A single tap on a phone can enroll a user in a streaming service, transfer money, or approve a purchase that lasts for months through installment payments. That speed is convenient, but it also creates risk. Many financial problems do not begin with huge decisions; they begin with small choices made without reading the details. A missed fee, an automatic renewal, or a fake payment link can turn an ordinary purchase into a contract dispute, debt, or identity theft problem.

Being a smart consumer is not just about finding the lowest price. It means understanding what you agree to, what companies are allowed to do, and what protections the law gives you if something goes wrong. It also means recognizing that consumers have both rights and responsibilities. Rights protect people from unfair treatment. Responsibilities help people lower the risk of lost money, damaged credit, fraud, and legal trouble.

Every day, consumers enter the marketplace by buying goods, using services, opening bank accounts, downloading apps, or borrowing money. A purchase at a store may feel simple, but many transactions create legal and financial obligations. If you order shoes online, you expect accurate advertising and a safe payment system. If you use a debit card, you expect unauthorized charges to be handled fairly. If you sign a membership agreement, you are expected to follow the payment terms.

Consumer protection matters because businesses usually know more than buyers about products, pricing rules, and contract language. That difference in knowledge is called information asymmetry. Laws and regulations help balance that difference by requiring disclosures, limiting deceptive practices, and giving consumers ways to challenge errors.

Consumer means a person who buys or uses goods and services for personal use.

Contract is a legally enforceable agreement between parties.

Financial transaction is an exchange involving money or credit, such as a purchase, bank transfer, loan payment, or card charge.

Consumer protection law is a law designed to prevent unfair, deceptive, or abusive business practices and to give buyers legal rights and remedies.

For teenagers, these issues are already real. Students may have prepaid cards, checking accounts, online subscriptions, in-app purchases, mobile wallets, part-time job income, or car insurance costs. Even before adulthood, decisions about contracts and payments can affect future finances.

A consumer's first responsibility is to read before agreeing. Many people click "I agree" without reviewing the terms, but those terms can include late fees, cancellation rules, arbitration clauses, data-sharing permissions, and automatic renewals. Reading carefully reduces the chance of being surprised later.

Another responsibility is to compare options. A phone plan with a lower monthly fee may have a longer contract, a cancellation penalty, or extra data charges. A loan with a small monthly payment may actually cost more overall because of a higher annual percentage rate, often called APR. Comparing total cost, not just the advertised monthly amount, is a key financial habit.

Consumers are also responsible for protecting their own information. That includes using strong passwords, avoiding suspicious links, checking account statements, and not sharing account numbers casually. In the digital economy, poor security habits can lead to fraud, frozen accounts, and lost time spent repairing the damage.

Other important responsibilities include paying bills on time, keeping receipts and account records, reporting mistakes quickly, and using products as directed. If a consumer ignores billing statements or fails to report an unauthorized charge for a long time, the legal protections may become weaker.

Responsibility as risk management

Consumer responsibility is closely connected to personal financial risk management. Reading a contract can prevent surprise fees. Keeping copies of statements can help prove an error. Reporting fraud quickly can limit losses. In other words, responsible consumer behavior reduces the financial risk of lost income, damaged property, health costs, and identity fraud.

Suppose a student signs up for a "free" trial of a music app and enters a debit card number. If the trial automatically changes into a paid plan after two weeks, the student may feel tricked. But if the terms clearly explained the renewal, the consumer still had the responsibility to read and cancel on time. Consumer rights and consumer responsibilities work together, not against each other.

Consumers have the right to accurate information. Advertisements and disclosures should not be false or misleading. If a lender advertises borrowing costs, federal law requires the company to disclose the APR, fees, and repayment terms clearly enough for comparison.

Consumers also have the right to safety when buying products. A company cannot legally sell dangerous products without meeting safety standards or warning users about serious hazards. For example, if a charger overheats because of a defect, safety rules and recall systems may protect the buyer.

Another important right is the right to privacy and secure handling of personal financial data. Businesses collect names, addresses, account numbers, and purchase histories. Consumers have an interest in how that information is used, stored, and shared. Privacy notices do not eliminate all risk, but they do create expectations and legal duties.

