A lot of adults get into financial trouble not because they are lazy or bad at math, but because they make serious decisions with incomplete information. A paycheck can look big until rent, transportation, food, phone service, and surprise costs hit all at once. The good news is that a responsible money plan is not about being rich. It is about being prepared, realistic, and in control.

If you are about to start working more hours, save for moving out, help your family, or plan for college or training, this skill matters now. Money affects your choices: where you can live, whether you can handle emergencies, and how much stress follows you each month. When you manage money well, you buy yourself time, flexibility, and peace of mind.

A budget is simply a plan for your money before you spend it. It tells your money where to go instead of leaving you to wonder where it went. A responsible plan covers three big areas: work, housing, and future goals. If one of those is missing, your plan is incomplete.

Think about two different students. One earns $1,200 per month, spends freely, and hopes everything works out. The other earns the same amount but plans ahead: $500 for housing help or future rent, $200 for food, $100 for transportation, $150 for savings, $100 for phone and subscriptions, and the rest for personal spending. Both have the same income, but one has direction. The difference is not luck. It is planning.

Net pay is the money you actually receive after taxes and other deductions come out of your paycheck. Fixed expenses are costs that usually stay the same each month, like rent or a phone bill. Variable expenses change from month to month, like groceries or gas. Irregular expenses show up less often, such as car repairs, annual fees, gifts, or school supplies.

One reason people overspend is that they only plan for regular bills. Real life includes costs that may seem unexpected but are often predictable if you think ahead. Your shoes wear out. A pet needs care. You may need interview clothes, an ID replacement, a rideshare home, or a copayment at urgent care. A money-management plan works best when it leaves room for real life, not a perfect fantasy month.

Start with your monthly income. If your hours change, estimate conservatively. If you usually work between \(12\) and \(18\) hours per week at $14 per hour, do not build your plan around the best possible week. Build it around a safer average, such as \(14\) hours per week. Your estimated monthly gross income is \(14 \times 14 \times 4 = 784\), so your plan should probably treat about $784 before taxes as your starting point, not a dream number based on overtime.

Then calculate your monthly net pay. If taxes and deductions remove about $84 from that month, your usable income is \(784 - 84 = 700\). That $700 is what your plan can spend, save, or assign. If you budget with gross income instead of net pay, your numbers will fail immediately.

Next, list every expense category you can think of. Separate them into fixed, variable, and irregular costs. Be honest. If you spend money on gaming, coffee, skin care, streaming, gifts, or eating out, those count. A responsible plan is not about pretending you never spend on enjoyment. It is about deciding the amount on purpose.

| Category | Type | Example monthly amount |

|---|---|---|

| Phone | Fixed | $45 |

| Transportation | Variable | $80 |

| Groceries/snacks | Variable | $120 |

| Streaming/subscriptions | Fixed | $18 |

| Clothes/personal care | Irregular | $40 |

| Emergency savings | Planned savings | $75 |

Table 1. Example categories a student might include in a monthly money-management plan.

As you build your list, notice that savings belongs in the plan just as much as bills do. If you wait to save "whatever is left," there is usually very little left. Responsible money management treats savings as a regular expense you owe your future self.

Your first monthly plan should be simple. The basic idea is that every dollar of your net pay gets a job: bills, essentials, savings, or optional spending. This does not mean you must spend every dollar. It means every dollar is assigned on purpose.

