Have you ever looked at your money and thought, "I barely bought anything, so where did it go?" That happens to a lot of people. Small purchases add up fast, especially when you do not have a plan. A budget is not about making life boring. It is about telling your money where to go before it disappears on random snacks, game purchases, delivery fees, or subscriptions you forgot about.

Learning to budget early gives you a real advantage. If you know how to manage $20, $100, or $300 now, you will be much more prepared when you start earning more money later. Budgeting helps you avoid stress, save for things you care about, and make smarter choices instead of rushed choices.

A personal budget is a plan for your money. It shows how much money you have coming in, how much is going out, and how much you want to save. When you budget well, you are less likely to run out of money before the end of the week or month. You are also more likely to reach goals like buying new headphones, saving for a trip, building an emergency fund, or having money ready for gifts and events.

Without a budget, money decisions often become emotional. You might spend because you are bored, trying to keep up with friends online, or reacting to a sale. With a budget, you switch from guessing to planning. That gives you more freedom, not less.

"A budget is telling your money where to go instead of wondering where it went."

— Common personal finance saying

That quote matters because money management is not only about math. It is about habits. Even simple habits, repeated over time, can make a big difference.

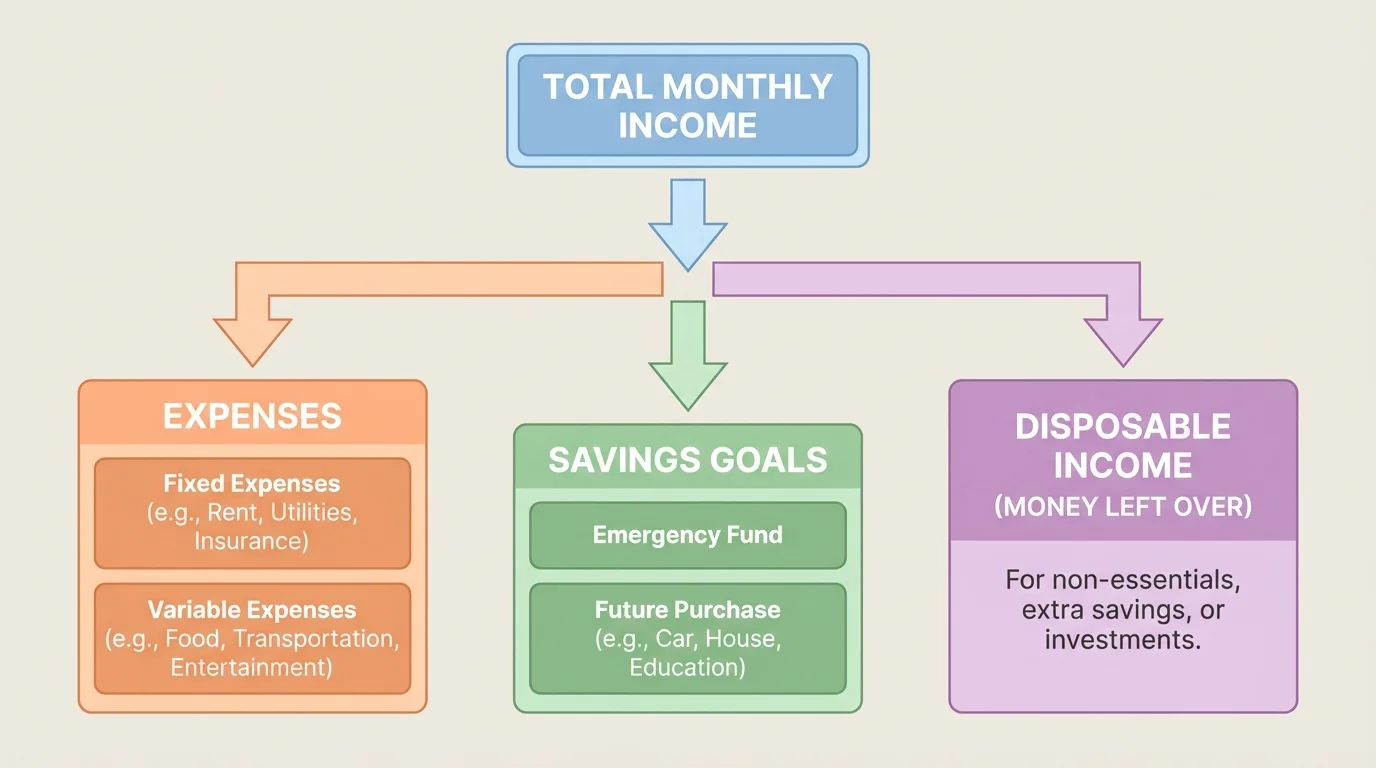

[Figure 1] Every budget is built from three connected parts: income, expenses, and savings goals. If one part is missing, your plan will not be complete. You need to know how much money comes in, what it needs to cover, and what part of it you want to keep for the future.

