Two people can borrow the same amount of money and end up in very different financial situations. One may use credit to handle an emergency and repay it efficiently. The other may make small payments for months or years and lose hundreds or even thousands of dollars to interest and fees. That difference is why understanding credit is not just about borrowing money. It is about making choices that protect your budget, your future options, and your financial independence.

Credit affects everyday life more than many students expect. It can help pay for a car, college, housing, or an unexpected medical bill. It can also create long-term problems when a borrower chooses the wrong type of debt, borrows more than they can afford, or ignores the true cost of repayment. Comparing credit options means asking better questions: How fast must the money be repaid? Is the interest fixed or variable? Are there hidden fees? Is something valuable at risk if the borrower cannot pay?

Credit is an agreement in which a lender gives money, goods, or services now and expects payment later. This may sound simple, but the details matter. A borrower is usually paying for two things at once: the original amount borrowed and the cost of borrowing it. That cost may include interest, late fees, annual fees, origination fees, penalties, or other charges.

In personal finance, credit can be useful or harmful depending on how it is managed. Used carefully, it can make large purchases possible and help a person build a strong financial record. Used carelessly, it can trap someone in a cycle where much of each payment goes toward interest instead of reducing the balance. For teenagers and young adults, this is especially important because early credit decisions can affect future access to apartments, car loans, and even some jobs.

Interest is the price paid for borrowing money. Principal is the original amount borrowed. APR, or annual percentage rate, is the yearly cost of credit, including interest and sometimes certain fees, expressed as a percentage. Collateral is property a borrower promises to the lender as security for a loan.

When comparing types of credit, one key idea is affordability. A purchase is not automatically affordable just because the monthly payment seems low. Stretching payments over a longer time may reduce the monthly amount while increasing the total amount paid. A smart borrower looks at both the monthly payment and the full cost over time.

When lenders decide whether to approve someone for credit, they consider creditworthiness, which means how likely the borrower is to repay on time. Lenders often look at income, debt levels, payment history, and a person's credit record. Someone with stronger creditworthiness may qualify for lower interest rates, while someone seen as risky may face high rates or be denied entirely.

