One of the fastest ways to feel like an adult is not turning a certain age. It is opening your phone, seeing three bills due this week, realizing your paycheck already has a job, and understanding that no one else is automatically fixing it for you. Financial planning is what turns that stressful feeling into control. When you know where your money is going before it leaves your account, adult responsibilities become manageable instead of overwhelming.

Financial planning is not about being rich, and it is not about never spending money on things you enjoy. It is about making sure your choices match your real life. If you earn $800 this month and commit to $950 in expenses, the problem is not motivation. The problem is the plan. A strong plan helps you cover needs, protect yourself from surprises, and still leave room for goals and enjoyment.

As you move toward independent living, money decisions affect almost everything: where you live, how you get to work, whether you can handle an emergency, and how much stress follows you day to day. Good planning gives you options. Poor planning often leads to overdraft fees, late charges, damaged credit, conflict with roommates or family, and constant anxiety.

Financial planning means organizing your income, expenses, savings, and goals so you can meet current needs and prepare for future responsibilities. Independent living means managing the costs and tasks of everyday life yourself, such as housing, food, transportation, utilities, and personal bills.

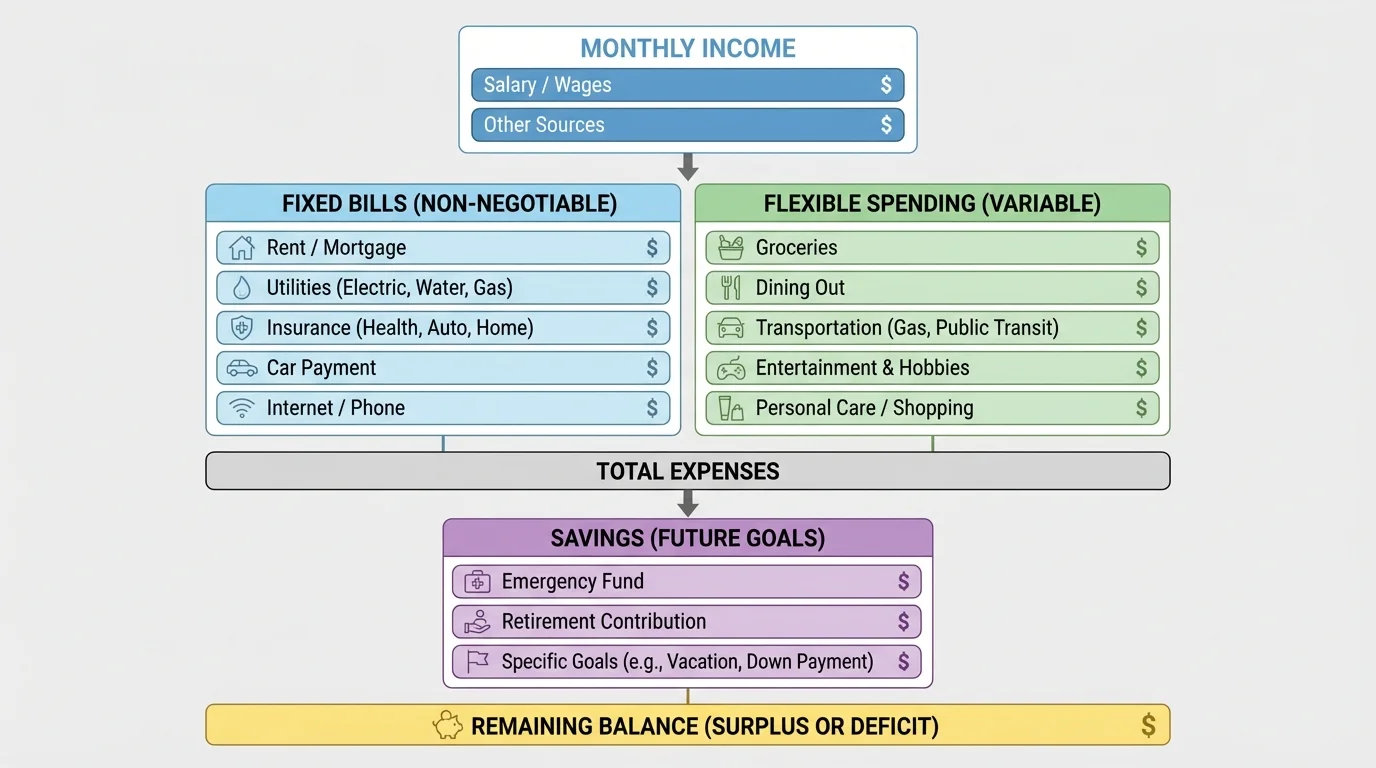

The first step is understanding your monthly money picture. That means knowing how much money comes in, how much must go out, and what is left after essentials. In personal finance, people often talk about cash flow, which is simply the movement of money in and out of your life. Positive cash flow means more comes in than goes out. Negative cash flow means you are running short.

