Have you ever had a few dollars and felt pulled in two directions at once? Maybe one part of you wanted a treat right now, while another part wanted to save for something bigger later. That small moment actually involves an important kind of thinking. Every time you choose what to do with money, you are making a financial decision, and that decision can lead to good results, hard results, or a mix of both.

A financial decision is a choice about money. Kids make financial decisions too. You might decide whether to buy a snack, save birthday money, put coins in a class fundraiser, or spend allowance on a small toy. Even when the amount of money is small, the choice still matters.

Money choices matter because you usually cannot use the same money twice. If you spend $4 on stickers, then you no longer have that same $4 to save for a book. If you save $4, then you may need to wait before buying something fun. This is why smart money choices begin with thinking ahead.

Consequence means what happens after a choice. A consequence can be positive, which means helpful or good, or negative, which means unhelpful or not so good.

Benefit is a good part of a choice. Cost is what you give up, spend, or lose when you make that choice.

Sometimes a choice has more than one consequence. Buying a snack may taste good right away, but it may also mean you have less money later. Saving your money may feel slow now, but it can help you reach a bigger goal. Good decision-makers think about both sides.

A positive consequence is a result that helps you. For example, if you save your money, then you may have enough later for a game you really want. If you compare prices, then you may keep more money in your pocket.

A negative consequence is a result that causes a problem or makes a goal harder to reach. For example, if you spend all your money on the first thing you see, then you may not have enough left for something more important. If you lose track of your money, then you may not know whether you can afford something.

Some consequences happen fast, and some happen later. A fast consequence might be getting a toy today. A later consequence might be not having enough money next week. Thinking about now and later helps you make wiser choices.

Many adults use the same skill when they make big choices, such as buying a car or saving for a house. Learning to think about consequences when you are young builds a strong habit for later.