Income is the money you receive. For a teenager, that might come from allowance, babysitting, pet sitting, yard work, selling handmade items online, birthday money, or a part-time job.

Expenses are the things you spend money on. Some expenses are necessary, like toiletries, transportation, school supplies, or a phone bill. Others are optional, like snacks, streaming subscriptions, game add-ons, or clothes you want but do not urgently need.

Savings goals are the amounts you set aside for future use. A savings goal could be short-term, like saving for concert tickets, or longer-term, like building an emergency cushion or saving for a laptop.

Budget means a plan for how you will use your money. It includes what you earn, what you spend, and what you save.

Needs are expenses that matter for daily life or responsibilities. Wants are things you enjoy but could delay, reduce, or skip if needed.

A good budget does not have to be complicated. In fact, the simpler it is, the more likely you are to actually use it.

Your first job is to find out how much money you actually have available. This sounds obvious, but many people budget based on what they hope to get instead of what they realistically receive.

Start by listing all the sources of money you usually get in a month. If your income is steady, this is easy. If it changes, estimate an average. For example, if you earned $40 one month, $60 the next month, and $50 the month after that, your average monthly income is

\[\frac{40 + 60 + 50}{3} = \frac{150}{3} = 50\]

So a realistic monthly estimate would be $50.

Be honest here. Do not count money that is uncertain. If your aunt sometimes sends you money or you might get extra hours helping a neighbor, that should not be part of your main budget unless it happens regularly.

If someone else gives you money for a specific purpose, treat it carefully. For example, if a parent gives you $15 for transportation or lunch, that is not the same as free spending money. It already has a job.

Income example

Jordan gets $25 each month for allowance and earns money from pet sitting. In the last three months, pet-sitting income was $30, $10, and $20.

Step 1: Find average pet-sitting income.

\[\frac{30 + 10 + 20}{3} = \frac{60}{3} = 20\]

Step 2: Add regular allowance.

\[25 + 20 = 45\]

Jordan should build a monthly budget based on about $45, not on a lucky high month.

Using an average protects you from planning too much spending on money that may not show up.