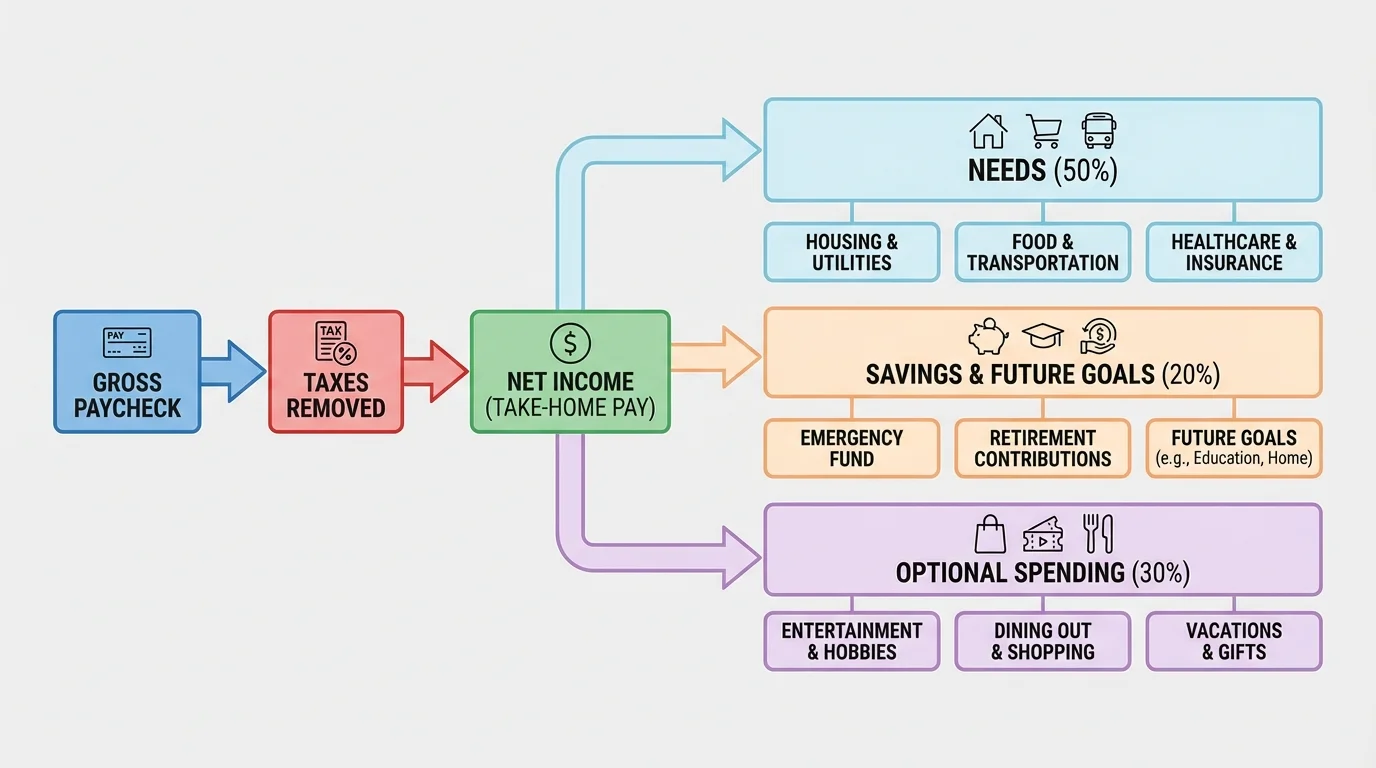

One useful budgeting check, shown in [Figure 1], is this equation: \(\textrm{income} - \textrm{expenses} = \textrm{leftover}\). If the leftover is negative, your plan is not balanced and something must change. For example, if your net pay is \(\$700\) and your planned spending is \(\$760\), then \(700 - 760 = -60\). That means you are short by $60 and need to cut costs, raise income, or delay a goal.

A practical starting approach is to sort spending into three groups: needs, savings, and wants. Needs include housing, food, transportation, medicine, and basic communication. Savings includes emergency money and future goals. Wants are fun purchases, hobbies, entertainment, and upgrades. Different people draw the line differently, but the key is consistency and honesty.

Starter budget example

A student brings home $1,400 per month from part-time work and freelance jobs. They want to help with home costs now and save for moving out later.

Step 1: Cover needs first.

Family contribution $300, transportation $120, food and snacks $180, phone $50, essentials $70. Total needs: \(300 + 120 + 180 + 50 + 70 = 720\).

Step 2: Pay savings next.

Emergency fund $120, future housing fund $200, education or training fund $100. Total savings: \(120 + 200 + 100 = 420\).

Step 3: Decide optional spending.

Entertainment, clothes, and social spending get the amount left over: \(1,400 - 720 - 420 = 260\).

This budget works because the student chooses limits before spending starts.

If your budget feels too tight, that does not mean you failed. It means your budget told you something important. Maybe your hours need to increase. Maybe your transportation plan is too expensive. Maybe you need fewer subscriptions or fewer impulse purchases. A budget is a reality check, not a punishment.

Many people use separate checking and savings accounts, or digital banking tools, to reduce temptation. If your savings automatically moves the same day your paycheck arrives, you are less likely to spend it casually. That single habit often matters more than trying to rely on willpower later.

