A financial decision you make at age 16 can still affect you at 26. That is not because every teen choice is huge, but because money decisions often stack. Saving a little early can give you options later. Borrowing carelessly can limit those options for years. When you understand how savings, loans, and education costs work together, you stop guessing and start making choices that fit your real life.

You are already making financial decisions, even if you do not call them that. Keeping birthday money in cash, using a debit card, buying something online, considering a car, thinking about college, trade school, certification programs, or training after high school—all of these involve tradeoffs. The goal is not to become obsessed with money. The goal is to make choices that protect your future freedom.

Good financial decisions usually answer three questions: How much does it cost now? How much will it cost later? What option gives me the most value for the least long-term stress? These questions matter whether you are choosing where to keep $300, whether to finance a laptop, or how to pay for a nursing program, welding certification, or four-year degree.

Savings is money you set aside for future use. Principal is the amount borrowed before interest and fees. Interest is the extra money paid for borrowing or earned for saving. Postsecondary costs are the expenses connected to education or training after high school, including far more than tuition.

One of the most useful money skills is understanding opportunity cost. That means when you choose one use for your money, you give up another option. Spending $400 on a new phone might mean you cannot use that same $400 for emergency savings, a certification exam, or books for a class. There is nothing wrong with spending money on something you enjoy, but a smart decision includes what you are giving up.