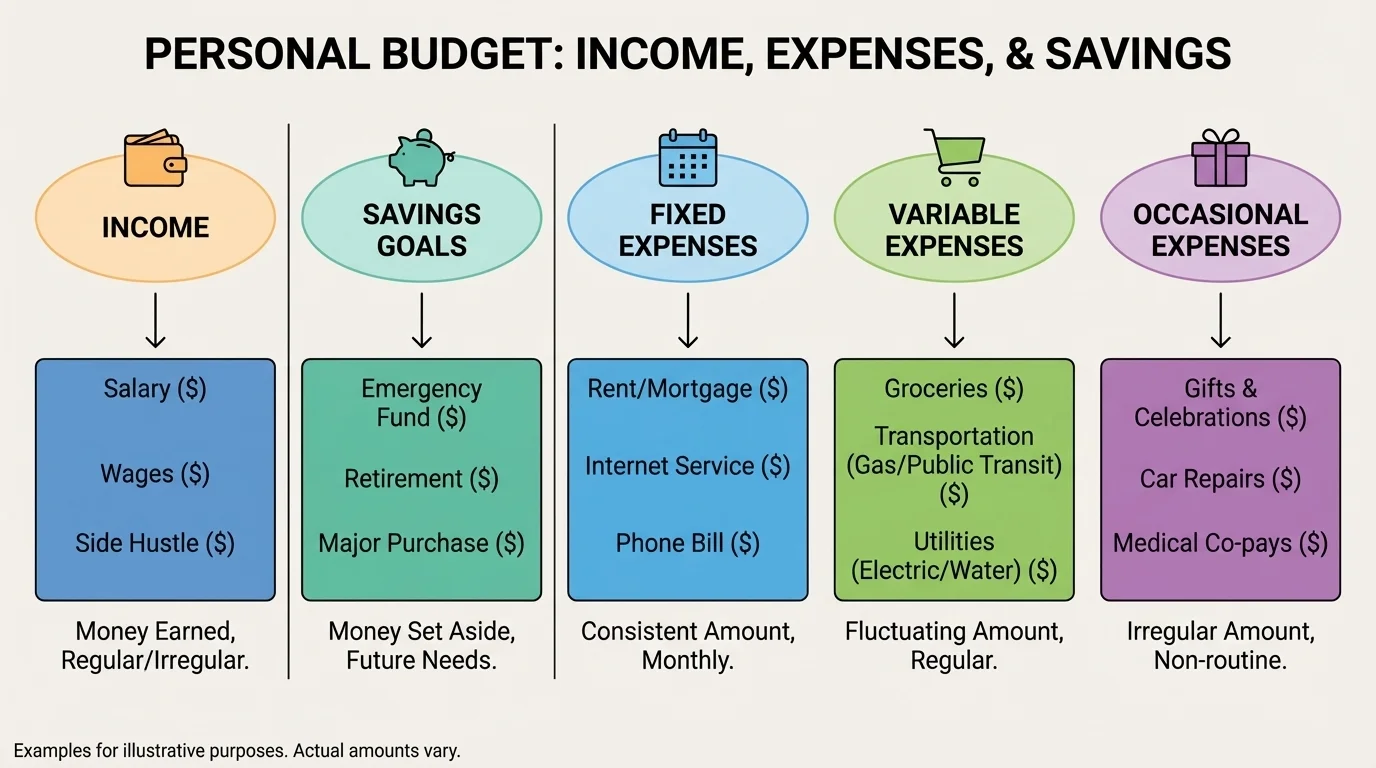

[Figure 2] Once you know your income, the next step is organizing your spending. The three most useful expense groups are fixed expenses, variable expenses, and occasional expenses. Sorting them makes your budget easier to understand and adjust.

Fixed expenses stay about the same each month. If you pay $10 every month for a music subscription or $20 toward your phone, that is fixed.

Variable expenses change from month to month. Snacks, entertainment, clothing, and hobby spending often fit here. You might spend $8 one week and $20 another week.

Occasional expenses do not happen every month, but they still matter. Gifts, holiday shopping, replacing headphones, club fees, or special events belong in this category.

It also helps to separate needs from wants. A need is something important for your responsibilities or basic routine. A want is something you enjoy but can live without for now. Sometimes the same item depends on context. A basic phone plan might be a need for communication and safety, while extra paid app features might be a want.

One of the biggest budgeting mistakes is forgetting small expenses. A $4 drink, a $3 game add-on, and a $6 delivery fee may seem tiny, but together they matter. If you do that several times a week, the total can surprise you.

| Category | Example | Type | Need or Want? |

|---|---|---|---|

| Phone payment | $15 monthly | Fixed | Usually need |

| Snacks | $5 to $12 weekly | Variable | Usually want |

| Streaming subscription | $8 monthly | Fixed | Want |

| Birthday gift | $20 once in a while | Occasional | Important planned expense |

| Bus fare | $10 monthly | Fixed or variable | Need |

Table 1. Examples of expense categories and how they may be classified in a personal budget.

Subscriptions are one of the easiest expenses to forget because they often renew automatically. A small monthly charge can keep draining money long after you stop using the service.

That is why reviewing bank app notifications, digital wallet history, or receipts can be so useful. Your memory is not always a reliable money tracker.

Saving is not what you do with "whatever is left." If you wait until the end, there may be nothing left. A better habit is to choose a savings amount first and treat it like an important category.

A savings goal should be specific. "I want to save more" is too vague. "I want to save $120 for new headphones in four months" is much better. That goal tells you exactly what you are aiming for.

To find the monthly amount, divide the total goal by the number of months. If you want $120 in four months, you need to save

\[\frac{120}{4} = 30\]

That means saving $30 each month.

You can create more than one savings goal, but be realistic. If your monthly income is only $50, trying to save $40 while also paying for everything else may not work. A budget should challenge you a little, not set you up to fail.

Pay yourself first means putting money into savings before you start spending on optional things. This works because you are making your future self one of your top priorities, not the leftover priority.

Useful savings categories include short-term goals, larger planned purchases, and emergency savings. Even a small emergency fund matters. If you suddenly need to replace a charger, pay a fee, or handle a surprise expense, saved money keeps the problem from turning into panic.

As you continue budgeting, the three-part structure we saw in [Figure 1] becomes more powerful. Income is not just for spending in the present; part of it should protect your future choices too.