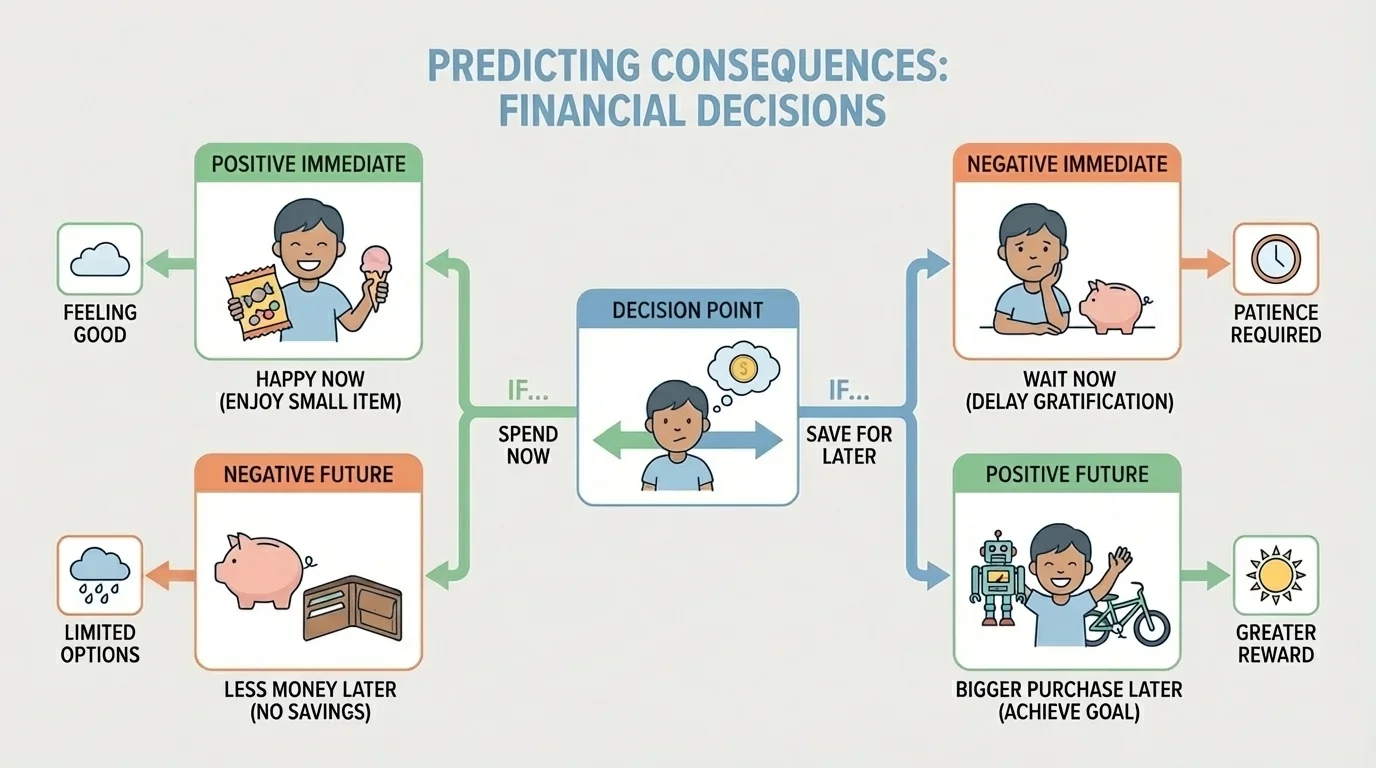

[Figure 1] helps show that consequences are not only about money. A choice might affect your feelings, your time, or other people. For example, sharing money with a cause may leave you with less to spend, but it may help others and make you feel proud.

The If... Then... thinking strategy helps you predict what may happen before you choose. As [Figure 1] shows, one money choice can lead to different results. You can say, "If I do this, then what might happen next?" This gives your brain time to slow down and think carefully.

Here are simple sentence frames: If I spend my money now, then I will have less later. If I save my money, then I may be able to buy something bigger. If I lend money to a friend, then I may get it back later, or I may need to wait.

This kind of thinking is not guessing wildly. It is using clues from what you know. You think about how much money you have, what you want, what you need, and what might happen after your choice.

For example, suppose Mia has $5. She sees a shiny pen for $5 and a puzzle for $8 that she likes even more. She can think: If I buy the pen now, then I will have $0 left. If I save my $5, then I will be halfway to the puzzle. This helps Mia see both the quick reward and the later result.

Children often make money choices in four common ways: spending, saving, sharing, and borrowing. Each one has possible positive and negative consequences.

Spending means using money to buy something. If you spend $3 on a snack, then you get the snack now. That is a positive consequence if you are hungry and the snack is a good choice. But a negative consequence is that you now have $3 less.

Saving means keeping money for later instead of using it now. If you save $2 each week for 4 weeks, then you will have \(2 + 2 + 2 + 2 = 8\) dollars, or $8. A positive consequence is reaching a goal. A negative consequence may be waiting longer for something you want today.

Sharing means giving some money to help others, such as donating to a fundraiser. If you share $1, then you help a cause. That is a positive consequence. A negative consequence is that you have $1 less for your own spending.

Borrowing means using someone else's money or something bought with money and returning it later. If you borrow, then you may get what you need now, but you must remember to return it or pay it back. Borrowing can help in some situations, but it also brings responsibility.

