What would happen if every dollar you received had to stay in a jar at home forever? It might sound simple, but it would make saving, tracking, and protecting your money much harder. Banking tools are helpful because they give you safe places to keep money, easy ways to use it, and clear records that show what is happening. When you learn how these tools work, you are not just learning about money—you are building skills that help you make smart choices in real life.

Even at age 11, banking tools already matter. You might get birthday money, earn money by helping with chores, sell homemade crafts online with an adult, or save up for something important like sports gear, art supplies, or a new game. Knowing where to keep that money, how to protect it, and how to avoid spending it too fast is part of financial responsibility. That means taking care of your money in a thoughtful, honest, and organized way.

A bank or credit union is a place that helps people store, move, and manage money. Instead of carrying lots of cash or hiding it at home, people can put money into accounts. Then they can check balances, pay for things, transfer money, and keep records of what they earned and spent. This makes money easier to manage and usually much safer.

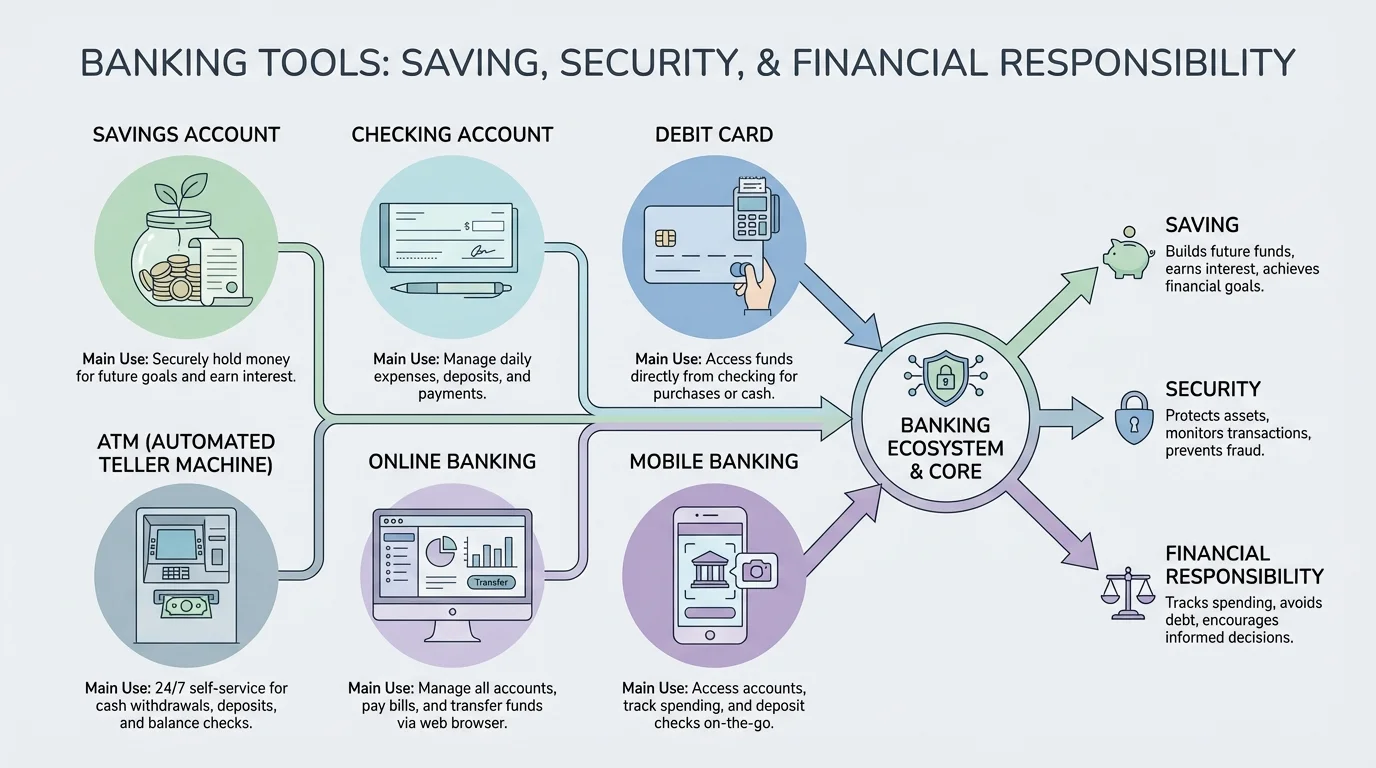

Banking tools are the accounts, cards, apps, and services people use to manage money. Common examples include savings accounts, checking accounts, debit cards, ATMs, direct deposit, and online or mobile banking.