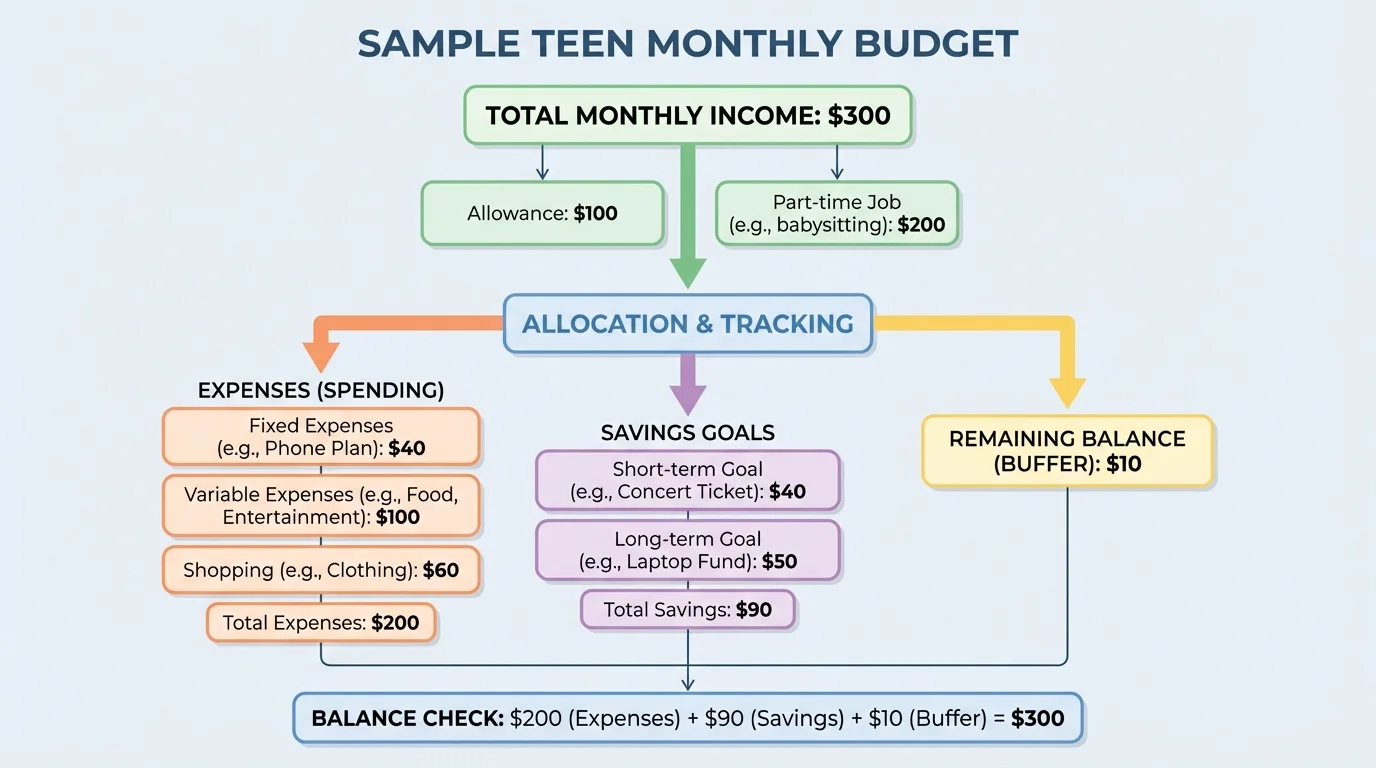

[Figure 3] A written budget works like a map. You start with your total income, subtract planned expenses, and make sure your savings amount is included. If the total planned spending is greater than your income, something needs to change.

Here is the basic budgeting relationship:

\[\textrm{Income} = \textrm{Expenses} + \textrm{Savings} + \textrm{Money Left Over}\]

Some people aim for the money left over to be zero because every dollar has a job. That does not mean you spend everything. It means all of it is assigned somewhere: bills, transportation, spending money, savings, or future expenses.

Suppose your monthly income is $80. You plan $20 for transportation, $15 for snacks, $10 for a subscription, and $25 for savings. Your total planned amount is

\[20 + 15 + 10 + 25 = 70\]

That leaves

\[80 - 70 = 10\]

You can keep that $10 as extra savings, emergency money, or spending flexibility.

If your expenses and savings total more than your income, cut or reduce the least important categories first. Usually that means wants before needs. You might lower entertainment spending, pause a subscription, or stretch a savings goal across more months.

How to build a simple budget

Talia has $90 for the month.