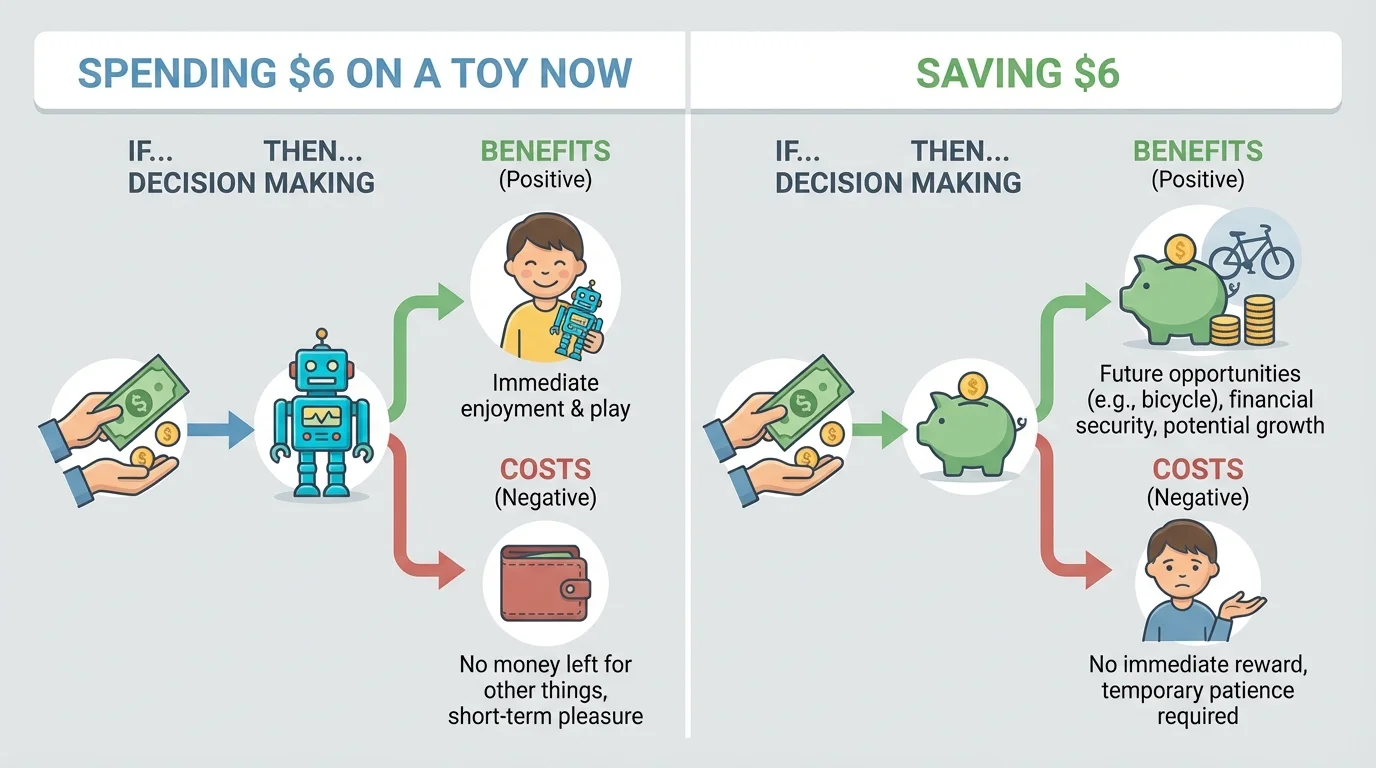

Smart money choices become clearer when you look at cost and benefit together. In the comparison shown in [Figure 2], one choice has good parts and hard parts at the same time. A benefit is the helpful part of a choice. A cost is what you give up. Sometimes the cost is money. Sometimes it is time, waiting, or giving up another choice.

Suppose a toy costs $6 and you have $6. The benefit is that you get the toy now. The cost is that your money becomes $0. If you keep the $6 instead, the benefit is that you still have your money. The cost is that you do not get the toy today.

| Choice | Benefits | Costs |

|---|---|---|

| Buy the toy for $6 | Get the toy now | Have $0 left |

| Save the $6 | Keep money for later | Wait to get the toy |

Table 1. This table compares benefits and costs of buying a toy now or saving the money.

[Figure 2] can help you compare choices by asking questions like these: What do I get? What do I give up? Will this help me now? Will this help me later? Is this a need or a want? A need is something important, like food or school supplies. A want is something you would like to have, such as a game or extra candy.

Sometimes the best choice is not the one that feels exciting first. Looking at costs and benefits helps you notice more than just the fun part. Later, when you compare a new choice, you can remember the chart in [Figure 2] and ask yourself what each path gives and takes away.

Needs and wants help guide money choices. If something is a need, buying it may have a strong benefit because it helps you do something important. If something is a want, saving first may sometimes be the wiser choice. This does not mean wants are bad. It means you think carefully before spending.