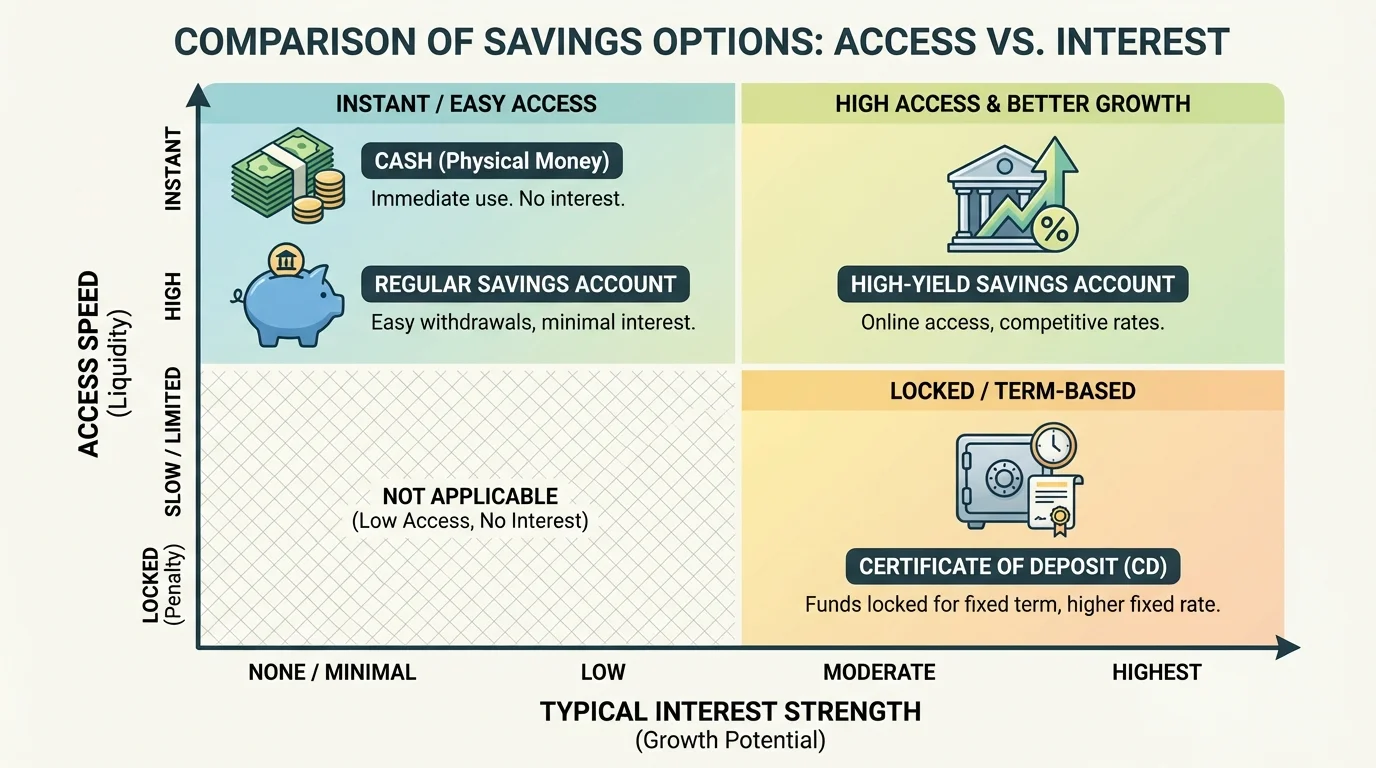

Saving is not just about "being responsible." It is about creating breathing room. If your headphones break, your work hours are cut, or you need to pay for a test fee, savings can keep a problem from becoming a crisis. As [Figure 1] shows, the best place for your money depends on two things: how soon you may need it and how much growth you want from it.

A practical savings plan often has different buckets. One bucket is spending money for regular purchases. Another is an emergency fund for unexpected costs. Another may be a goal fund for something specific like a laptop, car insurance, move-out costs, or education expenses. Keeping all your money in one mental pile makes it easier to spend money meant for a more important purpose.

Another key idea is liquidity, which means how quickly you can access your money without penalty. Cash is very liquid. A checking or savings account is also liquid. A certificate of deposit may pay more, but your money is less accessible for a set time. If your money is for emergencies, access matters more than chasing a slightly higher return.

If you earn interest on savings, your balance can grow even when you are not adding much. For example, if you save $50 each month for 12 months, you contribute $600 total. Without interest, you still have $600. With interest, you may have a little more. At this stage, the biggest win is usually the habit of saving regularly, not trying to find magical returns.

Here is a simple savings check: before you put money somewhere, ask When will I need this? If the answer is "any week now," keep it somewhere safe and easy to access. If the answer is "not for a year or more," you can compare options that may earn more. That tradeoff between access and growth is the same one shown earlier in [Figure 1].

Example: Building a short-term goal fund

You want $900 for a laptop in 9 months.

Step 1: Divide the goal by the number of months.

\[\frac{900}{9} = 100\]

Step 2: Decide where the money should go.

Because you need it within a year, a savings account makes more sense than an option that locks up your money.

Step 3: Turn it into an automatic habit.

Set up an automatic transfer of $100 each month right after any paycheck or allowance arrives.

This works because the goal becomes a system, not a vague wish.

Try This: Pick one savings goal you could realistically work on this month. Name it, choose an amount, and decide where the money will live. Even starting with $10 or $20 matters because it creates a pattern.

Not all savings choices serve the same purpose. A regular savings account is simple and usually safe, but may pay low interest. A high-yield savings account often pays more, especially online, but you should still check rules, transfer speed, and whether the institution is insured. Cash is easy to use but can be lost, stolen, or spent too casually. A certificate of deposit can reward patience, but it is not a great choice for money you may need soon.

When comparing saving options, do not ask only, "Which one earns the most?" Also ask, "Is my money safe? Can I get it when I need it? Will this setup help me avoid impulse spending?" Sometimes a slightly lower return is worth it if the account is easier to manage and better supports your goal.

| Option | Best For | Main Advantage | Main Limitation |

|---|---|---|---|

| Cash | Very small short-term spending | Immediate access | Easy to lose or spend |

| Regular savings account | Emergency fund or short-term goals | Safe and accessible | Lower interest |

| High-yield savings account | Short- to medium-term goals | Higher interest | May take longer to transfer funds |

| Certificate of deposit | Money you will not need soon | Predictable return | Penalty for early withdrawal |

Table 1. Comparison of common places to keep saved money.