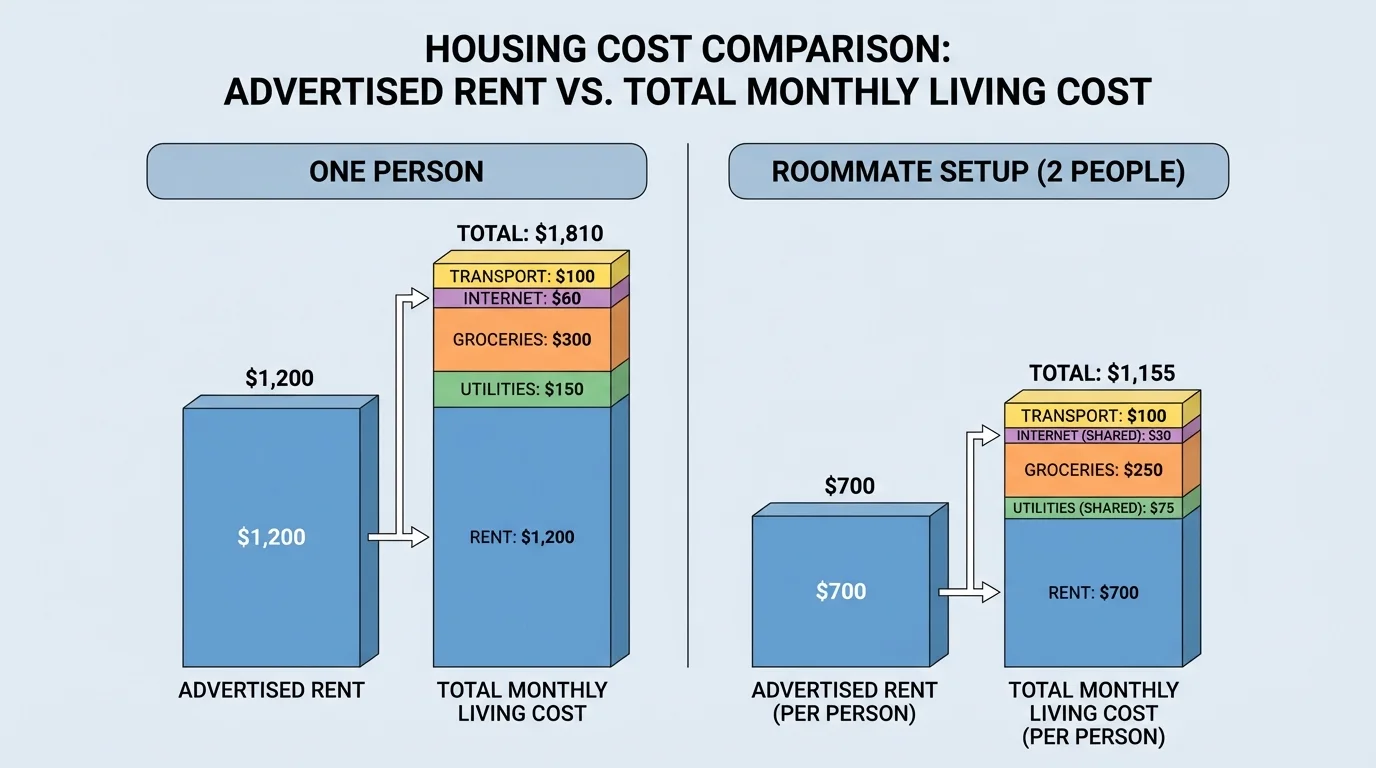

Housing is where many young adults make their biggest financial mistake: they focus on rent and ignore the full monthly picture. The real cost of housing usually includes utilities, groceries, internet, renter's insurance, deposits, furniture, cleaning supplies, and transportation to work.

[Figure 2] Suppose an apartment listing says $850 per month. That number may sound possible. But if utilities are $120, internet is $50, renter's insurance is $15, groceries are $250, and transportation is $140, the true monthly cost becomes \(850 + 120 + 50 + 15 + 250 + 140 = 1,425\). That is a very different decision from "an $850 apartment."

There are also move-in costs. If rent is $850, the security deposit may be another $850. You might also owe an application fee, utility setup fee, and the first month of service for internet or electricity. A move can require more than $2,000 before you even settle in. That is why moving out should be planned, not rushed.

Roommates can lower costs, but only if expectations are clear. If two people split a $1,200 rent evenly, each pays $600. If utilities are $180 total, each pays $90. But if one roommate pays late, damages the place, or leaves early, your financial risk increases. Responsible housing planning is not only about price. It is also about reliability and communication.

Affordable housing is about ratio, not just rent. A place is only affordable if the total cost fits your income while leaving room for food, transportation, savings, and emergencies. If housing takes such a large share of your income that one unexpected bill ruins the month, the housing choice is probably too expensive even if you can technically sign the lease.

Before committing to housing, ask practical questions. How far is it from work? Are utilities included? Is laundry on site? Is public transportation realistic? What fees are nonrefundable? What furniture is already there? Can you handle the move-in cost without emptying your savings? These questions protect you from the common mistake of choosing based on one attractive number or one emotional moment.