A useful way to organize your money is to separate expenses into three groups, as [Figure 1] shows: fixed expenses, variable expenses, and savings. Fixed expenses stay mostly the same each month, like rent, a phone bill, or car insurance. Variable expenses change, like groceries, gas, and entertainment. Savings should be treated as a planned category, not as whatever happens to be left over.

Here is a simple monthly check: income minus total expenses equals what remains. If your take-home pay is $1,200, rent is $500, your phone bill is $60, transportation is $140, groceries are $220, and savings is $100, then your remaining money is calculated as \(1200 - (500 + 60 + 140 + 220 + 100) = 180\). That $180 has to cover everything else, including personal items, streaming services, or unexpected spending.

Many money problems happen because people guess instead of measure. You do not need a complicated spreadsheet to start, but you do need honest numbers. Look at your job income, side gigs, support from family if that applies, and any regular expenses already coming out of your account.

Start by writing your monthly income. If your pay changes from week to week, estimate carefully using a lower, realistic amount instead of your highest possible month. For example, if you usually earn between $250 and $320 per week, planning around $260 per week gives you a safer monthly estimate of \(260 \times 4 = 1040\). Planning with your best-case income can leave you short when hours drop.

Next, list your nonnegotiable expenses. These are costs that protect your stability: rent, insurance, minimum debt payments, transportation to work, groceries, medication, and utilities. After that, list flexible expenses such as eating out, gaming purchases, clothes, or subscriptions. This separation helps you see what can be adjusted when money gets tight.

Starter monthly budget example

You are working part-time and preparing to pay more of your own expenses.

Step 1: Add monthly income.

Job income is $980 and freelance work is $120, so total income is \(980 + 120 = 1100\).

Step 2: Add fixed expenses.

Phone is $55, insurance is $90, and a contribution to household rent is $250. Total fixed expenses are \(55 + 90 + 250 = 395\).

Step 3: Estimate variable essentials.

Gas is $100 and groceries are $180, so essentials add \(100 + 180 = 280\).

Step 4: Pay yourself first.

Set aside $100 for savings.

Step 5: Find remaining money.

The amount left is \(1100 - (395 + 280 + 100) = 325\).

That $325 covers personal spending, occasional fun, and any extra goals. If you spend more than that, your budget stops working.

A budget is not punishment. It is permission with limits. It tells you what you can spend without creating a problem later. If you know you have $80 for entertainment this month, spending $25 on a movie night is fine. Spending $80 in one weekend and then panicking about gas money is what budgeting helps prevent.

A good beginner budget has a few key features: it is simple, based on your real numbers, and reviewed often. If your system is too complicated, you will avoid it. Start with one monthly plan and one weekly check-in.

Use this step-by-step method. Step 1: Estimate income conservatively. Step 2: Cover essential bills first. Step 3: Set a savings amount. Step 4: Assign limits to flexible spending. Step 5: Review every week and adjust before a problem grows.

Many people find it helpful to use percentages as a reality check, not as a perfect rule. If housing takes half your income, your budget may feel tight no matter how carefully you plan. If food spending is much higher than expected, meal planning might matter more than cutting tiny expenses elsewhere. Percentages help you notice imbalance. For example, if rent is $600 and income is $1,200, then housing is \(\dfrac{600}{1200} = 0.5\), or \(50\%\) of income.

Small recurring charges often do more damage than one big purchase because they feel invisible. A $12 subscription, a $9 app charge, and a $15 membership add up to $36 a month, which becomes \(36 \times 12 = 432\) over a year.

That is why tracking subscriptions matters. Before agreeing to any monthly service, ask yourself three questions: How often will I actually use this? Can I cancel easily? What bill will this compete with if my income drops? If you cannot answer clearly, pause before signing up.