These tools support three big goals. First, they help you save by keeping money separate and easy to track. Second, they help with security by protecting money from loss, theft, or scams. Third, they support responsibility because they create records and make you pay attention to what you have, what you spend, and what you still need for future goals.

Different tools do different jobs, and [Figure 1] shows how they fit together in everyday money management. Learning the basics now helps you understand what adults use and prepares you to manage your own money more confidently later.

A savings account is mainly for money you want to keep for later. A checking account is usually for money that moves in and out more often, such as paying for things. A debit card lets you spend money from a checking account without using cash. An ATM lets you take out cash or do some account tasks. Online banking and mobile banking let you check your account on a computer or phone. Direct deposit is when money goes straight into an account instead of being handed to you in cash or paper check.

Some students have joint accounts with a parent or guardian. That means an adult is also connected to the account and helps manage it. This can be a smart way to practice using banking tools while still having support.

Think of these tools as parts of a system. Your savings account is like your "hold for later" space. Your checking account is your "money in motion" space. Your debit card is the spending tool. Your banking app is the dashboard where you check what is happening. When you understand the job of each tool, it becomes easier to make smart choices.

Many people spend more carefully when they check their account often. Seeing the real balance can make money feel more real than just guessing.

That matters because guessing can lead to mistakes. If you think you have enough money but never check, you might try to buy something you cannot afford. If you use your tools carefully, you stay in control.