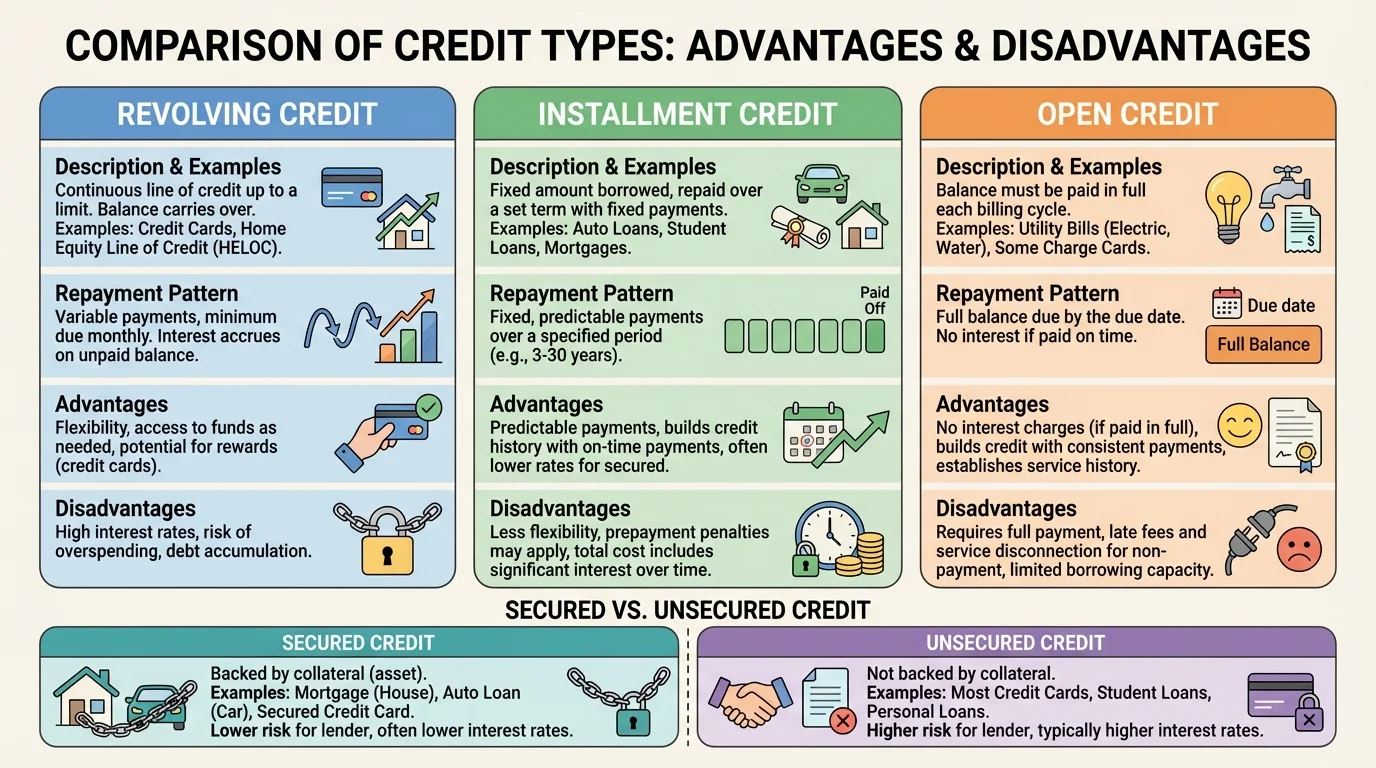

[Figure 1] Different credit products work in different ways. Some let a borrower use funds repeatedly up to a limit. Others provide one lump sum that is repaid in equal installments. Still others require the full balance to be paid each month. Understanding those patterns helps borrowers match the type of credit to the purpose of the borrowing.

Cost of borrowing versus access to opportunity

Credit is not automatically good or bad. It can create opportunity when it helps a person buy something important at a manageable cost, such as transportation for work or education that increases future earnings. It becomes dangerous when the cost of borrowing is extremely high, when payments do not fit the budget, or when debt is used repeatedly for everyday spending without a plan to repay it.

A useful way to think about credit is to separate short-term convenience from long-term cost. A credit card swipe takes seconds. A loan approval online may take minutes. But repayment can last months, years, or even decades. The easiest credit to access is not always the safest credit to use.

Financial products can seem confusing, but the broad categories make them easier to compare. Several of the most important distinctions include the difference between revolving credit and installment credit. Revolving credit allows repeated borrowing up to a set limit. Installment credit gives a fixed amount that is repaid over a scheduled period.

Another category is open credit, which requires the full balance to be paid by a certain date, such as many utility bills or some charge accounts. Credit may also be secured credit, backed by collateral, or unsecured credit, which is based mostly on the borrower's promise to repay and their financial record.

Revolving credit offers flexibility but can be expensive if balances stay unpaid. Installment loans are more predictable, but a borrower is locked into a schedule. Secured loans often have lower interest rates because the lender has protection through collateral, but that also means the borrower could lose the asset.

For example, a credit card is revolving and usually unsecured. An auto loan is installment and usually secured by the vehicle. A mortgage is installment and secured by the home. A utility bill is often open credit because the full amount is expected when due.

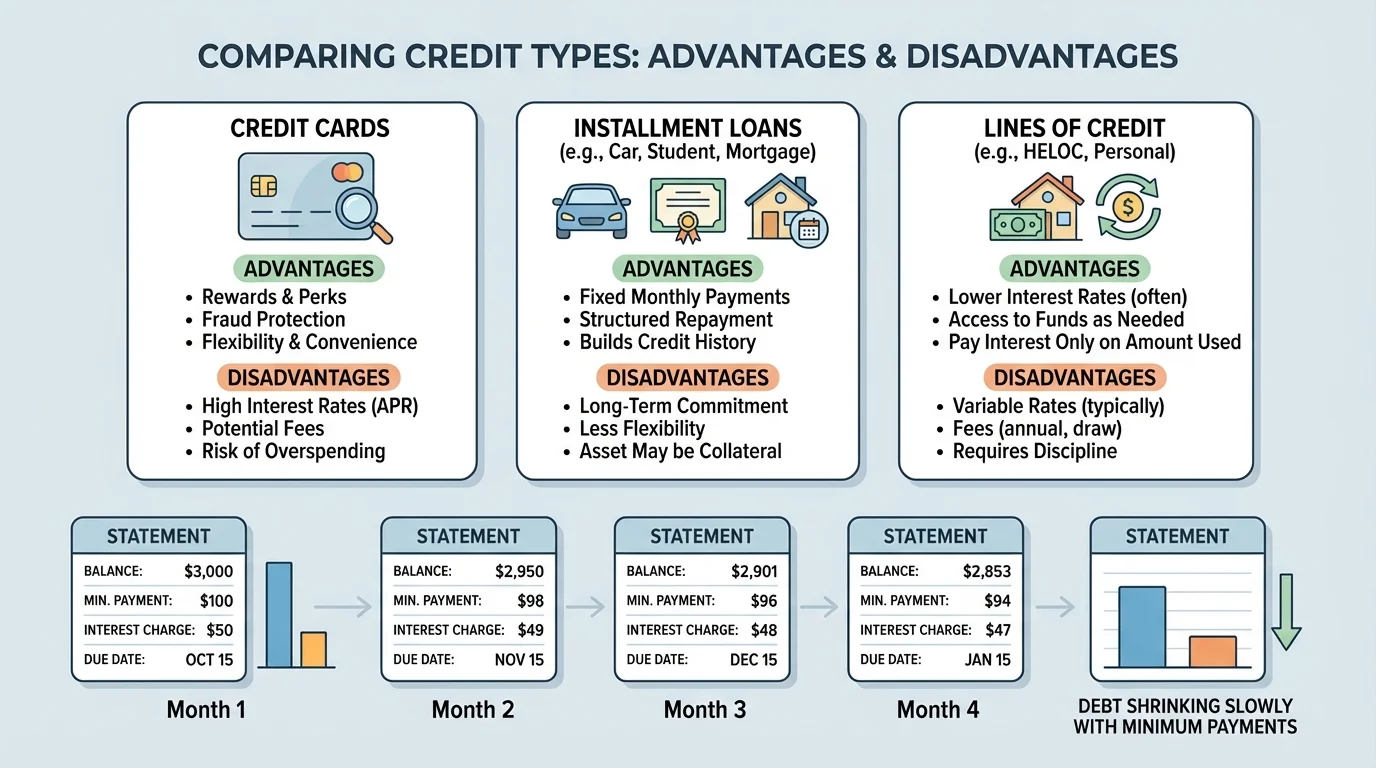

A credit card is one of the most common forms of revolving credit, and [Figure 2] illustrates why it can feel helpful in the short term but expensive in the long term. Credit cards let borrowers make purchases now and pay later, usually up to a credit limit. If the full statement balance is paid by the due date, many cards offer a grace period and charge no interest on those purchases.

The advantages of credit cards include convenience, fraud protection, emergency access, and the ability to build a credit history. They can also provide rewards such as cash back, travel points, or purchase protection. For someone with a budget and discipline, a credit card can be a practical payment tool rather than a source of debt.

The disadvantages appear when the balance is not paid in full. Credit card interest rates are often high. Minimum payments may look manageable, but they can keep a borrower in debt for a very long time. Late payments may trigger fees and damage the borrower's credit profile. Some people also overspend more easily when using a card than when using cash or a debit card.

Suppose Maya puts $600 on a card with an APR of 24% and then pays only $30 each month while continuing to avoid new charges. The monthly interest rate is approximately \(\dfrac{24\%}{12} = 2\%\). In the first month, the interest is about \(0.02 \times 600 = 12\), so only \(30 - 12 = 18\) of her payment reduces the principal. That is the hidden danger of minimum-payment borrowing.

Credit cards are usually best for purchases that can be paid off quickly, especially within the grace period. They are usually a poor choice for long-term debt unless the borrower has a specific payoff plan. The same convenience that makes them useful also makes them risky.

Worked example: comparing full payment and minimum payment

A student charges $500 to a credit card with an APR of 18%.

Step 1: Find the approximate monthly interest rate.

The monthly rate is \(\dfrac{18\%}{12} = 1.5\%\).

Step 2: If the full $500 is paid during the grace period, determine the interest.

Interest is approximately \(0\), so the total cost stays $500.

Step 3: If only $25 is paid and there is no grace-period protection on the carried balance, estimate first-month interest.

Interest is \(0.015 \times 500 = 7.50\), so only \(25 - 7.50 = 17.50\) reduces the balance in the first month.

Paying in full avoids interest. Paying only the minimum makes the purchase cost more and keeps the debt around longer.

As with the slow balance reduction shown earlier in [Figure 2], small monthly payments can create the illusion of progress while the debt remains stubbornly high.

A personal loan is usually an unsecured installment loan. The borrower receives a lump sum and repays it in fixed monthly amounts over a set number of months or years. This predictability is a major advantage. Because the payment schedule is fixed, budgeting is often easier than with revolving credit.

Personal loans can be useful for consolidating higher-interest debt, paying for a major planned expense, or covering an emergency when the borrower can afford the payment. Their disadvantages include possible origination fees, interest costs, and the risk of taking on debt for nonessential spending. A fixed payment is only helpful if it fits the borrower's budget.

Buy now, pay later plans, often called BNPL, are another form of short-term credit. Some plans split a purchase into several equal payments. Others charge interest if the balance is not paid in time. Their biggest advantage is easy access and predictable small payments. Their biggest disadvantage is that they can make a purchase seem cheaper than it really is, leading people to stack multiple payment plans at once.

If a student buys shoes, clothes, and electronics using three separate BNPL plans, each payment may seem small. But the combined total may strain the monthly budget. This is a good example of why budgeting and borrowing decisions must be connected. Credit should fit the budget, not replace it.

An auto loan is usually a secured installment loan. The car serves as collateral, which is one reason interest rates are often lower than those on credit cards. The advantage is that a borrower can buy transportation now and repay over time. Reliable transportation can make it possible to get to school or work, so the purchase may support future income.

The disadvantages include interest cost, depreciation, and repossession risk. Cars lose value over time, sometimes faster than the loan balance falls. A borrower can end up owing more than the car is worth. If payments are missed, the lender may take the vehicle. That makes affordability especially important.

Student loans are often used to pay for education. Their advantage is that they may help a person invest in skills and qualifications that increase future earnings. Some student loans have lower rates or more flexible repayment terms than other loans. Their disadvantages are long repayment periods, accumulating interest, and the possibility of taking on debt without finishing a degree or without earning enough income afterward to manage the payments comfortably.

Some debts are sometimes described as productive because they may help increase future income, but that does not make them automatically safe. A useful purpose does not cancel out a payment that is too large for the borrower's budget.

Borrowers should ask not only whether an item is important, but whether the financing terms are realistic. A car may be necessary, but a shorter loan on a less expensive car may be safer than a longer loan on a more expensive one. Education may be valuable, but borrowing should still be connected to expected costs, completion plans, and future earning potential.

A mortgage is a long-term secured installment loan used to buy a home. The main advantage is that it makes homeownership possible without paying the full price upfront. Monthly payments can gradually build ownership, called equity. Mortgages often have lower rates than unsecured borrowing because the home serves as collateral.

The disadvantages are a serious long-term commitment, large total interest costs over many years, and foreclosure risk if payments cannot be made. A lower monthly mortgage payment does not always mean a better deal. Extending the loan term may lower the payment while increasing the total interest dramatically.

Home equity loans and home equity lines of credit allow homeowners to borrow against the value they have built in a home. These products may offer lower rates than credit cards, but the risk is much greater because the home is tied to the debt. Using home equity for necessary repairs may be different from using it for vacations or nonessential spending.

At the opposite end of the risk spectrum are payday loans and other high-cost short-term loans. These are often marketed as quick solutions for emergencies. Their main advantage is speed and easy approval. Their disadvantages are extremely high fees, very short repayment periods, and a high chance that the borrower will need to borrow again to cover the first loan. This cycle can become financially destructive very quickly.

"The most dangerous debt is often the debt that looks easiest to get."

For most borrowers, payday loans are among the least favorable credit choices because the total cost is so high relative to the amount borrowed. Fast approval is not the same as good value.

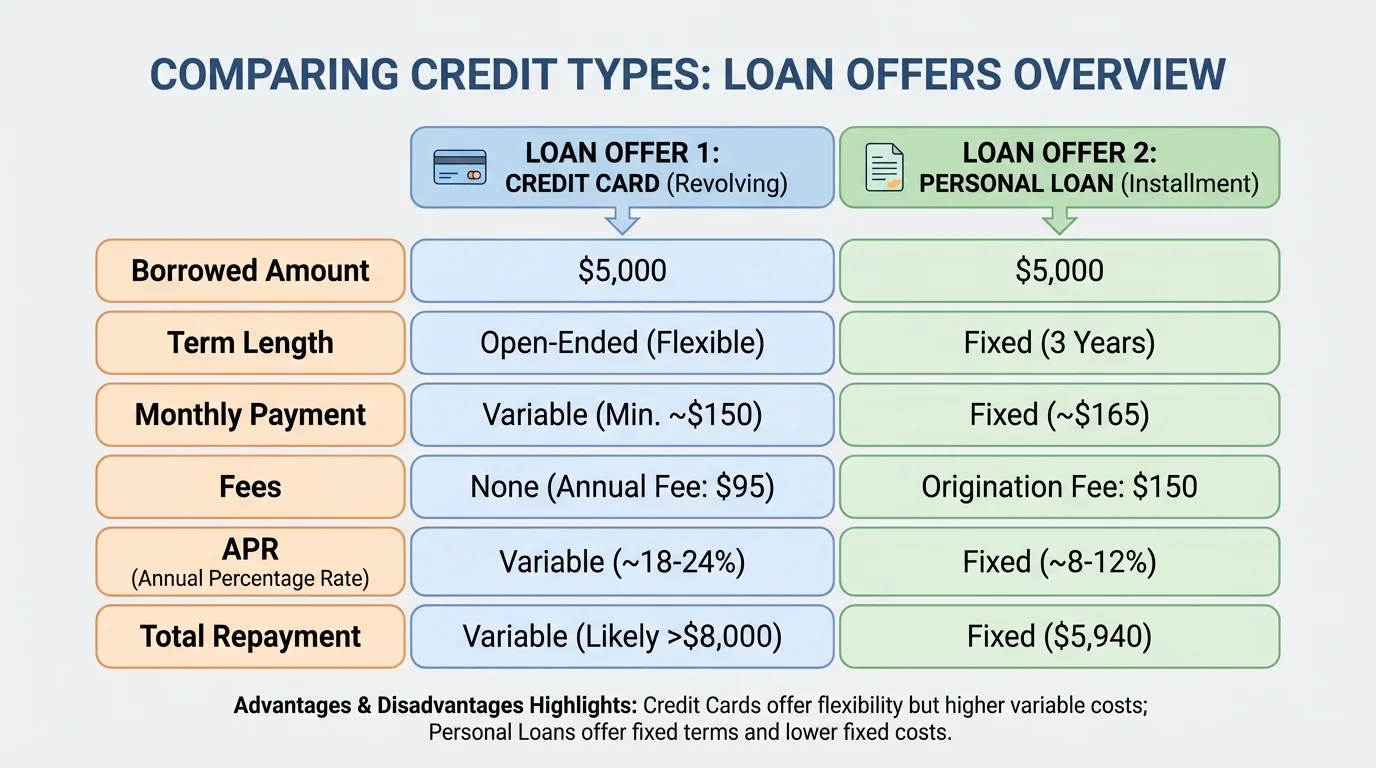

When comparing loans, the smallest monthly payment is not always the best choice, as [Figure 3] emphasizes. Borrowers should compare at least five things: the APR, the total amount borrowed, the repayment term, the fees, and the total repaid by the end.