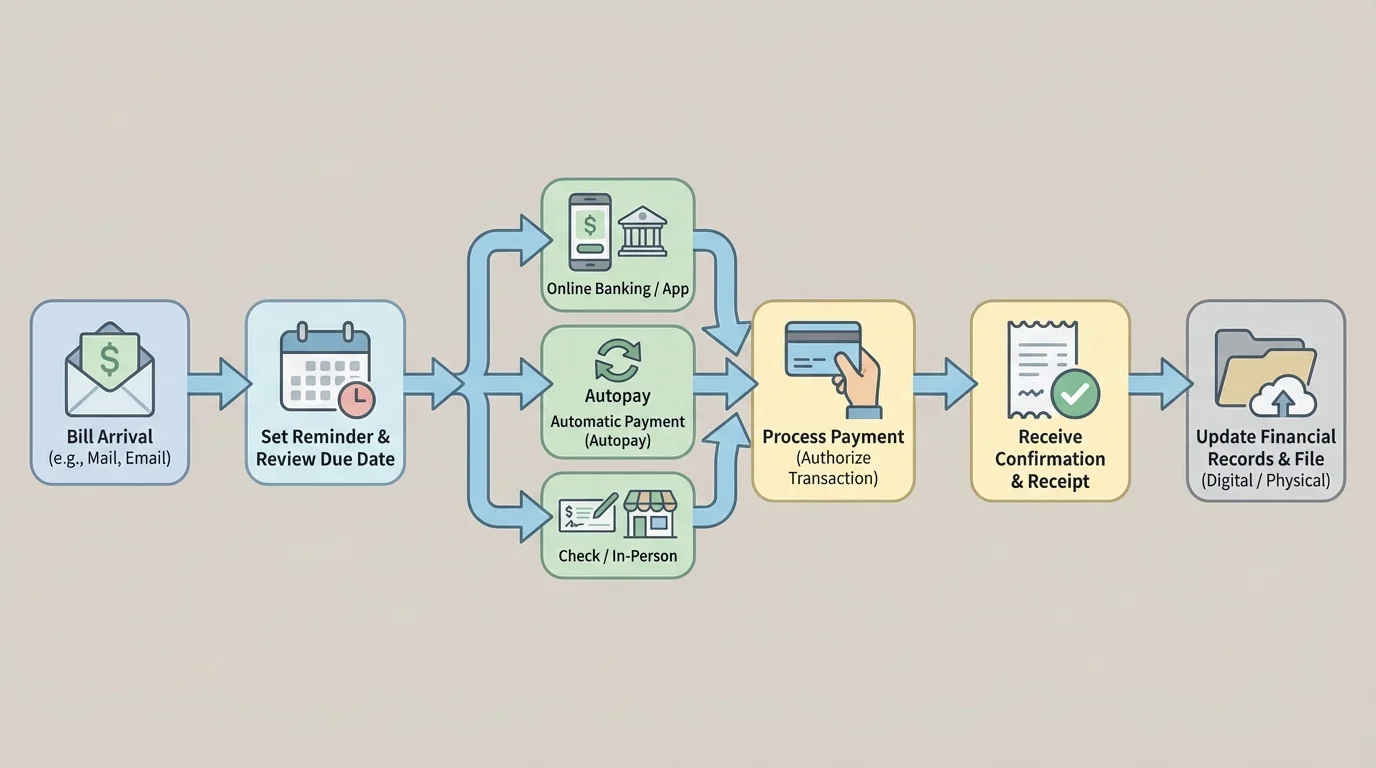

Bills become easier when you build a repeatable system, as [Figure 2] illustrates. Adult life includes due dates, confirmation emails, account passwords, and service providers who still expect payment even if you forgot. Your goal is to make remembering less important than having a system.

Use one bill list with five pieces of information for each expense: the company name, amount, due date, payment method, and whether it is automatic or manual. This can live in a notes app, spreadsheet, or budgeting app. What matters is that it is updated and easy to check.

Your basic bill routine should look like this: when a bill appears, confirm the amount, check the due date, make sure enough money is in the account, schedule or send the payment, and save proof that it was paid. Late payments can trigger fees, service interruption, and credit damage. A missed phone bill might mean your service gets cut off. A missed insurance payment can create much bigger problems if you need coverage.

Autopay can help, but only when you monitor it. Autopay does not mean ignore it. If the amount changes, if fraud appears, or if your balance is too low, autopay can still cause overdraft problems. A safer method for many beginners is to automate stable bills and manually review changing bills like utilities or credit card balances.