Fair treatment in credit is another major right. A lender cannot lawfully deny credit based on protected characteristics such as race, religion, national origin, sex, marital status, age in many cases, or because someone receives public assistance, if the applicant otherwise qualifies. This protection matters for credit cards, car loans, mortgages, and other forms of borrowing.

Consumers also have rights when errors occur. If a bank transfer is unauthorized, if a credit report contains a mistake, or if a debt collector uses harassment, the consumer may dispute the problem and seek correction. These rights are strongest when the consumer acts quickly and keeps records.

Some of the most powerful consumer protections do not erase a bad situation; they limit how much worse it can get. Quick reporting deadlines, fraud protections, and dispute procedures are designed to reduce damage before a problem grows.

One widely recognized set of ideas is the right to be informed, the right to choose, the right to safety, and the right to be heard. These principles are not always listed in exactly the same way in every law, but they help explain the purpose of consumer protection.

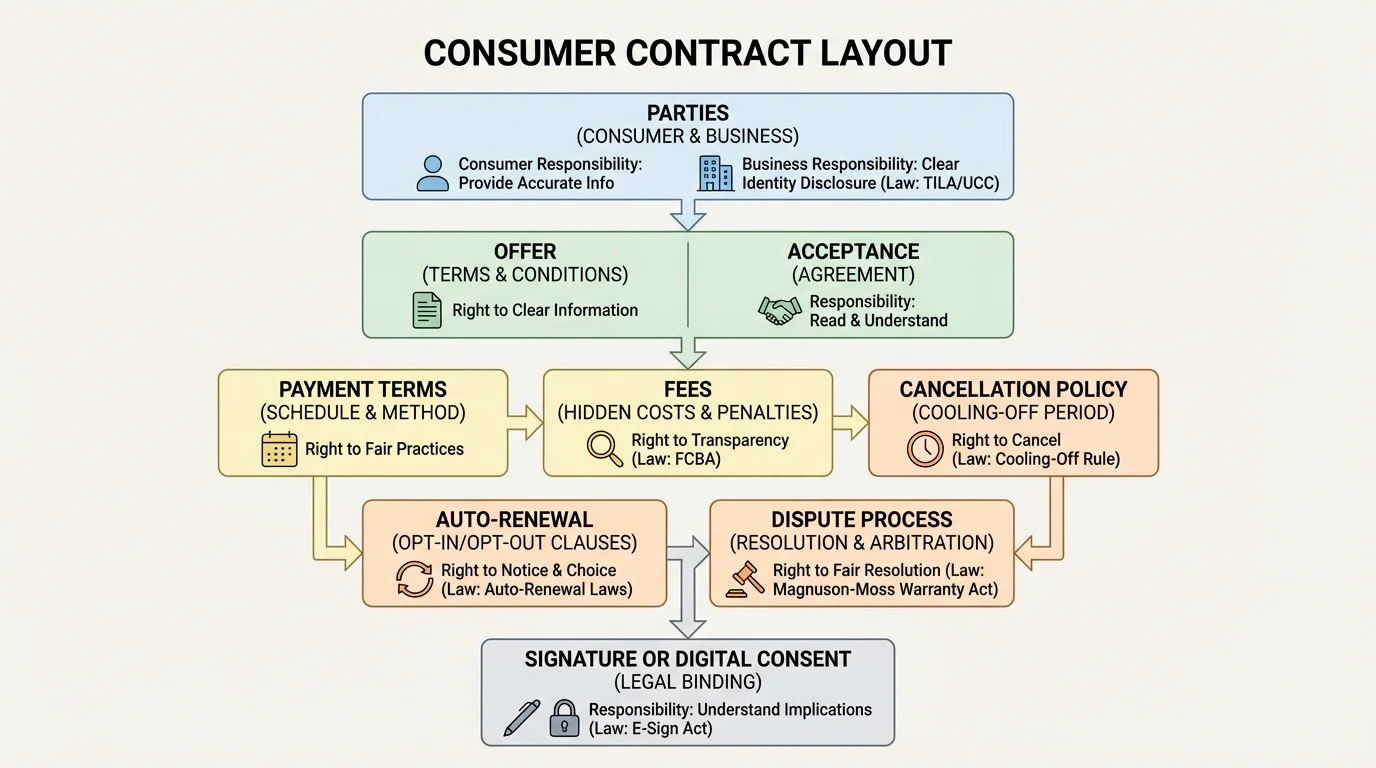

When people hear the word contract, they often picture a long paper covered in legal language. But contracts are everywhere: a gym membership, a car insurance policy, a streaming service subscription, a payment plan for a phone, or an online purchase agreement. Even a basic consumer contract has recognizable parts that help determine each side's duties.