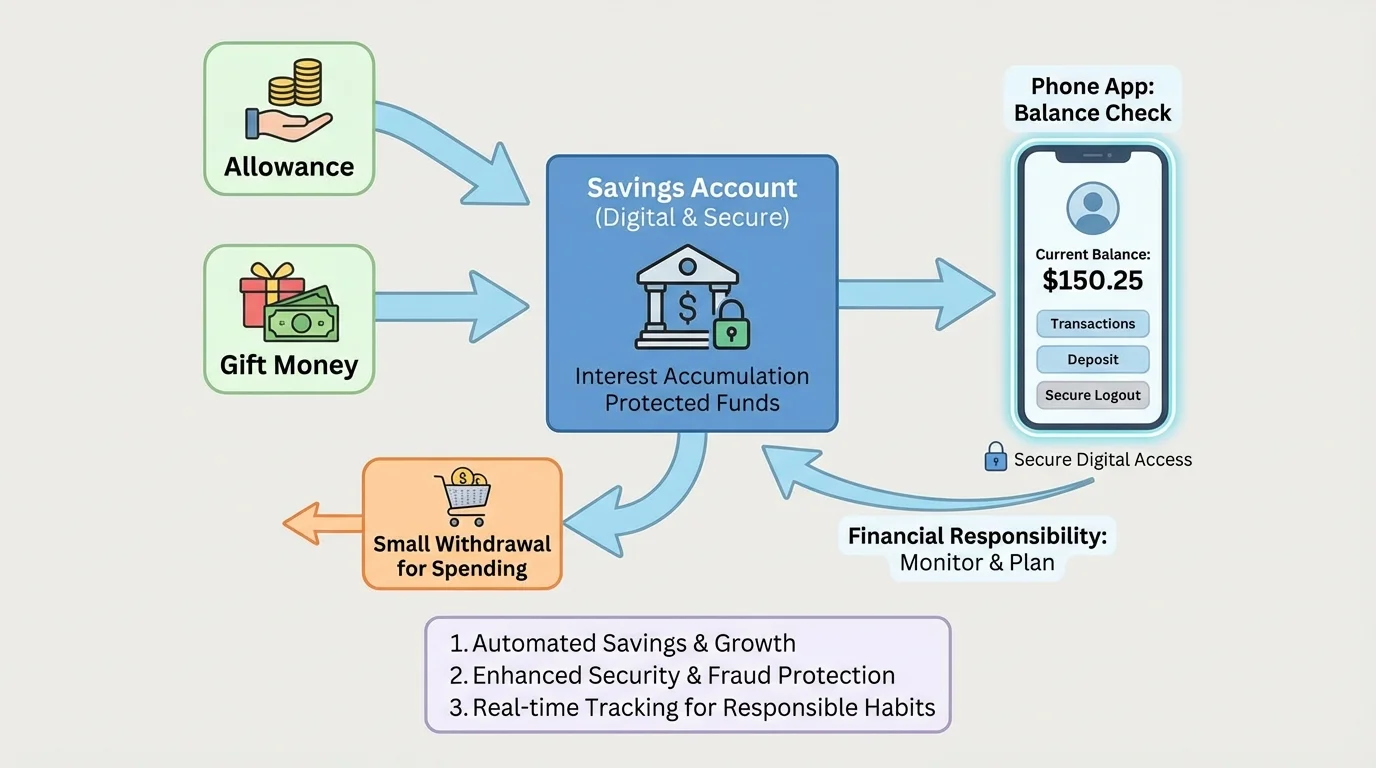

Saving is easier when your money has a clear place to go, and [Figure 2] illustrates how money can move into savings and stay there for a goal. If all your money stays mixed together in cash, it is easier to lose track of it or spend it without thinking.

A savings account helps by separating money you want to keep. Let's say you get $20 for your birthday and earn $10 helping a neighbor with yard work. If you decide to save $25 and keep $5 for spending, the account gives you a simple record. You can see that your saved amount is $25, not just a guess in your head.

Banking tools also help you watch your balance, which is the amount of money currently in your account. If you start with $25 and later deposit $15 more, your balance becomes \(25 + 15 = 40\). If you then spend $12, your new balance is \(40 - 12 = 28\). Being able to see those changes clearly helps you stay on track.

Saving tools also support goals. Maybe you want headphones that cost $48. If you already saved $28, you can tell exactly how much more you need: \(48 - 28 = 20\). That makes the goal feel reachable. Without a record, you might forget how close you are and spend your money on smaller things.

Real-world saving example

You are saving for a $36 sketch set.

Step 1: Check what you already have.

Your account balance is $14.

Step 2: Add new money.

You deposit $8 from chores, so \(14 + 8 = 22\).

Step 3: Compare your balance to your goal.

You still need \(36 - 22 = 14\).

Because the account shows each change, you know exactly where you stand.

Another way banking tools help with saving is by slowing you down in a good way. If your savings money is in an account, you are less likely to grab it quickly for an impulse purchase. That pause gives you time to ask, "Do I really want this now, or do I care more about my bigger goal?"