Create reminders before due dates, not on due dates. A reminder three to five days early gives you time to move money or fix an issue. If rent is due on the first, a reminder on the twenty-sixth or twenty-seventh of the previous month is more useful than a reminder on the morning it is already due.

Late fees are not just annoying; they reshape your budget. If you miss a $70 bill and get a $15 late fee, your cost becomes \(70 + 15 = 85\). If that causes your bank account to overdraft and adds another $35 fee, the original $70 obligation can suddenly cost $120. A weak system turns ordinary bills into expensive problems.

If you cannot pay a bill, communicate early. Many companies offer extensions, payment plans, or temporary assistance, but these options are more likely when you contact them before the account becomes seriously overdue. Professional communication matters: be direct, respectful, and specific about what you can pay and when.

A bank account is not just a place where money sits. It is part of your daily financial system. Most young adults need a checking account for spending and bill payments and a savings account for goals and protection. Your checking account handles transactions. Your savings account protects money from casual spending.

Watch your overdraft risk. Overdraft happens when you spend more money than is available in your account. Some banks decline the transaction. Others allow it and charge a fee. Either way, it is a sign your tracking system needs improvement. Checking your account balance every few days is a simple habit that prevents a lot of damage.

Direct deposit can help you stay organized because your money arrives faster and more predictably. Many people also use a simple split: bill money stays in checking, while emergency or goal money is moved to savings right away. Separating money by purpose makes it harder to spend accidentally.

Use your debit card carefully. A debit card feels easy, but it pulls real money directly from your account. If you tap repeatedly without checking your balance, you can lose track fast. Keep receipts digitally or review transactions in your banking app at least once a week.

Independent living costs are often higher than people expect because they include both obvious and hidden expenses. Rent is not the full story. You may also need a security deposit, application fees, renter's insurance, internet, electricity, water, household supplies, and furniture. Transportation may include gas, maintenance, parking, insurance, public transit, or ride-share costs.

If you are comparing living options, estimate the total monthly cost, not just the advertised rent. Apartment A may cost $700 in rent with $140 in utilities and $60 in internet, for a total of \(700 + 140 + 60 = 900\). Apartment B may cost $820 with utilities included. The second option may actually be cheaper and more predictable.

Food is another area where planning matters. Buying random convenience food every day usually costs more than shopping intentionally. If lunch costs $11 five days a week, that becomes \(11 \times 5 = 55\) per week, or about \(55 \times 4 = 220\) per month. Packing some meals or planning simple groceries can lower that total significantly without making life miserable.

| Category | Examples | Questions to Ask |

|---|---|---|

| Housing | Rent, deposit, insurance, internet | What is included? How stable is the monthly total? |

| Utilities | Electricity, water, trash | Do costs rise by season? Who pays which bill? |

| Transportation | Gas, transit pass, insurance, repairs | What do I need every month to get to work reliably? |

| Food | Groceries, occasional meals out | What plan is realistic for my schedule? |

| Household | Cleaning supplies, toilet paper, laundry | What small costs am I forgetting? |

Table 1. Core independent-living expense categories and the planning questions that help estimate them realistically.

If you live with roommates, money management includes communication. Decide who pays which bill, how shared costs are split, how reimbursements happen, and what the deadline is. Vague agreements create conflict. Clear agreements protect relationships.

Comparing transportation choices

You are deciding between driving and public transit for work.

Step 1: Estimate driving costs.

Gas is $120, insurance is $95, parking is $40, and average maintenance savings is $35, so monthly driving cost is \(120 + 95 + 40 + 35 = 290\).

Step 2: Estimate transit costs.

A monthly pass is $90 and occasional ride-share costs are $35, so total transit cost is \(90 + 35 = 125\).

Step 3: Compare.

The difference is \(290 - 125 = 165\).

If transit is realistic for your schedule, it saves $165 per month. But time, safety, and reliability still matter, so the cheapest choice is not always the best choice.