Step 1: List needed expenses.

Phone: $15, transportation: $12, toiletries: $8.

\[15 + 12 + 8 = 35\]

Step 2: Add savings goal.

Talia wants to save $25.

\[35 + 25 = 60\]

Step 3: Find remaining flexible money.

\[90 - 60 = 30\]

Step 4: Split the remaining amount.

Talia plans $15 for snacks, $10 for entertainment, and keeps $5 unassigned.

This budget works because the total planned amount equals the total income.

Budgets do not have to look perfect. They just need to be clear enough that you can use them consistently.

Let's build one complete monthly example. Suppose Eli gets $30 allowance, earns $40 from babysitting, and usually receives about $10 from small online art commissions. Monthly income is

\[30 + 40 + 10 = 80\]

Eli's planned expenses are: phone contribution $15, bus fare $10, snacks $12, streaming subscription $8, and gift/emergency category $5. Total expenses are

\[15 + 10 + 12 + 8 + 5 = 50\]

Eli wants to save $20 for a new controller. If we add that to expenses, we get

\[50 + 20 = 70\]

That leaves

\[80 - 70 = 10\]

Eli could leave that $10 as cushion money or move it into savings. If Eli chooses to save it too, then total savings become $30 instead of $20. As the sample format in [Figure 3] suggests, even a small leftover amount can strengthen your budget when you give it a purpose.

Now picture what happens without a budget. Eli buys extra snacks, forgets the subscription renewal, and spends $18 on impulse game content. By the third week, the controller goal is gone. The problem is not always low income. Often the problem is unplanned spending.