A smart saver also protects against fees. If an account has a monthly fee of $5, that is $60 a year. On a small balance, that can cancel out the benefit of earning interest. Always read the fee details before opening an account.

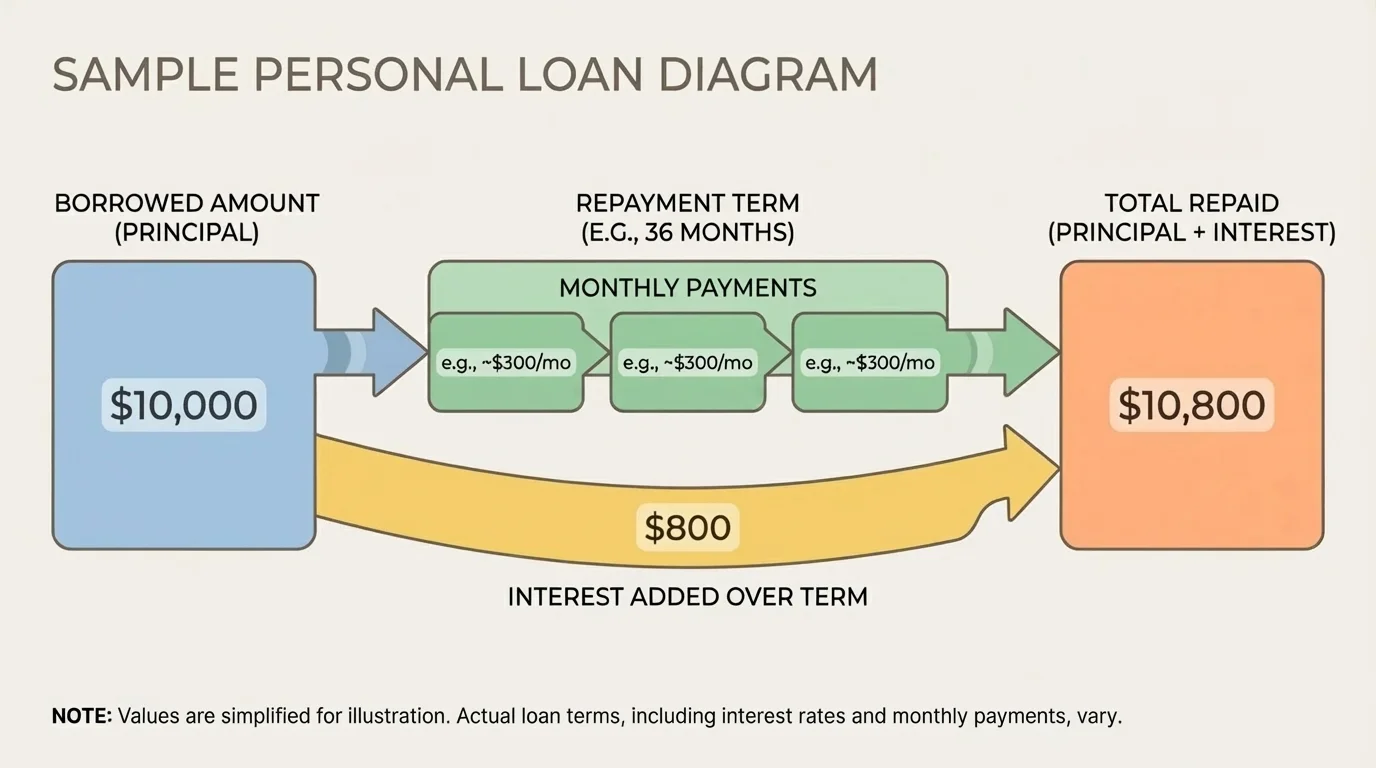

[Figure 2] A loan can solve a short-term problem, but it always creates a future obligation. The amount you borrow is only one part of the story. You also need to look at how interest, fees, and time change the total amount you repay.

The first important term is principal, the amount borrowed. Then comes the interest rate, which affects how much extra you pay. The loan term is how long you have to repay the loan. A longer term often lowers the monthly payment, but it can increase the total paid because interest has more time to add up.