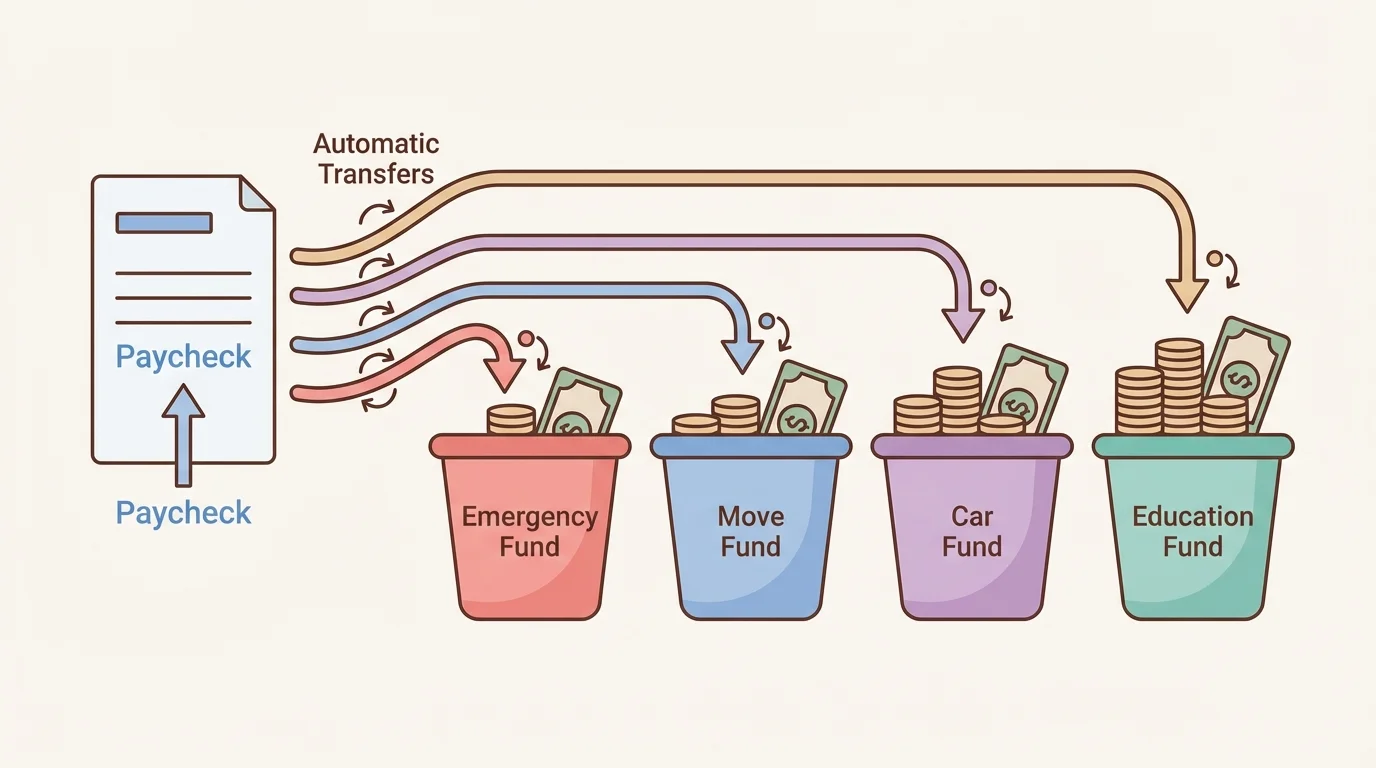

A strong money plan includes an emergency fund and at least one sinking fund. Separating savings by purpose makes it easier to avoid mixing "unexpected crisis money" with "money for a known future expense."

[Figure 3] An emergency fund is money for urgent, unplanned problems: a sudden loss of work hours, medicine, a broken phone you need for work, or a car repair. A sinking fund is money you set aside over time for expenses you know are coming, such as moving costs, holiday gifts, class fees, or replacing tires. Both matter, but they solve different problems.

If you can only start small, start small. Saving $25 from each paycheck is still real progress. If you are paid twice a month and save $25 each time, that is \(25 \times 2 = 50\) per month. Over a year, \(50 \times 12 = 600\). Six hundred dollars will not solve every crisis, but it can prevent a small problem from turning into debt.

A useful first goal is to build a mini emergency fund of $500 to $1,000. After that, you can work toward covering a bigger target, such as one month of essential expenses. If your essentials total $1,200 per month, then one month of coverage means saving $1,200. The exact amount depends on your situation, but the principle stays the same: emergencies are expensive when you have no buffer.