As [Figure 1] shows, a valid contract generally includes an offer, an acceptance, and consideration. Consideration means that each side gives something of value, such as money, goods, services, or a promise. In a phone contract, the company provides service and the consumer promises payment.

Contracts usually include payment terms, due dates, cancellation rules, penalties, warranty language, dispute procedures, and sometimes an arbitration clause. That clause may require disputes to be resolved outside court. Students should know that signing a contract means more than agreeing to a price; it means agreeing to all stated conditions unless the law says a term is unfair or unenforceable.

Another issue is age. Minors, people under the age of majority, often have limited power to enter binding contracts. The exact rules vary by state, and some contracts for necessities such as food, shelter, medical care, or sometimes employment-related matters may be treated differently. This does not mean minors can ignore every agreement, but it does mean contract law recognizes that young people may need extra protection.

Auto-renewal terms deserve special attention. A subscription may continue unless canceled before a deadline. If the consumer misses that date, charges may continue month after month. This is one reason keeping records, screenshots, and confirmation emails is so important.

In many disputes, the question is not "Was there a contract?" but "What did the contract actually say?" The structure shown earlier in [Figure 1] helps explain why checking the cancellation policy, fee section, and dispute language matters before agreeing.

Case study: A gym membership

A student signs up for a gym membership advertised at $25 per month. Later, the student notices charges for an annual maintenance fee and a cancellation fee.

Step 1: Identify the consumer's responsibility.

The student should review the contract for fees, cancellation terms, and notice requirements before signing.

Step 2: Identify the consumer's rights.

If the advertisement was misleading or the fee was never properly disclosed, the student may have grounds to dispute the charge.

Step 3: Identify the best evidence.

Copies of the advertisement, the signed agreement, payment records, and emails with the business support the consumer's position.

This example shows that rights are strongest when consumers have documentation.

Contracts are not automatically unfair just because they are complicated. But they become dangerous when consumers assume that clicking a button is harmless. Legally, digital consent can matter as much as a handwritten signature.