This is why a "low monthly payment" can be misleading. A $120 monthly payment may sound easier than $180. But if the $120 option lasts much longer and includes more fees, you may end up paying much more overall. The monthly payment matters because it affects your budget, but it should never be the only number you compare.

You should also learn the idea of APR, or annual percentage rate. APR gives a broader picture of borrowing cost because it usually includes interest and some fees. It is often more useful than looking at the interest rate alone when comparing two loan offers.

Why longer loans can cost more

Stretching payments over more months can make a loan feel affordable in the short term. But affordability is not just about this month. If interest keeps building over a longer period, the total repayment rises. A lower monthly payment can be a trap if it hides a much larger final cost.

Late fees add another layer. Missing payments can cost you extra money, hurt your credit history, and make future borrowing more expensive. Even a useful loan can become harmful if it does not fit your actual budget.

When you see a loan offer, slow down and compare these five things: amount borrowed, APR, monthly payment, repayment term, and total repayment. If the lender does not make those numbers easy to find, that is a warning sign.

Look for whether the rate is fixed rate or variable rate. A fixed rate stays the same. A variable rate can change, which means your payment or total cost can become less predictable. For many beginners, predictability matters.

Example: Comparing two loan offers

You need to borrow $1,000 for a necessary expense.

Step 1: Compare the monthly payments.

Loan A costs $95 per month for 12 months. Loan B costs $55 per month for 24 months.

Step 2: Find the total repaid for each loan.

For Loan A, the total is \[95 \times 12 = 1{,}140\]

For Loan B, the total is \[55 \times 24 = 1{,}320\]

Step 3: Compare the extra cost beyond the amount borrowed.

Loan A adds \[1{,}140 - 1{,}000 = 140\]

Loan B adds \[1{,}320 - 1{,}000 = 320\]

Loan B feels easier each month, but it costs $180 more overall. If your budget can handle Loan A safely, it is the less expensive choice.

Payday loans, title loans, and "buy now, pay later" offers can be especially risky if you do not read the terms. Fast approval does not mean a good deal. If a lender pressures you, hides fees, or depends on you being desperate, step back.

Try This: The next time you see a financing ad online, ignore the "only $___ per month" line at first. Search for the total repayment and fees. Train yourself to look past the ad's most attractive number.

Later, when you are comparing education financing options, the same idea from [Figure 2] still applies: borrowing is never just about what you receive today; it is about what you owe across time.