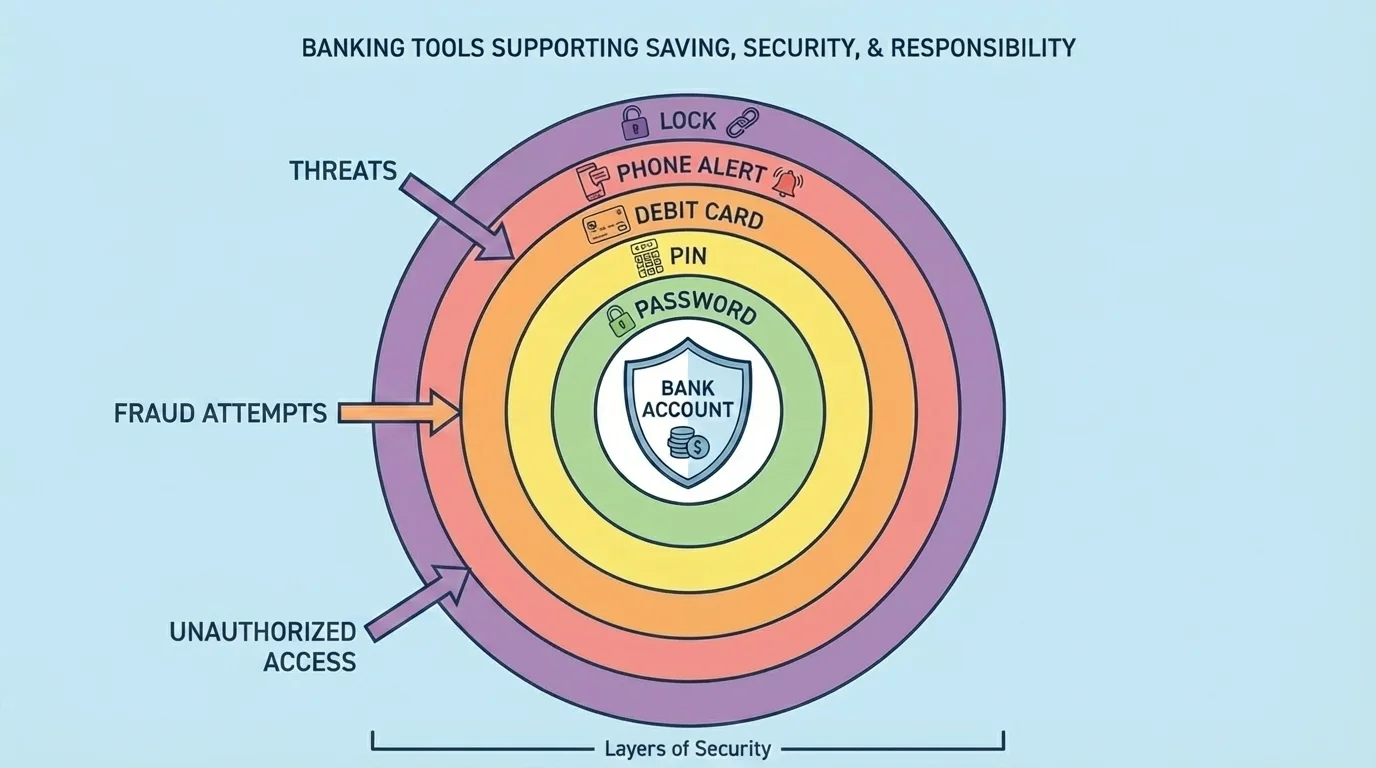

Money safety is not just about where your dollars are stored. It is also about protecting your information, your card, and your account access. Banking security works in layers, and [Figure 3] shows how tools such as passwords, PINs, and alerts work together.

A PIN is a secret number used with some bank cards. A password protects online or mobile banking. Security alerts can send messages if something unusual happens, such as a purchase you did not expect. Banks and credit unions also watch for signs of fraud, which means dishonest attempts to steal money or information.

If you keep cash in your room and it disappears, it may be gone for good. If a debit card is lost, the account can often be protected by reporting it quickly and freezing or replacing the card. That is one reason banking tools can be safer than carrying all your money in cash.

You also have an important job in keeping money safe. Never share your password or PIN with friends. Do not type banking information on random websites. If a message says, "Click now or your account will close," stop and check with a trusted adult. Scammers often try to create panic so people act too fast.

How smart security habits protect you

Banking security is strongest when the bank's tools and your choices work together. The bank can monitor accounts and send alerts, but you still need to use strong passwords, keep cards in a safe place, and report problems right away.

Many accounts in the United States are also protected by a kind of insurance through the government if the bank or credit union itself has a serious problem. You do not need to memorize the program names yet, but it is helpful to know that regulated financial institutions usually have protections that a cash jar at home does not.

Later, when you use apps or websites more often, the same idea still matters: good security is not one single lock. It is a group of habits and protections working together.

Being responsible with money means more than "not wasting it." It means checking your financial information before spending, keeping track of what happened, and making choices that match your goals. Banking tools help because they create records. When you look at your account history, you can see deposits, withdrawals, purchases, and transfers.

That record helps you notice patterns. Maybe you keep spending small amounts on game add-ons or snacks from a community event, and by the end of the month you are surprised at how much is gone. A banking app or statement helps you see the truth. Then you can make a better plan.