For example, if your pencil breaks and you need a new one for school, then buying a pencil may be a smart decision. But if you already have enough pencils and want a glitter one just because it looks fun, then saving your money might be better.

Sometimes you are not choosing between buying and saving. Sometimes you are choosing between two things to buy. Then you can still use If... Then... thinking.

Suppose Leo has $7. He can buy a small ball for $4 or a sketch pad for $7. He thinks: If I buy the ball for $4, then I will have $3 left, because \(7 - 4 = 3\). If I buy the sketch pad for $7, then I will have $0 left, because \(7 - 7 = 0\). Now Leo can think about which result he likes better.

Worked example: choosing between two items

Sara has $9. She wants a puzzle for $5 or a stuffed animal for $9.

Step 1: Find what happens if she buys the puzzle.

If Sara buys the puzzle, then she has \(9 - 5 = 4\) dollars left.

Step 2: Find what happens if she buys the stuffed animal.

If Sara buys the stuffed animal, then she has \(9 - 9 = 0\) dollars left.

Step 3: Compare the consequences.

The puzzle costs less and leaves $4 for later. The stuffed animal uses all of her money but gives her the item she wants now.

Sara can now choose by thinking about which consequence matters more to her.

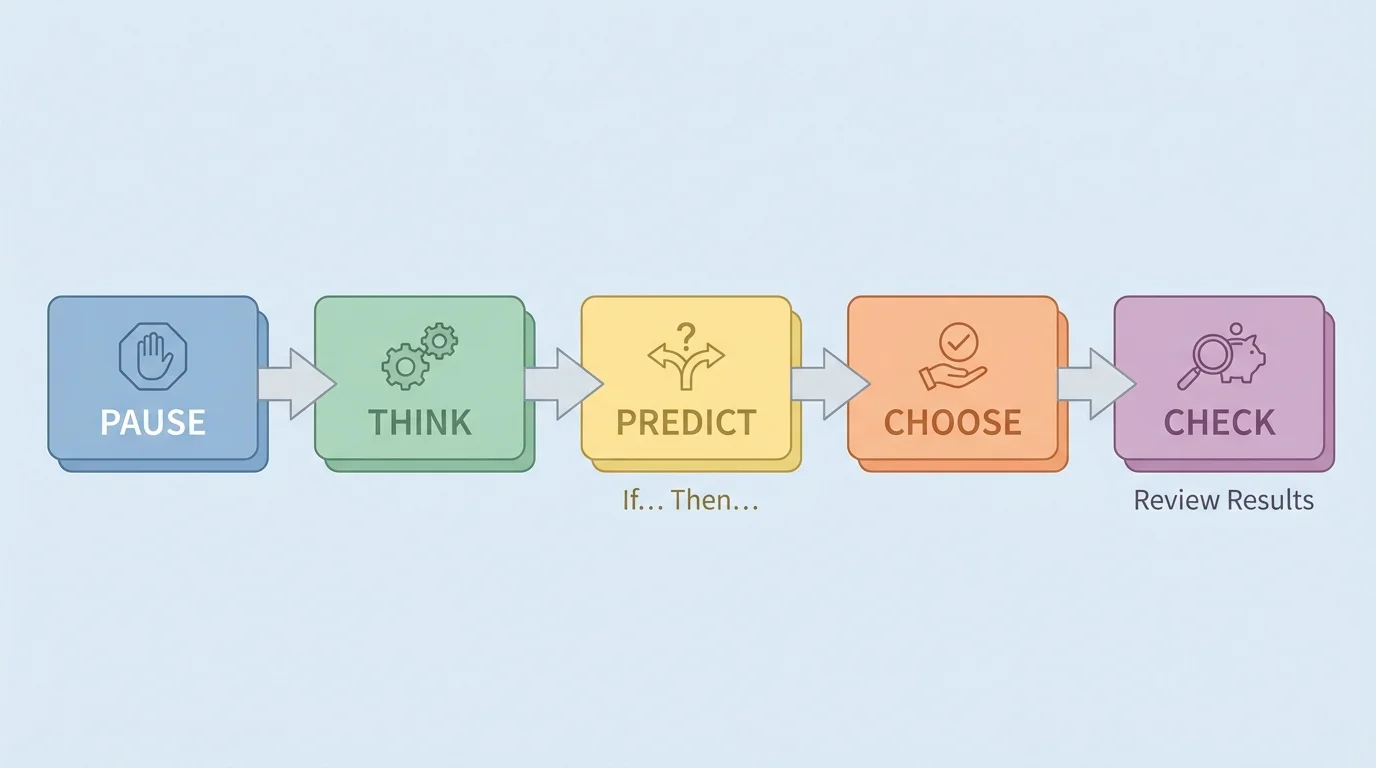

[Figure 3] shows a simple process for slowing down and thinking before you choose. There is not always just one perfect answer. The important thing is to think before you choose. A careful choice is one that matches your goal.

You can follow a simple decision process when money is involved. The steps in [Figure 3] help you slow down, think, and choose. First, pause. Next, say what the choice is. Then predict the consequences. After that, choose. Last, check how the choice worked out.

This process helps because sometimes a choice looks good at first, but the later consequence is not so good. When you pause, you give yourself time to notice both positive and negative results.

You can use these steps in simple words:

Pause: Do not rush.

Think: What are my choices?

Predict: If I choose this, then what may happen?

Choose: Pick the choice that best fits your goal.

Check: Was it a good choice? What did I learn?

Checking your choice matters. If you bought something and later wished you had saved, that teaches you something important. If saving helped you reach a goal, that teaches you too. Good decision-makers learn from old choices to make better new ones.

Remember that subtraction helps you find how much money is left after spending. Addition helps you find how much money you have after saving over time.