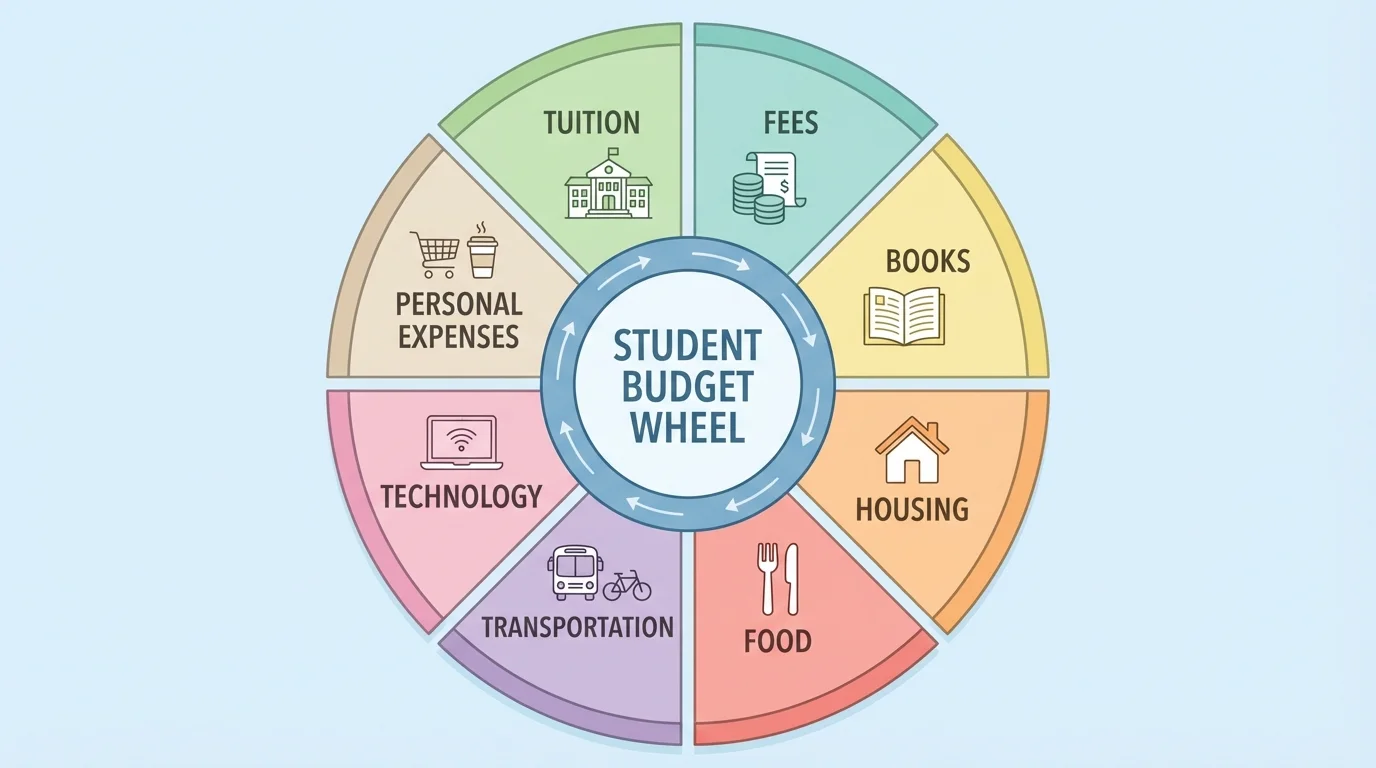

[Figure 3] Many students make one big mistake when planning for education after high school: they focus only on tuition. But tuition is just one category. The full cost of attendance usually includes fees, books, supplies, housing, food, transportation, technology, and personal expenses.

If a program costs $8,000 in tuition, that does not mean your total yearly cost is $8,000. You may also need a laptop, internet service, certification exam fees, gas, transit passes, or work clothes. If you move out, housing can become one of the biggest costs. If you stay home, commuting may become the trade-off instead.

This matters because the "cheapest" school on paper may not be the lowest total cost. A school with lower tuition but high housing costs could end up costing more than a nearby option where you can live at home. A shorter training program may get you into paid work faster, changing the math in a good way.

Another hidden factor is lost income. If one pathway lets you work part-time while studying and another makes work nearly impossible, that affects affordability. Money you cannot earn because of your schedule is part of the real cost too.

| Cost Category | Examples | Often Overlooked? |

|---|---|---|

| Tuition and fees | Classes, registration, lab fees | No |

| Books and supplies | Textbooks, tools, uniforms | Yes |

| Technology | Laptop, software, internet | Yes |

| Living costs | Housing, food, utilities | Yes |

| Transportation | Gas, parking, bus pass, car maintenance | Yes |

| Personal and exam costs | Certification tests, toiletries, medical co-pays | Yes |

Table 2. Common postsecondary cost categories students should include in their planning.

Example: Estimating total monthly education-related cost

A student estimates the monthly cost of attending a local program while living at home.

Step 1: List the monthly costs.

Transportation $120, food away from home $80, books and supplies averaged monthly $90, internet and software $60, personal school expenses $50.

Step 2: Add them.

\[120 + 80 + 90 + 60 + 50 = 400\]

Step 3: Project the cost over a 10-month academic year.

\[400 \times 10 = 4{,}000\]

Even before tuition, this student needs to plan for $4,000 in related yearly costs.

When families and students underestimate these categories, they often borrow more than expected later. That creates stress in the middle of a school year, when changing plans is harder. Building a fuller estimate earlier gives you more control.