Small recurring savings often beat occasional big efforts. People are more likely to reach savings goals when transfers happen automatically and the money leaves the account before they feel free to spend it.

Later, when you compare your savings choices, remember this idea: one bucket protects you from emergencies, while other buckets move you toward planned goals. That separation helps you make calm decisions instead of stealing from one goal every time another need appears.

A financial goal is a specific money target with a purpose and timeline. "Save more" is too vague. "Save $1,500 for a used car down payment in \(10\) months" is much clearer. When a goal is specific, you can figure out the monthly amount required.

For example, if you want $1,500 in \(10\) months, the monthly target is \(1,500 \div 10 = 150\). If that amount is unrealistic, change the timeline, increase income, or lower the goal. Responsible planning is flexible. It adjusts the plan instead of pretending impossible numbers will somehow work.

Future-goal planning example

A student wants to save $2,400 to move into an apartment in \(12\) months.

Step 1: Break the goal into monthly savings.

\(2,400 \div 12 = 200\). The student needs to save $200 per month.

Step 2: Compare that target with the current budget.

If the budget only has $140 available for future savings, the gap is \(200 - 140 = 60\).

Step 3: Make one practical adjustment.

The student could cut optional spending by $30 and earn an extra $30 through two additional work shifts or a small freelance job.

The goal becomes realistic because the student closes the exact gap instead of guessing.

Your goals might include education, job training, a car, a move, travel, tools for work, or paying for documents and fees that help you become more independent. Goals should match your real values. If you try to save for things just because other people expect them, you may lose motivation fast.

"Do not save what is left after spending; spend what is left after saving."

— Common financial principle

That idea does not mean you ignore basic needs. It means you make your future visible in your plan instead of treating it like an afterthought. Your current self and future self both need support.

Credit can be useful, but it becomes dangerous when people use it to live above their actual income. A credit card is not extra money. It is borrowed money that must be paid back, often with interest. If you carry a balance, the purchase may end up costing much more than the sticker price.

For example, if you charge $300 and then only make small payments while interest keeps adding on, the item can cost far more than $300 over time. Even if the exact rate differs, the lesson is the same: borrowing for wants can trap future income. When next month's paycheck is already promised to past purchases, you lose freedom.

Be especially careful with buy-now-pay-later offers, payday loans, cash advances, and subscription-style payment plans. These are designed to make spending feel easy in the moment. The problem is that your future bills pile up quietly. A plan that looks manageable this week can become stressful after three or four payment commitments overlap.

If you cannot clearly explain how you will repay borrowed money from your normal income, that is a warning sign. Borrowing should solve a necessary problem carefully, not hide the fact that your budget is already stretched.

One smart rule for beginners is this: do not borrow for nonessential purchases unless you can already cover the full cost from your budget or savings. That rule helps you avoid building habits that look normal online but create real long-term stress.

A money-management plan is not something you write once and never revisit. Income changes. Work hours shift. Housing costs rise. Goals become more urgent. Track your spending each month and compare it with your plan. Where did the numbers match? Where did they drift? Those answers teach you more than wishful thinking ever will.

Use simple tools if that helps: a notes app, spreadsheet, banking app, or paper tracker. The best system is the one you will actually keep using. At the end of each month, review three questions: What did I earn? What did I spend? What should change next month? Keep the process short and honest.

Communication matters too. If you share housing, discuss bills before move-in, not after conflict starts. If you need more work hours, ask professionally and early. If a family contribution changes, update your plan the same week. Financial responsibility is not just private math. It also includes clear conversations with the people your money choices affect.

Earlier, [Figure 2] showed why housing costs are bigger than rent alone. That same idea applies when you review your plan: always check the full picture, not just the most obvious number. And the money flow in [Figure 1] still applies every month because each paycheck needs an assignment before it disappears into random spending.

Use this checklist when building or revising your plan.

Step 1: Estimate your monthly net pay using realistic work hours.

Step 2: List fixed, variable, and irregular expenses.

Step 3: Calculate full housing costs, not just rent.

Step 4: Assign money to needs, savings, and optional spending.

Step 5: Build an emergency fund and separate sinking funds.

Step 6: Turn future goals into monthly targets.

Step 7: Avoid debt for nonessential spending when possible.

Step 8: Review and adjust your plan every month.

Responsible money management is not about perfection. Some months will go off track. A good plan helps you recover quickly instead of spiraling. The goal is not to control every penny forever. The goal is to make steady choices that protect your present life and expand your future options.