Responsibility also means not spending more than you have. Some accounts charge fees if people try to spend past their balance. Even if your account type is designed to prevent that, it is still important to check first. Spending without checking can lead to embarrassment, stress, or extra costs.

| Tool | How it helps | Responsible habit |

|---|---|---|

| Savings account | Keeps goal money separate | Deposit part of new money before spending |

| Checking account | Handles everyday money movement | Check the balance before using it |

| Debit card | Makes purchases without cash | Use only when you know the account has enough money |

| Banking app | Shows balances and activity | Review transactions often |

| Alerts | Warns about unusual activity | Tell a trusted adult right away if something looks wrong |

Table 1. Common banking tools, what they do, and the habits that help you use them responsibly.

When you learn to read those records, you become a stronger decision-maker. That skill will help later with bigger responsibilities such as jobs, bills, subscriptions, and long-term saving.

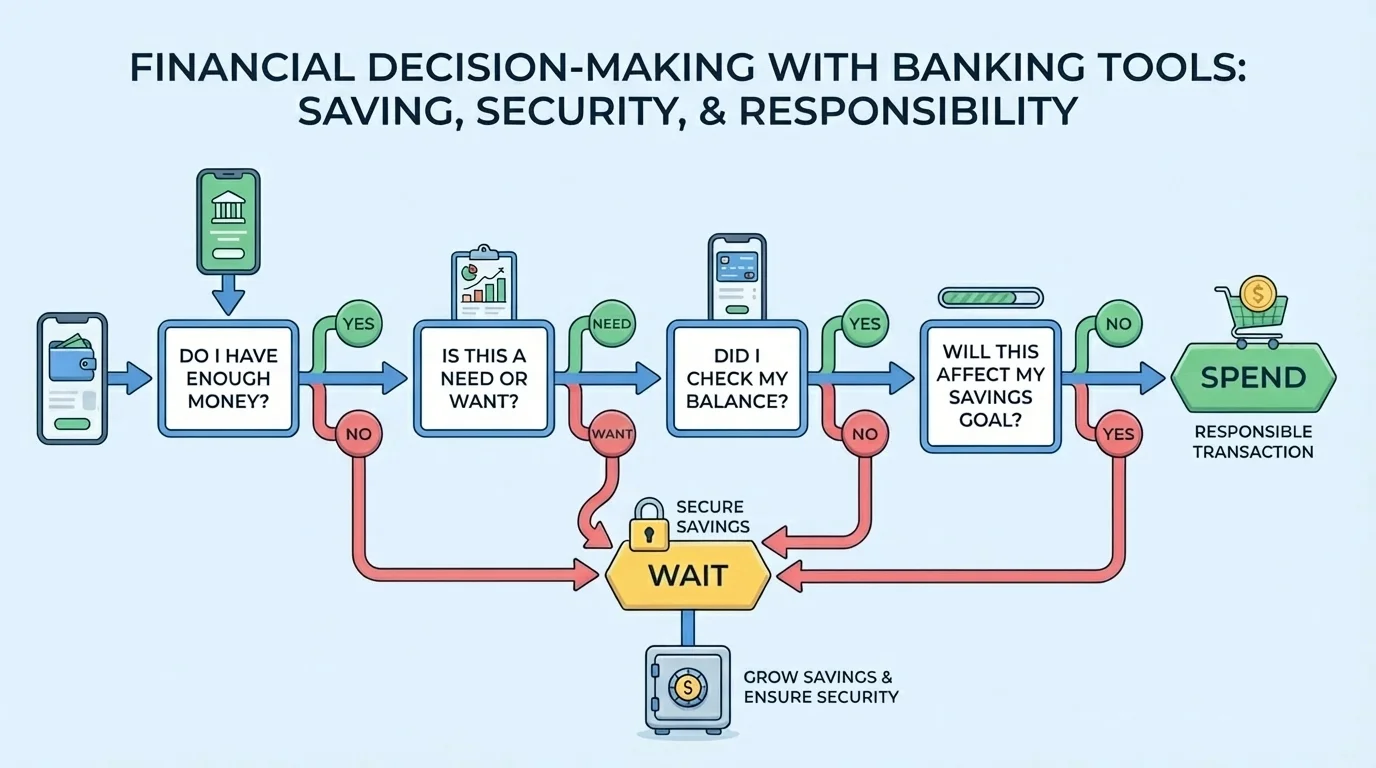

A simple decision routine can prevent many money mistakes, and [Figure 4] shows a quick check you can use before spending or moving money. You do not need a complicated system. You just need a few clear steps that you repeat every time.