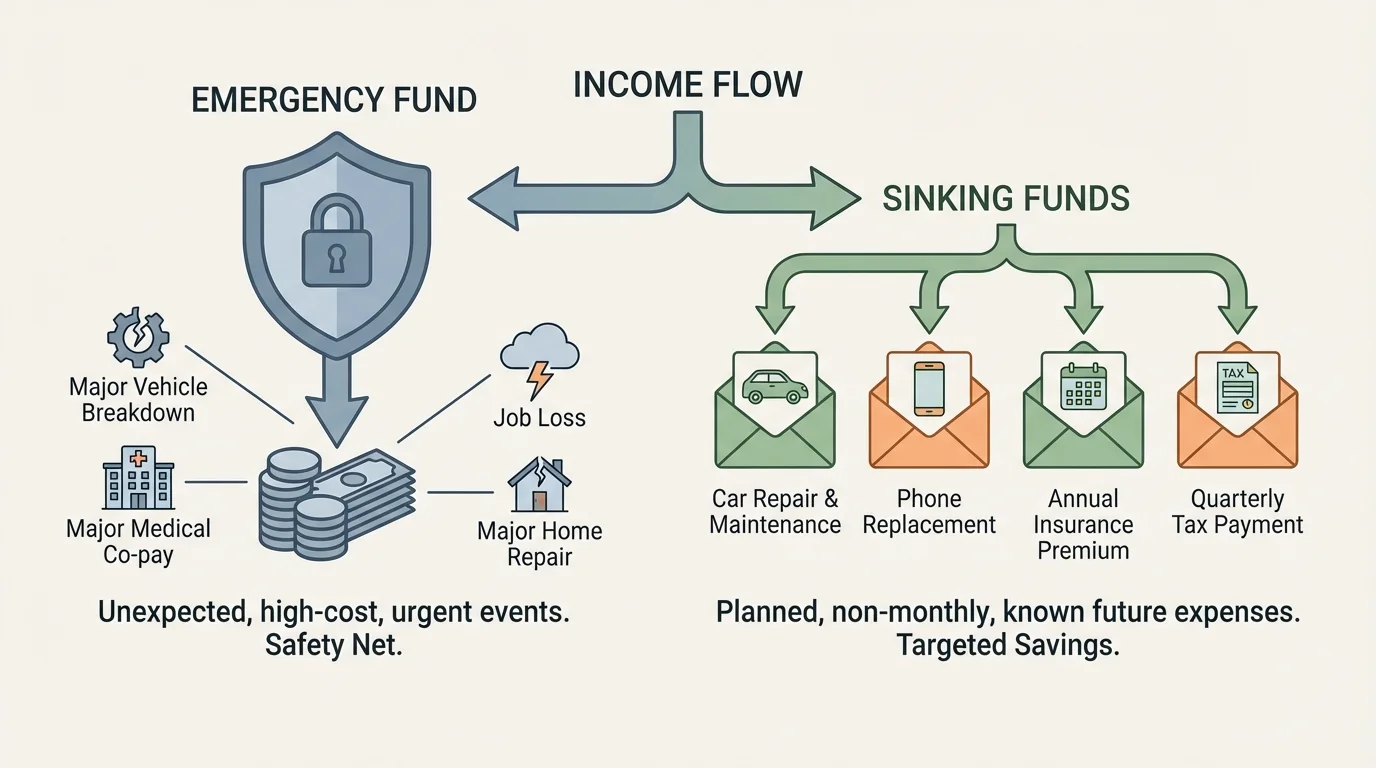

Financial stability is not only about the bills you expect. It is also about what happens when life interrupts your plan. A dead car battery, a cracked phone screen, a medical copay, reduced work hours, or an urgent trip can wreck a budget that has no backup. That is why emergency fund planning matters, as [Figure 3] shows alongside other targeted savings.

You need two kinds of protection. An emergency fund covers true surprises or urgent losses. A sinking fund covers predictable but irregular costs. Car maintenance is not a surprise in the long run. Neither are holiday gifts, school supplies for a certification program, or replacing worn-out shoes. They may not happen every month, but they are still real costs.

If you know a car service usually costs about $300 every six months, you can save for it gradually. Saving \(\dfrac{300}{6} = 50\) means putting aside $50 each month. That is much easier than trying to find $300 at once when the bill arrives.

A good beginner goal is to start small but consistently. Even $25 or $50 at a time builds protection. If you save $40 per paycheck and get paid twice a month, that becomes \(40 \times 2 = 80\) monthly, or \(80 \times 6 = 480\) in six months. That amount can cover many common emergencies and keep a bad week from becoming a financial crisis.

