harder and more expensive.

Consider three short situations. In the first, a young adult wants to move into an apartment near a new job. Strong credit helps them qualify quickly with a standard deposit. In the second, someone with several missed payments applies for the same apartment and is told they need a much larger deposit. In the third, someone has no credit history at all, which can also create problems because there is not enough information to judge risk.

Now think about transportation. If your car breaks down and you need financing fast, a stronger score may give you better choices. If your score is weak, you may still get approved, but with more expensive terms. That can trap you in a cycle where the payment is so high that the rest of your budget suffers.

Even a phone can become part of this story. Some carriers check credit before offering certain financing plans for devices. A stronger record may make approval easier, while a weaker one may require more money up front.

These situations show the relationship clearly: credit scores affect borrowing, and borrowing affects financial opportunity. The cycle can work in your favor or against you. Responsible borrowing can improve your score, and a stronger score can expand your opportunities. Irresponsible borrowing can damage your score, and a weaker score can shrink your opportunities.

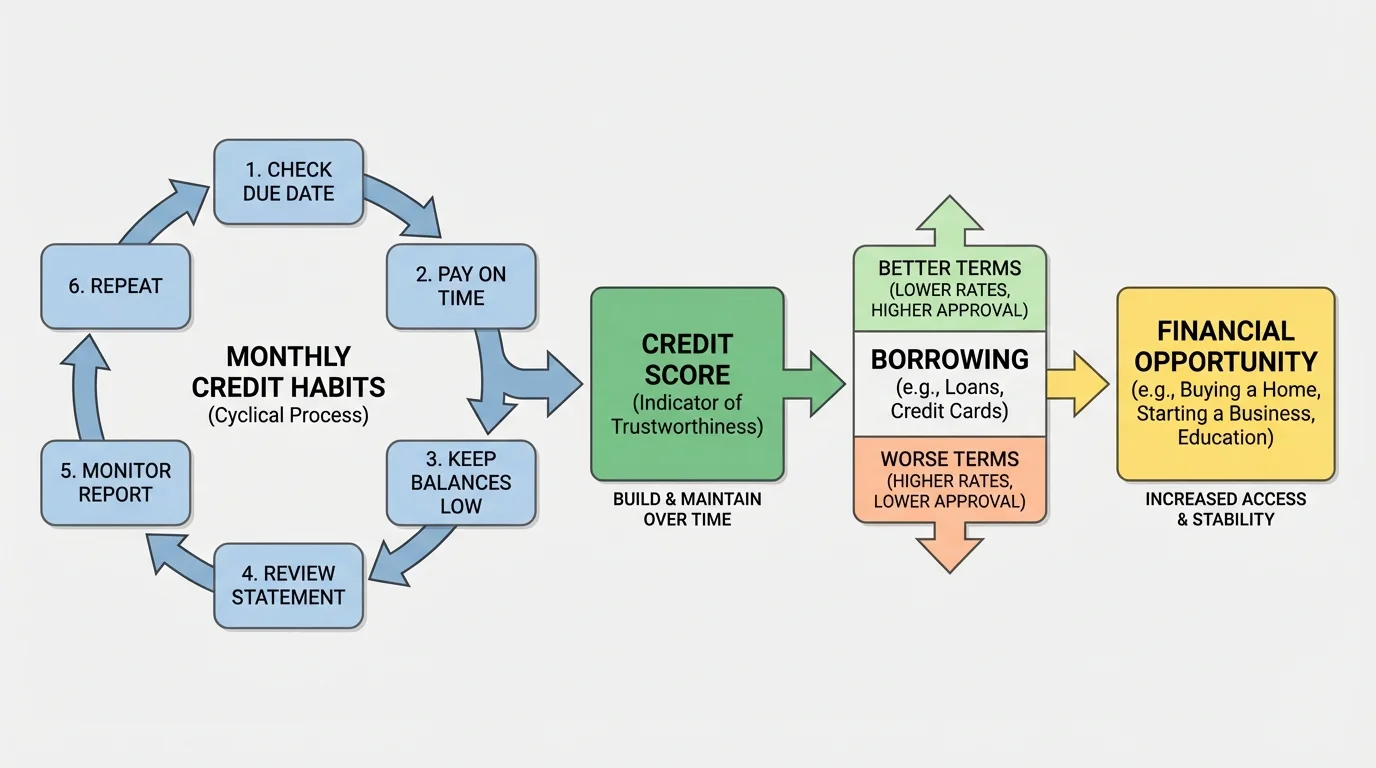

Responsible credit works best as a repeatable routine, and [Figure 4] shows the kind of monthly system that protects your future. You do not need perfect finances. You need consistent habits.

Step 1: Only borrow what you can realistically repay. Before using a card or taking a loan, ask yourself whether the payment fits your budget even if an unexpected expense appears.

Step 2: Pay on time every time. Put due dates in your phone calendar, use alerts, or set up automatic payments if you have enough money in the account.

Step 3: Keep balances low. If possible, avoid using most of your credit limit. Lower utilization helps both your budget and your score.

Step 4: Review statements. Check for errors, forgotten subscriptions, fraud, or signs that you are spending faster than you realized.

Step 5: Monitor your credit. As you get older and begin using credit, review your reports periodically to make sure the information is accurate.

Debt becomes dangerous when it grows faster than your ability to repay it. That is why "Can I make the minimum payment?" is not the best question. A better question is, "Can I pay this off without hurting my future budget?"

Try This: a simple decision check before borrowing

Step 1: Name the purpose.

Is this purchase necessary, useful, or just impulsive?

Step 2: Check the monthly impact.

If the payment is $75, ask what you must give up each month to cover it.

Step 3: Test your backup plan.

If your hours at work drop or another bill appears, can you still pay on time?

Step 4: Choose the safer option.

If the answer is no, wait, save, or buy something cheaper.

Be careful with "buy now, pay later" offers too. They can feel harmless because the payments are split up, but they still create obligations. If you stack too many of them, you can overload your budget the same way you would with other debt.

It also helps to build an emergency fund. Even a small cash cushion can stop you from using credit for every surprise expense. That protects both your score and your peace of mind.

A damaged score is serious, but it is not permanent. Credit can recover when behavior changes. The key is to respond quickly instead of avoiding the problem.

First, bring late accounts current if you can. Second, make every future payment on time. Third, lower balances where possible. Fourth, stop applying for new credit unless it is truly necessary. Fifth, check your credit report for mistakes and dispute errors if you find them.

Recovery usually takes time because lenders want to see a new pattern, not just one good week. The same way poor habits can drag a score down, consistent better habits can gradually lift it.

"Credit is easy to ignore when you do not need it, but it matters most when you suddenly do."

This is one reason financial responsibility is really about protecting your future self. The decisions you make now can affect the options you have later when life changes fast.

Even if you are not using credit yet, you can still prepare. Learn to budget, track spending, and save for short-term goals. Practice paying obligations on time, even small ones like subscriptions or shared costs with family. These habits transfer directly into good credit behavior later.

Talk with a trusted adult about how credit cards, loans, and reports work. If appropriate, some teens may eventually become an authorized user on a parent or guardian's account, which can sometimes help them begin building history. But this only helps when the account is well-managed, so the adult's habits matter too.

You can also protect yourself from identity theft by being careful with personal information online. If someone opens accounts in your name, that can create credit problems before you even start adulthood. Use strong passwords, avoid sharing sensitive information casually, and watch for suspicious messages or fake forms.

Financial opportunity grows when you combine three things: wise borrowing, strong repayment habits, and patience. Credit scores sit in the middle of that relationship. They are shaped by what you do with borrowed money, and in return they shape what financial options become available to you.