A simple way to evaluate a loan is to ask: How much will I pay each month, and how much will I pay altogether? If two loans provide the same amount of money, the one with the lower total repayment is usually cheaper, even if the monthly payment is a little higher.

Worked example: comparing two loan offers

A borrower needs $1,200 for a car repair.

Step 1: Compare Loan A.

Loan A requires 12 monthly payments of $110. The total repaid is \(12 \times 110 = 1,320\). The borrowing cost is \(1,320 - 1,200 = 120\).

Step 2: Compare Loan B.

Loan B requires 18 monthly payments of $80 and a $40 fee. The payment total is \(18 \times 80 = 1,440\). Adding the fee gives \(1,440 + 40 = 1,480\). The borrowing cost is \(1,480 - 1,200 = 280\).

Step 3: Evaluate the trade-off.

Loan B has the lower monthly payment, but Loan A costs much less overall. The difference in total cost is \(280 - 120 = 160\).

Lower monthly payments can be attractive, but total repayment reveals the full cost.

APR is especially useful because it gives a yearly percentage cost that helps make offers easier to compare. Still, APR does not tell the whole story by itself. A borrower should also read for fees, penalties, and whether the rate can change over time.

Another important comparison is whether the debt is secured or unsecured. A secured loan may have a lower rate, but the borrower could lose the collateral. An unsecured loan may protect assets but often costs more. The right choice depends on both affordability and risk tolerance.

Worked example: estimating simple interest for comparison

A lender offers a one-year loan of $800 at 10% simple annual interest.

Step 1: Use the simple interest formula.

\(I = Prt\)

Step 2: Substitute the values.

Here, \(P = 800\), \(r = 0.10\), and \(t = 1\), so \(I = 800 \times 0.10 \times 1 = 80\).

Step 3: Find the total repayment.

The total is \(800 + 80 = 880\).

This estimate helps a borrower compare whether another loan offer would cost more or less.

Later, when weighing a fixed loan against a revolving balance, the side-by-side thinking shown in [Figure 3] remains useful: compare not just access to money, but cost, time, and risk.

A credit report is a record of a person's borrowing and repayment history. A credit score is a number that summarizes risk based on information from that report. Paying on time, keeping debt manageable, and avoiding default generally help a borrower build stronger credit.

The type of credit matters less than the behavior attached to it. A credit card can help build credit when balances stay low and payments are on time. A student loan can support future goals if payments are managed responsibly. A personal loan can simplify finances if it replaces more expensive debt. But any form of credit can become harmful when payments are missed or borrowing exceeds income.

Budgeting still comes first. Before taking on a payment, subtract expected monthly expenses from monthly income and savings goals. If the payment does not fit comfortably, the credit may not be affordable even if approval is easy.

Responsible borrowing also means protecting against emergencies. A person with no emergency savings may be forced into expensive borrowing when unexpected costs appear. Saving regularly can reduce the need to rely on high-cost credit at all.

The best type of credit depends on the purpose. For a purchase that can be paid off immediately, a credit card may offer convenience and protections. For a fixed one-time expense, an installment loan may offer clearer repayment. For a long-term investment like a home, a mortgage may be appropriate. For very high-cost short-term borrowing, the disadvantages usually outweigh the advantages.

Borrowers should ask several practical questions before signing any credit agreement. Is this purchase necessary now? Could saving first avoid borrowing? Can the monthly payment fit alongside rent, food, transportation, and savings? What is the total amount that will be repaid? What happens if a payment is late? Is collateral at risk?

Good financial decisions rarely come from looking at only one number. A loan with a low payment, a card with a reward program, or a fast approval process may seem attractive at first glance. But smart comparison means looking at the complete picture: flexibility, total cost, repayment time, impact on future credit, and risk to the borrower's budget.