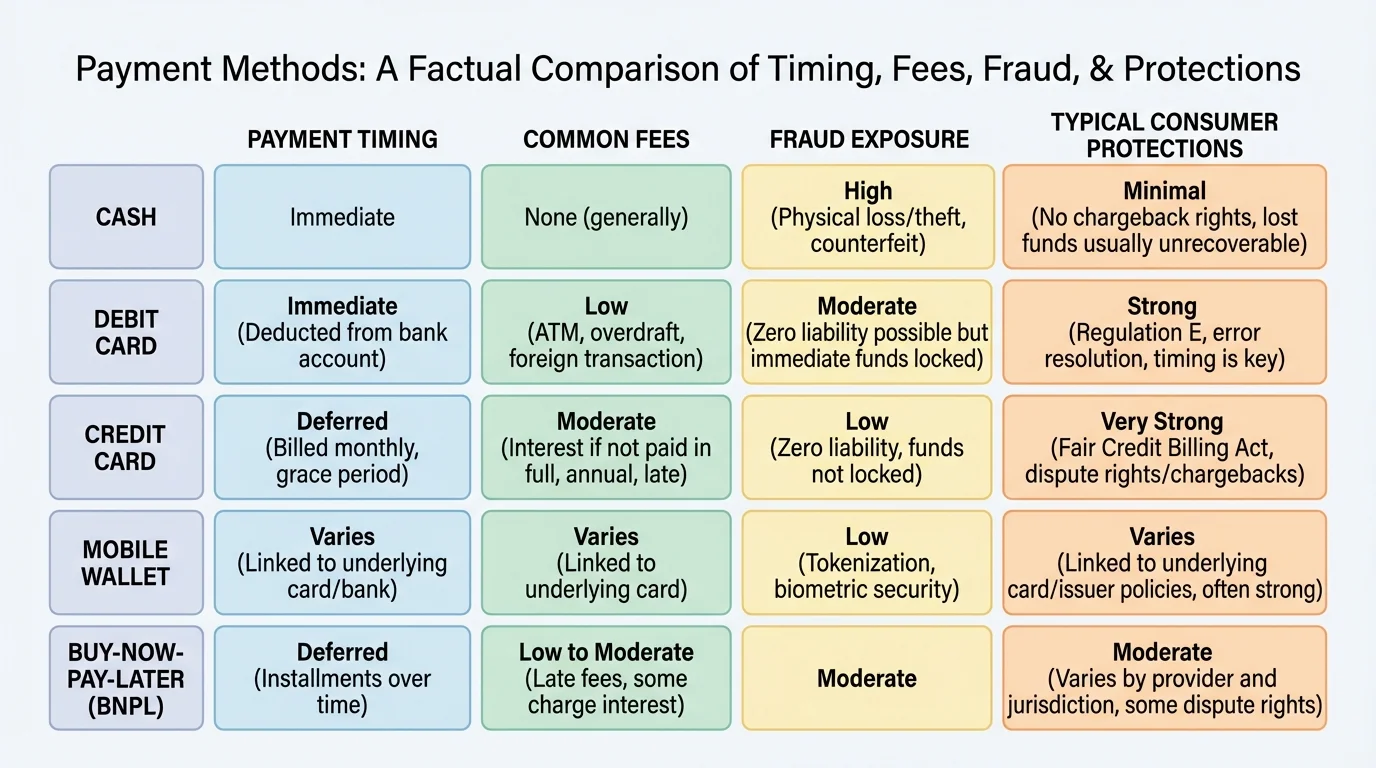

Different payment methods shift risk in different ways. Paying with cash, debit, credit, mobile apps, or installment services may all seem similar at checkout, but the legal protections are not identical.

As [Figure 2] shows, a debit card pulls money directly from a bank account. That can make budgeting easier because the money leaves immediately, but it also means fraud can affect available cash right away. A credit card uses borrowed money up to a limit and may provide stronger dispute procedures for certain purchases, although interest can build if balances are not paid in full.

Loans and credit products must be evaluated carefully. The total cost of borrowing depends on principal, fees, and interest. If a lender charges a high APR, a lower-looking monthly payment can still cost more over time. A simplified idea is that total repayment is approximately principal plus finance charges. If someone borrows $500 and pays back $560, then the finance cost is $560 minus $500, which equals \(560 - 500 = 60\). That $60 matters because borrowing is never judged only by the amount received at the start.

Electronic payments are convenient, but mistakes happen. A payment may be sent to the wrong person, a merchant may charge twice, or a thief may use stolen card information. Fast action matters. Many financial laws protect consumers only if they report the issue within a required time period.

Consumers should also understand records such as monthly statements, transaction histories, due dates, overdraft notices, and credit reports. These are not just paperwork. They are evidence. If a company says a payment was missed, the statement may prove otherwise.

| Payment method | How it works | Main risk | Useful protection habit |

|---|---|---|---|

| Cash | Immediate payment with no borrowing | Lost or stolen cash is hard to recover | Keep receipts for major purchases |

| Debit card | Money comes from bank account | Fraud can reduce available cash quickly | Monitor account activity often |

| Credit card | Borrow up to credit limit | Interest and debt growth | Pay on time and review statements |

| Mobile payment app | Digital transfer through phone or platform | Sending money to the wrong person or scammer | Verify recipient before confirming |

| Installment plan | Pay in several scheduled amounts | Late fees and hidden terms | Read the full repayment schedule |

Table 1. Comparison of common payment methods, major risks, and protective habits.

The comparison in [Figure 2] helps explain why "easy to use" does not always mean "low risk." The best payment method depends on the situation, the protections available, and the consumer's ability to track spending and respond to errors.

Several important laws regulate contracts and financial transactions in the United States. Students do not need to memorize every detail, but they should know the purpose of major protections.

The Truth in Lending Act requires lenders to disclose key borrowing terms, including the APR and other costs, so consumers can compare credit options more fairly. