Every time someone buys a snack, saves birthday money, or chooses not to spend at all, that small choice sends a signal through the economy. A family buying less fast food may lead a restaurant to order fewer supplies. A person saving money in a bank may help that bank make a loan to a business. Money choices may feel private, but they connect millions of people across neighborhoods, countries, and the Western Hemisphere.

In an economy, people and businesses depend on each other. A consumer is a person who buys and uses goods or services. A business often acts as a producer, meaning it makes goods or provides services. When consumers spend money, they help businesses earn revenue. When businesses earn revenue, they can pay workers, buy materials, and make more products.

This connection is important in the Western Hemisphere, where countries trade food, clothing, cars, electronics, and many other goods. A fruit company in one country may sell bananas to stores in another. A shoe company may design products in one place and manufacture them in another. The choices made by families, workers, and businesses all shape what gets produced, how much is sold, and where jobs are created.

Budget is a plan for how money will be earned, saved, and spent.

Saving means setting money aside for future use.

Investing means using money in a way that may help it grow over time, but with some risk.

Opportunity cost is the value of the next best choice given up when you choose something else.

Because money is limited, every choice has a trade-off. If a student spends all allowance money on a game, that student cannot also use the same money for school supplies or a future goal. That is why personal financial literacy matters. It helps people make choices that support both their own goals and the larger economy.

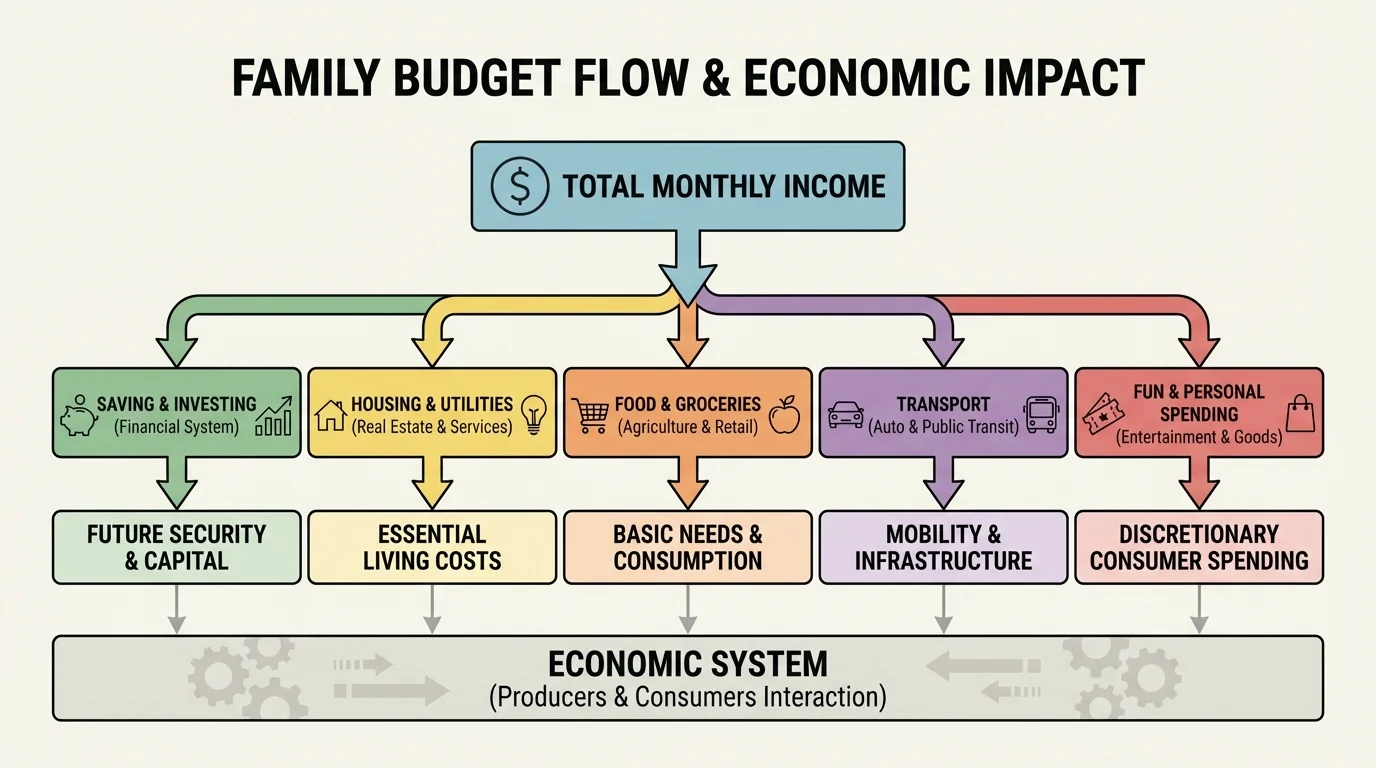

A budget helps people control money instead of wondering where it went. In a basic budget, money coming in is compared with money going out. As [Figure 1] shows, a budget works best when income is organized into categories such as saving, food, transportation, and extra spending.

Suppose a student earns $20 each week from chores and receives $10 for helping a neighbor, for a total weekly income of $30. If the student plans to save $8, spend $12 on snacks and school items, and use $5 for entertainment, the total planned spending is \(8 + 12 + 5 = 25\). That means \(30 - 25 = 5\) is still available. A good budget makes sure spending does not go above income.

Budgets often include fixed expenses and variable expenses. Fixed expenses stay about the same each time, such as a monthly streaming fee. Variable expenses change, such as money spent on snacks, gifts, or hobbies. Families also separate needs, like housing and food, from wants, like extra treats or the newest phone case.

Budgeting is not about never having fun. It is about making thoughtful choices. If someone knows a class trip costs $40 in one month, budgeting helps break that big goal into smaller parts. Saving $10 each week for four weeks gives \(10 \times 4 = 40\), which reaches the goal on time.

Worked example: Creating a simple weekly budget

A student has $35 for the week. The student wants to save $10, spend $9 on lunch treats, and spend $6 on a small gift. How much money remains?

Step 1: Add the planned uses of money.

\(10 + 9 + 6 = 25\)

Step 2: Subtract from total money available.

\(35 - 25 = 10\)

The student has $10 left. That extra money could stay unspent, be added to savings, or be planned for another need.

When many consumers budget carefully, businesses notice. Stores may see customers buying fewer unnecessary items and more basic needs. Companies then adjust what they stock, advertise, and produce. In that way, personal budgeting not only helps one person. It also sends signals to producers about what people value most.

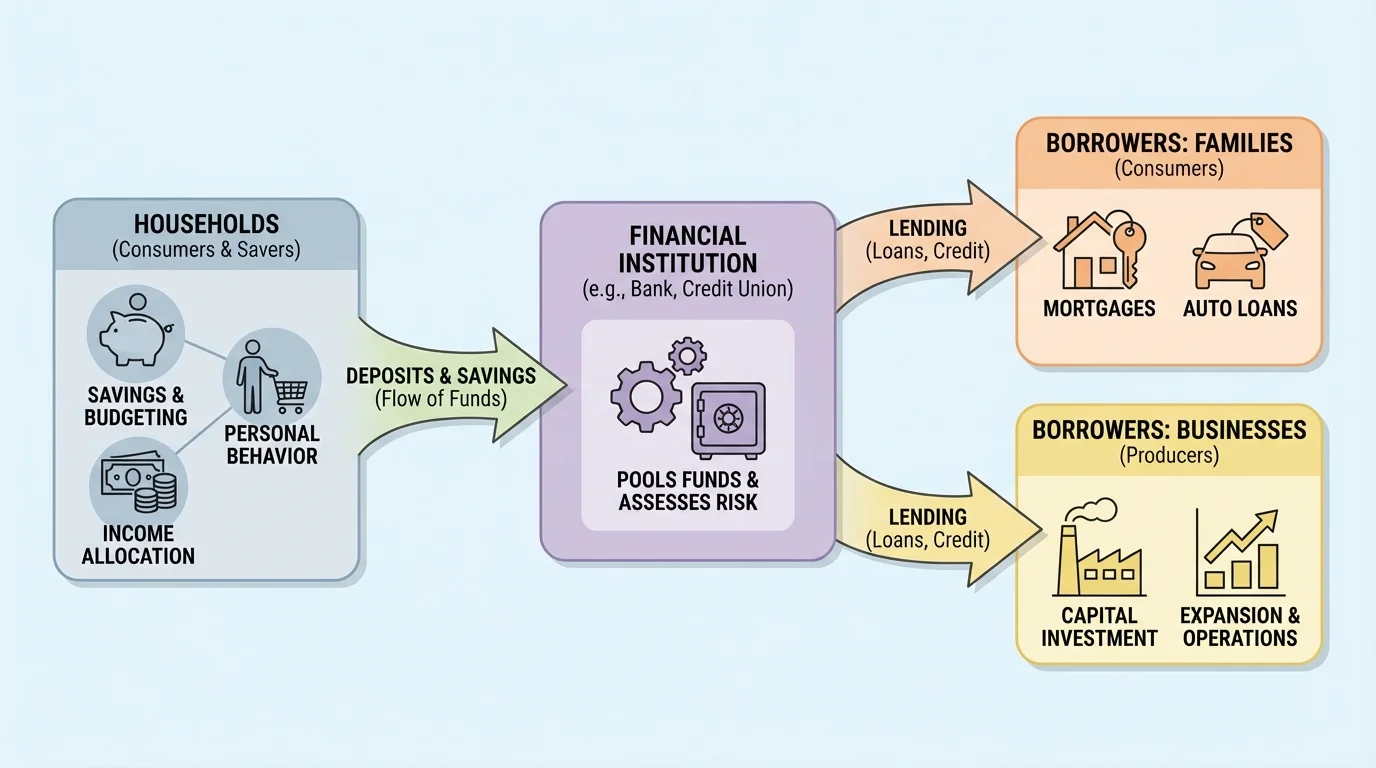

Saving means putting aside money for later. This could be for a short-term goal, such as headphones, or a long-term goal, such as college or a car years later. Saving also helps with surprises, such as a broken backpack zipper, a bike repair, or a family emergency. Saving matters beyond one person because, as [Figure 2] illustrates, money saved in banks can help support loans in the wider economy.

People save for different reasons. One person may save to avoid borrowing. Another may save because waiting makes a purchase more thoughtful. Saving builds security. Instead of feeling pressure to spend immediately, a saver has more choices later.

Banks and credit unions are important because they keep money safe and may pay a small amount of interest. Interest is money earned for keeping money in an account. If a savings account starts with $100 and earns $2 in interest, the new balance is \(100 + 2 = 102\). The amount is small in this example, but over time savings can grow.

When many people place savings in banks, those financial institutions can lend part of that money to families and businesses. A family might borrow to buy a car. A business might borrow to buy new machines or open another store. That means saving helps more than the saver; it can also support growth, jobs, and production in the economy.

There is also an opportunity cost to every saving decision. If you save $15 instead of buying a game today, the opportunity cost is the fun of having the game right now. But if that saving helps you buy something more important later, the trade-off may be worth it.

Even small savings can become meaningful. Saving $5 each week for ten weeks gives \(5 \times 10 = 50\), enough for a class fee, a gift, or a contribution toward a larger goal.

Saving also affects businesses. If many people decide to save more and spend less for a while, stores may sell fewer nonessential items. Businesses may respond by lowering prices, creating sales, or producing different goods. Later, when people feel ready to spend again, businesses may hire more workers or expand.

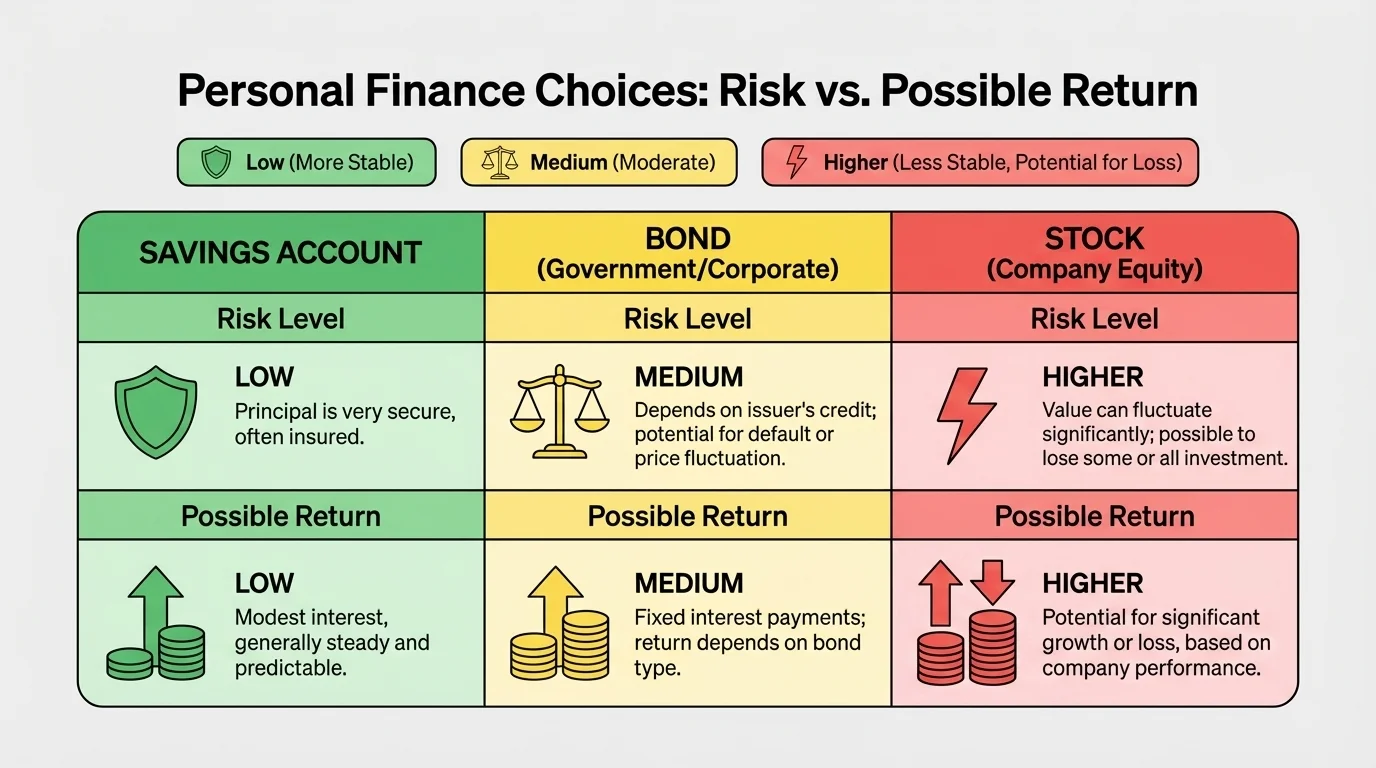

Saving usually focuses on safety and short-term or medium-term goals. As [Figure 3] shows, investing usually focuses on growth over a longer time. When people invest, they put money into things such as stocks or bonds with the hope that the value will increase or produce income.

Risk means the chance that money could lose value or grow less than expected. Return means the gain an investment may earn. A savings account is usually low risk and low return. A bond is often medium risk. A stock can be higher risk, but it may also have higher return over time.

A stock is a small share of ownership in a company. If a company does well, the value of the stock may rise. If the company struggles, the stock value may fall. A bond is money loaned to a government or company, which usually promises to pay it back later with interest.

Why does investing matter to the economy? Businesses need money to grow. They may need new tools, buildings, trucks, websites, or workers. Investment provides some of that money. So when people invest, they are not just trying to grow personal wealth. They are also helping fund business activity, production, and innovation.

Worked example: Comparing two money choices

A student has $50. Choice A is to keep all $50 in savings. Choice B is to invest $20 and keep $30 in savings. How much remains in savings in Choice B?

Step 1: Identify the part kept in savings.

Total money is $50, and $20 is invested.

Step 2: Subtract the invested amount.

\(50 - 20 = 30\)

Choice B leaves $30 in savings. This example shows that people often balance safety and growth instead of choosing only one.

Young students usually are not making major investments yet, but they can understand the idea. Adults who invest in businesses may help those businesses open factories, create apps, improve farms, or sell products across the Western Hemisphere. The flow of investment helps connect consumers, workers, and producers.

Money decisions are not only about numbers. They are also about behavior. Some behaviors help people make strong choices, while others make spending harder to control. For example, impulse buying happens when someone purchases something quickly without careful thought. Advertising, social pressure, and online shopping can all increase impulse buying.

Responsible money behavior includes comparing prices, checking quality, reading labels, and asking whether an item is really needed. If one store sells a notebook for $3 and another sells a similar notebook for $2, the difference is \(3 - 2 = 1\). Choosing carefully saves $1, and those dollars add up over time.

Borrowing is another behavior area. Borrowing can help when used wisely, but it can become a problem if people borrow more than they can repay. Older students and adults often learn about credit cards, loans, and interest payments. The key idea is simple: money used now may cost more later.

Smart money habits grow over time. Planning before shopping, avoiding pressure from ads, saving before spending on wants, and asking whether a choice matches a goal are habits that protect people from poor decisions. These habits also make consumers more thoughtful, which pushes businesses to compete through better prices and quality.

Businesses pay close attention to consumer behavior. If shoppers start choosing products that last longer, companies may improve durability. If buyers prefer local produce or eco-friendly packaging, producers may change how goods are grown, shipped, or wrapped. Consumer behavior becomes a kind of message to the market.

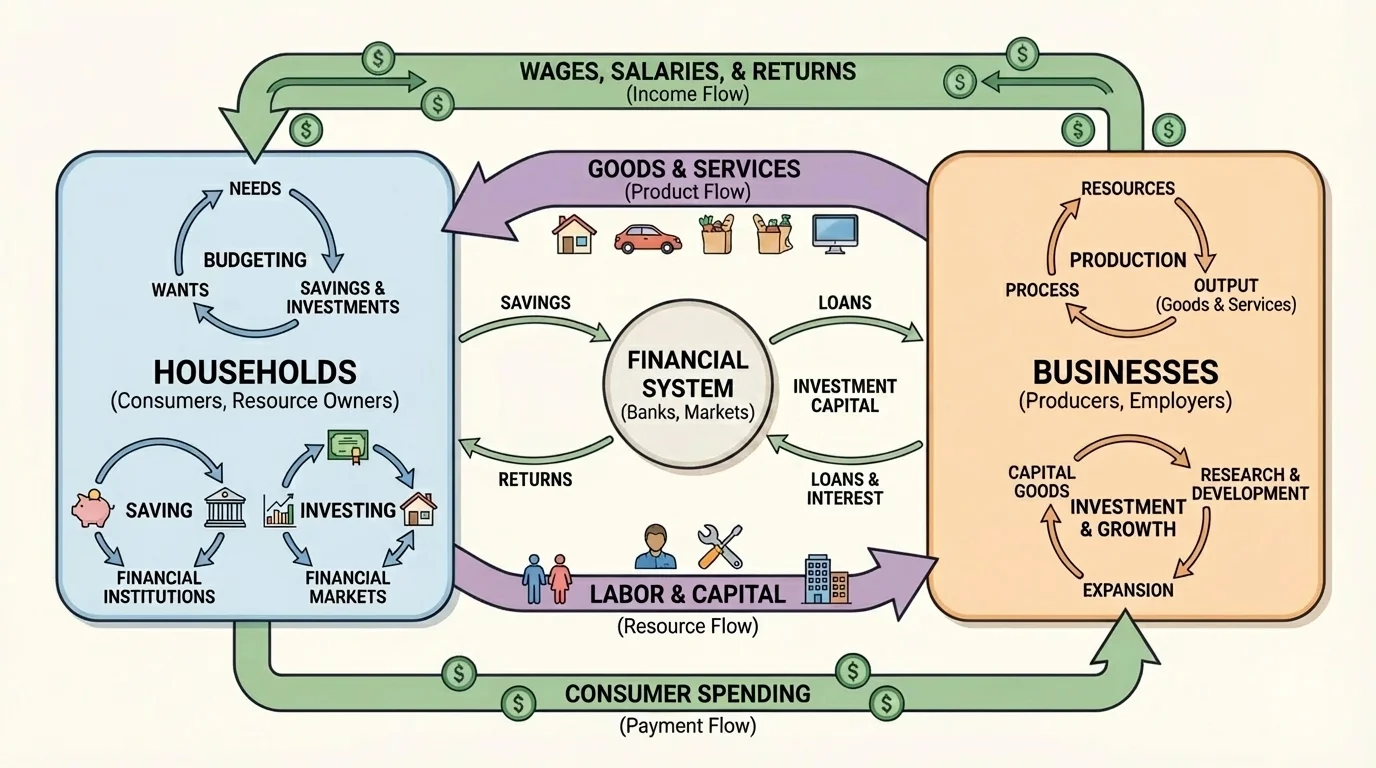

The economy is like a giant network of exchanges between households and businesses. As [Figure 4] illustrates, consumers spend money on goods and services, while businesses pay wages and create products. This circular movement means one person's spending becomes someone else's income.

Suppose many families in a town begin buying more bicycles. Bike shops may order more bikes. Factories may produce more parts. More workers may be needed to assemble, ship, or sell the bikes. This chain reaction shows how demand affects production.

The opposite can also happen. If many consumers stop buying a certain product, businesses may make less of it. They might cut prices, create a new version, or stop producing it. In this way, consumer choices help answer the economic questions of what to produce, how much to produce, and for whom to produce it.

This pattern matters across the Western Hemisphere. If shoppers in one country want more coffee, cocoa, or fruit, producers in another country may increase output. If transportation costs rise, prices may also rise. If people save more and businesses borrow for expansion, investment can support new production in many regions.

| Personal action | Direct effect on the person | Possible effect on the economy |

|---|---|---|

| Creating a budget | Controls spending | Signals businesses about what consumers really want |

| Saving money | Builds security for future needs | Provides funds that banks can lend |

| Investing money | May grow wealth over time | Helps businesses expand and produce more |

| Impulse buying | Can reduce money for important goals | May encourage short-term demand for unnecessary items |

| Comparing prices | Saves money | Pushes businesses to compete on price and quality |

Table 1. Examples of how personal financial choices connect to the larger economy.

Later in the lesson, the same circular relationship from [Figure 4] helps explain why jobs, prices, and business decisions change when consumer behavior changes. The economy is not controlled by one person alone, but millions of choices together have real power.

Many people think children are only consumers, but that is not always true. Students may act as consumers when they buy lunch, games, or school supplies. They may also act as producers if they do chores for pay, babysit, sell handmade crafts, mow lawns, tutor younger children, or create digital art.

When someone produces a good or service, even on a small scale, that person begins to understand costs and choices from the business side. A student selling bookmarks for $2 each may need to buy paper and markers first. If supplies cost $6 and the student sells 5 bookmarks for $2 each, total revenue is \(5 \times 2 = 10\). The amount left after the cost of supplies is \(10 - 6 = 4\).

Worked example: Small producer decision

A student makes bracelets to sell. Supplies cost $8. The student sells 6 bracelets for $3 each. How much money is left after paying for supplies?

Step 1: Find total money earned.

\(6 \times 3 = 18\)

Step 2: Subtract the cost of supplies.

\(18 - 8 = 10\)

The student has $10 left. This simple example shows how producers must think about both money coming in and money going out.

Understanding both roles is powerful. Consumers decide what to buy. Producers decide what to make and how to sell it. Sometimes the same person is both. A bakery owner is a producer when selling bread, but also a consumer when buying flour, sugar, and electricity.

Good money decisions usually follow a process. First, identify the goal. Second, compare choices. Third, think about short-term and long-term effects. Fourth, consider the opportunity cost. Fifth, decide whether the choice fits the budget.

For example, if a student has $25 and wants either a $25 game today or to save for a $40 sports item later, the student can ask: What do I want more? How long am I willing to wait? How much more do I need? The remaining amount needed for the sports item is \(40 - 25 = 15\). That calculation helps make the decision clearer.

Strong financial literacy does not mean never spending money. It means spending, saving, and investing with purpose. Thoughtful consumers help businesses improve. Careful savers support future security and lending. Long-term investors can support business growth. Responsible producers learn how costs, prices, and customer demand work together.

"When you choose how to use your money, you are also choosing what kind of economy you help build."

That idea is true whether the choice is small or large. Buying local fruit may support nearby farmers. Saving money in a bank may support loans for homes or businesses. Comparing prices may push stores to compete fairly. The economy grows and changes through the daily actions of ordinary people.