For example, if you start with $10 and spend $3, then you have \(10 - 3 = 7\) dollars left. If you save $2 each week for 3 weeks, then you have \(2 + 2 + 2 = 6\) dollars saved.

At a school store, you might see an eraser for $1 and a notebook for $3. If you have $3 and buy the notebook, then you have $0 left. If you buy the eraser, then you have $2 left, because \(3 - 1 = 2\). Which choice is better depends on your goal and what you need more.

At a snack stand, suppose you have $5. One snack costs $2, and another costs $5. If you buy the $2 snack, then you still have $3 left. If you buy the $5 snack, then you have no money left. You can pause, predict, and choose instead of grabbing the first option you see.

Worked example: saving for a goal

Jalen wants a remote-control car that costs $12. He already has $5 and saves $1 each week.

Step 1: Find how much more money he needs.

Jalen still needs \(12 - 5 = 7\) dollars.

Step 2: Connect saving to the goal.

If he saves $1 each week, then after 7 weeks he will save \(1 + 1 + 1 + 1 + 1 + 1 + 1 = 7\) dollars.

Step 3: Predict the consequence.

If Jalen keeps saving, then he will have enough money for the car in 7 weeks.

The positive consequence of saving is reaching the goal. The negative consequence is waiting.

Now think about lending money. If a friend asks to borrow $2, then one positive consequence is helping your friend. One negative consequence is that you may need to wait to get the money back. You should think about whether you trust the person and whether you still need your money for something important.

Sharing money can also be a thoughtful decision. If you donate $2 to an animal shelter fundraiser, then the positive consequence is helping animals. The negative consequence is that you have $2 less for your own spending. Both parts are real, and both matter.

Strong money habits begin with small choices. Ask yourself: Do I need this? Do I want this? What will happen next? What will happen later? Those questions turn a fast choice into a smart one.

Another smart habit is setting a goal. If you know what you are saving for, then it becomes easier to wait. A goal gives your money a job. Instead of disappearing little by little, it starts building toward something important to you.

"Think first, choose next."

— A smart money rule

It also helps to talk about choices with a trusted adult. They may help you notice a consequence you missed. Maybe the cheaper item breaks quickly, or maybe saving a little longer gets you something better. Careful thinkers ask questions before spending.

When you predict positive and negative consequences, you become more confident with money. You do not need to be perfect. You only need to practice thinking ahead. Each time you use If... Then... thinking, you get better at making informed choices.