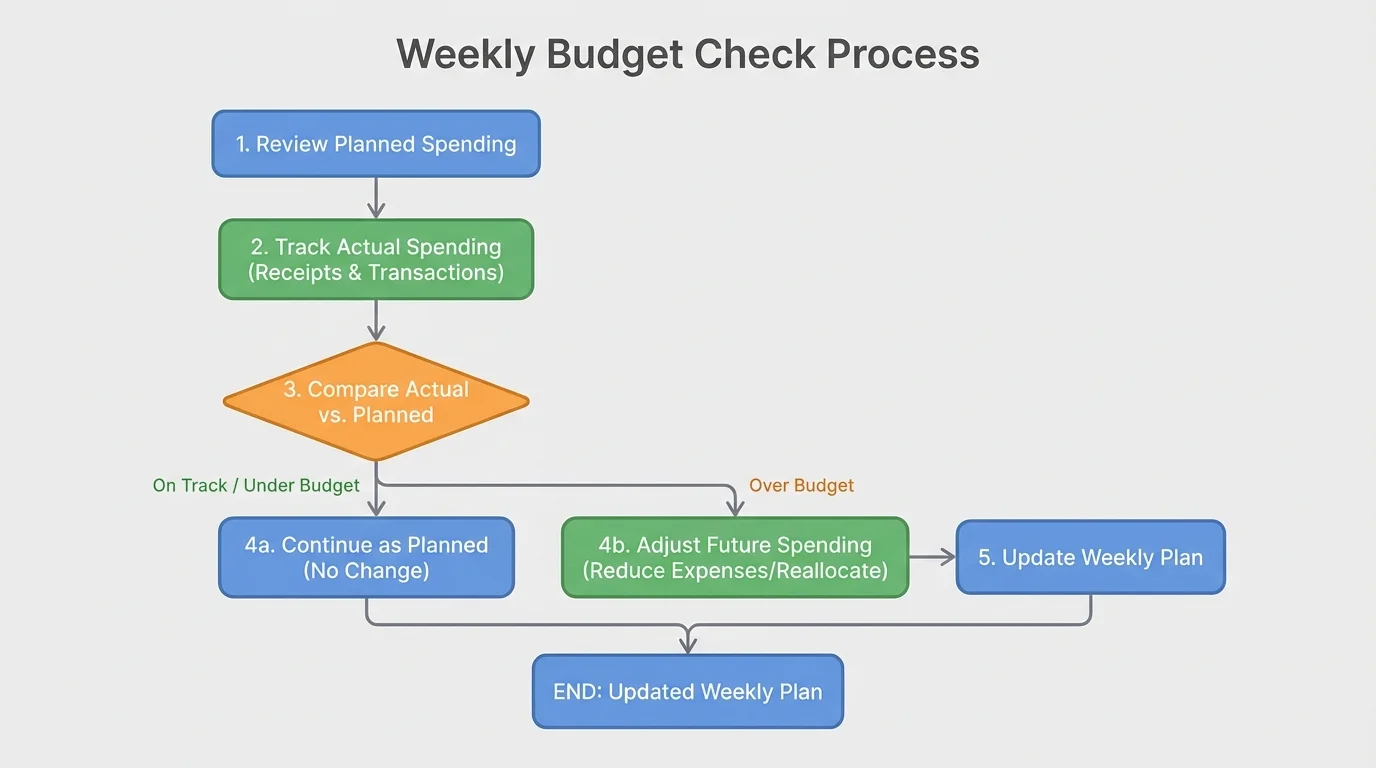

[Figure 4] Budgeting is a plan-check-adjust cycle: plan your spending, compare it with what actually happened, then make changes. Your first budget is not supposed to be perfect. It is supposed to be useful.

A good habit is to check your budget once a week. Look at what you planned and what you actually spent. If you planned $10 for snacks but spent $14, your difference is

\(14 - 10 = 4\)

That means you went $4 over in that category. You now have choices. You can spend $4 less in another category, reduce snack spending next week, or use some unassigned money if you have it.

Tracking can be very simple. You can use a notes app, a spreadsheet, or a paper list. The important thing is to record spending while you still remember it. Waiting until the end of the month makes details blur together.

If you overspend, do not quit. Adjust. That is one of the most important money skills you can build. People often fail with budgets because they treat one mistake like total failure. In reality, a budget is a tool, not a test.

Weekly adjustment example

Sam planned $12 for fun spending this week but spent $16.

Step 1: Find the difference.

\(16 - 12 = 4\)

Step 2: Choose an adjustment.

Sam decides to reduce next week's fun spending by $2 and snacks by $2.

Step 3: Prevent a repeat.

Sam turns off one shopping app notification and waits one day before buying non-urgent items.

The budget recovers because Sam responds quickly instead of ignoring the problem.

The cycle in [Figure 4] matters because real life changes. A strong budget is flexible, not frozen.

One smart habit is to separate your money mentally or digitally into categories. If you know $25 is for savings, do not treat it like spending money just because it is still in the same account.

Another smart habit is the pause rule. Before buying a want, wait a little. For a small purchase, maybe wait a day. For a bigger one, wait a week. This reduces impulse decisions.

Common mistakes include forgetting occasional expenses, making savings goals too ambitious, ignoring tiny purchases, and copying someone else's spending style. Your budget should fit your income and priorities, not someone else's social media life.

Simple subtraction and addition are the core math skills behind budgeting. If you can total categories and compare planned amounts with actual amounts, you already have the main math you need.

Another mistake is treating all income like spending money. Remember the structure from [Figure 1]: income needs to cover expenses and savings, not only fun purchases.

You do not need expensive software to budget. A notes app can work. A spreadsheet can work. A budgeting app can work. Even a simple table in a notebook can work.

Choose the tool you are most likely to keep using. If a fancy app feels confusing, it may not help. If a plain checklist keeps you consistent, that is a better tool for you.

| Tool | Best For | Possible Downside |

|---|---|---|

| Notes app | Fast tracking on your phone | Less organized over time |

| Spreadsheet | Easy math and monthly totals | Takes setup time |

| Budgeting app | Automatic tracking and alerts | May be too detailed or require linking accounts |

| Paper budget | Simple and visual | Harder to update quickly |

Table 2. Common budgeting tools and the strengths and weaknesses of each option.

A tool is only useful if you check it regularly. Consistency beats complexity almost every time.

Many teens do not receive the exact same amount every month. That is normal. If your income changes, build your budget around a lower, more reliable amount. Then, when you earn extra, decide where it goes on purpose.

For example, if your income is sometimes $40, sometimes $70, and sometimes $55, you might budget based on the safer amount of $40 or on an average if the pattern is steady enough. Extra income can then be divided among savings, occasional expenses, and flexible spending.

This approach protects you from overcommitting. It is much better to be pleasantly surprised by extra money than to be stressed because you planned to spend money you never received.

People with irregular income often benefit even more from budgeting than people with steady income, because planning helps smooth out the unpredictable months.

As your life changes, your budget should change too. New goals, new costs, or new sources of income all deserve updates. That does not mean your old budget failed. It means you are using it the right way.

When you build a budget, you are practicing decision-making, self-control, planning, and independence all at once. Those skills matter whether you are managing $25 now or much more later. Start simple, stay honest, and keep adjusting. That is how a budget becomes something you actually live by instead of something you meant to do once and forgot.