The best money for education is usually money you do not have to repay. That includes grants and scholarships. After that, savings and income from work can help. Borrowing should usually come later in the order, not first.

There are many smart pathways, not just one. Community college, transfer programs, apprenticeships, military benefits, employer-supported training, certification programs, and part-time study can all make sense depending on your goals. The "best" choice is not the most impressive-looking option online. It is the one that helps you reach your goal with a reasonable cost and manageable debt.

Before borrowing for education, compare the likely total debt to the earning power of the career path. No one can predict the future perfectly, but you can still ask practical questions: What jobs does this program lead to? What do entry-level workers in that field usually earn? How likely am I to finish this program? A good program that you cannot complete is not a good financial decision.

Many students save thousands by completing general courses at a lower-cost institution and transferring later, but only if the credits will actually transfer. Always verify transfer rules before assuming a cheaper first step will count the way you expect.

You also need to separate wants from required costs. A certain campus, apartment, or lifestyle may sound exciting, but if it forces you into much heavier borrowing, the long-term tradeoff may not be worth it. That does not mean choosing the cheapest option no matter what. It means being honest about value.

The complete cost picture shown earlier in [Figure 3] helps here too. If you can reduce transportation, housing, or technology expenses, you may need much less borrowing even when tuition stays the same.

When you face a savings, loan, or education decision, use a repeatable process instead of going by emotion alone.

Step 1: Define the goal. What are you trying to accomplish? Build emergency savings? Pay for a certification? Choose between schools? If the goal is unclear, the decision usually gets worse.

Step 2: List the full cost. Include upfront costs, monthly costs, fees, and total repayment if borrowing is involved.

Step 3: Check affordability. Can you handle the monthly amount without constantly falling behind on other needs?

Step 4: Compare value. Which option gets you the result you need at the lowest long-term cost?

Step 5: Look for risk. What happens if your income drops, your hours change, or an emergency appears?

Step 6: Pause before committing. One day of thinking can prevent months or years of regret.

"Do not ask only whether you can get something. Ask whether you can comfortably keep paying for it."

This framework works in small situations too. Suppose you want to finance a $600 device. You can ask: Do I need it now? Could I save for it instead? If financed, what is the total cost? Would paying monthly reduce my ability to handle other basics? Sometimes the smartest decision is waiting.

Good financial choices are easier when your habits support them. Read the full terms before agreeing to anything. Keep track of due dates. Save documents and screenshots. Use secure passwords for financial accounts. Do not assume an offer is safe because it looks polished on social media or comes through email.

Watch for red flags such as pressure to act immediately, unclear repayment terms, promises that sound too easy, hidden fees, or messages asking for personal information through suspicious links. Scams often target people who are busy, stressed, or excited.

Another strong habit is asking better questions. Instead of "Can I afford the monthly payment?" ask "What is the total cost?" Instead of "Which school is cheapest?" ask "Which path gives me the best outcome for the total cost?" Better questions usually lead to better decisions.

If you already know how to make a basic budget, use that skill here. A budget is not just for groceries or entertainment. It is one of the best tools for testing whether a loan payment, savings goal, or education plan actually fits your real life.

Try This: Make a simple list with three headings: Save, Borrow, and School/Training Costs. Under each, write one decision you may face in the next two years. Then add the most important question you should ask before choosing.

You do not need to have your entire future figured out to make a smart next move. Open a savings account if you do not have one. Start a small emergency fund. Learn how to read a loan ad. Research one career path and one education pathway connected to it. Look up not just tuition, but total estimated cost.

If you are discussing these decisions with a parent, guardian, or trusted adult, bring actual numbers. Conversations go better when they move beyond "I want this" or "I heard this school is good" and become "Here is the cost, here is what I found, and here is why this option seems stronger." That is how adult financial decision-making works.

The point is not perfection. The point is awareness. Every time you compare total cost, check access to savings, question a loan's real price, or estimate education expenses honestly, you build a skill that protects your independence.