Later, as your income grows, your emergency fund should grow too. The point is not perfection on day one. The point is reducing how often unexpected expenses force you into debt, panic, or missed bills. As you saw with [Figure 3], separating true emergencies from expected irregular expenses helps you save with purpose instead of just hoping extra money appears.

You already know that planning ahead makes big tasks easier. Money works the same way. Breaking a large cost into smaller monthly amounts makes it far more manageable than waiting until the deadline arrives.

At some point, you may use a credit card, finance a car, or need your financial history checked for housing. That is where your credit score matters. A credit score is a number that helps lenders and sometimes landlords estimate how reliably you handle borrowed money.

Credit can be useful, but only if you treat it as a tool, not extra income. If you charge $300 but only make the minimum payment, interest can make that purchase cost more over time. The exact amount depends on the interest rate and time, but the main lesson is simple: borrowing makes future money responsible for today's choices.

The safest beginner rule is this: do not put something on a credit card unless you already have a plan to pay it off. Using a card for one small recurring expense and paying the full balance on time each month is very different from using it to buy things you cannot actually afford.

Protecting your future also means protecting your identity. Use strong passwords, enable account alerts, avoid sharing financial information casually online, and review statements for unfamiliar charges. Fraud is not only something that happens to other people.

"Do not save what is left after spending; spend what is left after saving."

— Common personal finance principle

This idea works because it flips your priorities. If saving depends on leftovers, there often are no leftovers. If saving happens early, your spending naturally adjusts to the amount that remains.

Being financially responsible also means being a smart buyer. Advertising is designed to make spending feel urgent, harmless, or emotionally rewarding. Your job is to slow the decision down long enough to think clearly.

Read contracts before you agree to them. This includes phone plans, gym memberships, leases, buy-now-pay-later offers, and app subscriptions. Look for cancellation rules, fees, automatic renewal, penalties, and what happens if you miss a payment. A low monthly price can hide a long commitment or expensive consequences.

Comparison shopping saves money because it replaces impulse with evidence. Before making a larger purchase, compare total cost, quality, return policy, and reliability. A cheaper item is not always the better value if it breaks quickly and must be replaced. What matters is the cost over time, not just the cost today.

Avoiding a common buying mistake

You want headphones. Option A costs $25 but usually lasts about three months. Option B costs $70 and lasts at least a year.

Step 1: Estimate annual cost of Option A.

If you replace Option A four times, the yearly cost is \(25 \times 4 = 100\).

Step 2: Estimate annual cost of Option B.

One purchase costs $70 for the year.

Step 3: Compare value.

Option B saves \(100 - 70 = 30\) over the year and may work better too.

The lower upfront price is not always the smarter financial choice.

Scams also target people who are new to adult responsibilities. Be cautious if someone pressures you to act immediately, asks for payment by gift card or wire transfer, offers guaranteed easy money, or requests personal information through suspicious messages. When something feels rushed and secretive, step back and verify it through official sources.

Money management works best when it becomes routine instead of emotional emergency mode. A practical system might take only a few minutes at a time. The key is consistency.

Try this. Once a week, open your banking app and spending tracker. Check your balance, review recent charges, confirm upcoming bills, and compare your remaining spending money with the rest of the month. Once a month, update your budget using real numbers instead of guesses.

You can also use a short checklist: income received, bills covered, savings moved, subscriptions reviewed, and next week checked. This kind of system lowers stress because you are not constantly wondering whether you forgot something important.

Many people avoid checking their accounts when they feel stressed about money, but that usually makes the problem worse. Looking early gives you more choices, while looking late usually leaves fewer.

One more practical habit: keep a small buffer in checking if possible. Even an extra $50 to $100 can prevent tiny timing issues from causing overdrafts. If your paycheck lands a day later than expected or a subscription renews earlier than you remembered, that buffer can protect you.

Financial planning is also a mindset. It means accepting that small decisions repeat into bigger results. Paying attention is part of adulthood. So is asking questions before signing something, speaking up early when you cannot make a payment, and learning from mistakes without giving up.

You do not need to manage money perfectly to manage it well. What matters most is honesty, planning, and follow-through. If you overspend one month, the goal is not shame. The goal is to figure out why, adjust your system, and make a better choice next time.

Adult responsibilities become less intimidating when you build skills one habit at a time: track income, plan spending, save before emergencies happen, protect your accounts, and think carefully before committing to payments. Those habits create stability, and stability creates freedom.