Step 1: Check your balance. Do not guess. Look at the actual number in the app, website, or account record.

Step 2: Ask whether the purchase is a need or a want. A need is something important to daily life. A want is something extra you would enjoy but can live without.

Step 3: Think about your savings goal. If you spend this money now, what goal gets delayed?

Step 4: Make sure the payment method matches the job. Savings money is usually for later. Checking money is usually for spending.

Step 5: Review the transaction after it happens so you know your new balance is correct.

This short routine helps you act on purpose instead of on impulse. It is especially useful when you want to buy something online quickly or when a friend is talking about a new trend and you feel pressure to join in.

Before-you-buy example

You want to buy a game add-on for $9.

Step 1: Check your balance.

Your checking balance is $18.

Step 2: Remember your goal.

You planned to move $10 into savings for a sports item.

Step 3: Compare your choices.

If you spend $9 now, you would have \(18 - 9 = 9\) left, which is not enough to move $10 into savings.

Step 4: Make the decision.

You may decide to wait so your goal stays on track.

That is financial responsibility in action.

As you get older, the same routine can help with bigger decisions too. The questions stay useful even when the amounts become larger.

Suppose you get $30 for your birthday, and you want to split it wisely. You might put $20 into savings and keep $10 available for spending. That choice protects most of the money from disappearing too fast. If you later earn another $12 and deposit it, your savings total becomes \(20 + 12 = 32\).

Now suppose you sell handmade bracelets with an adult's help and receive payments through a bank-connected app. Banking tools help keep a record of what came in and what went out. If you earned $24 and spent $6 on supplies, you can see that you kept \(24 - 6 = 18\). Records make it easier to tell whether your project is actually helping you save.

Or picture this: you use a debit card to buy a snack and forget about it. Later, you want to buy a book online. If you never checked your account, you might assume you still have enough. But the banking app shows the real balance. That quick check prevents a mistake.

Cash is simple to understand, but it does not automatically keep records for you. Banking tools add organization and protection, which is why they are so helpful for real-life money management.

One more situation: if your card is missing, tell a trusted adult immediately. Fast action can protect the account. Waiting too long can make the problem worse. Responsible banking is not only about what you buy. It is also about how quickly you respond when something seems wrong.

One common mistake is treating your balance like it is "about" a certain amount instead of checking the exact number. Another is using a debit card because it feels like "not real money." But a debit card uses real money from an account. Every purchase changes the balance.

A second mistake is sharing private information. Even if someone seems trustworthy online, your banking details should stay private unless a trusted adult is helping you. Passwords and PINs are not for friends, teammates, or online contacts.

A third mistake is forgetting small purchases. Three separate $4 purchases may not feel huge, but together they make \(4 + 4 + 4 = 12\). Small amounts can add up quickly.

"Every money choice is small by itself, but habits turn small choices into big results."

A fourth mistake is not reading alerts or account activity. If something strange appears, speak up quickly. Catching a problem early is easier than fixing it later.

You do not need to wait until adulthood to practice good banking habits. Start small. Check balances before spending. Save part of new money right away. Keep passwords private. Ask questions when something is confusing. Review transactions with a trusted adult if you have a joint account.

Try This: The next time you receive money, decide on a simple split before spending any of it. For example, you might save half and keep half available. If you get $16, saving half means \(16 \div 2 = 8\), so you would save $8 and keep $8 for spending. A rule like this makes decisions easier and builds self-control.

Try This: If you already use a banking app with an adult, look at the transaction list and identify three things: money that came in, money that went out, and the current balance. This helps you read account records like a pro.

Try This: Make a short safety rule for yourself: "I never share my password or PIN, and I ask an adult before clicking account messages." Simple rules are easier to remember and follow.

Banking tools are powerful because they do more than hold money. They help you protect it, organize it, and make thoughtful choices with it. When you use them well, you become more confident and more prepared for real-world money decisions.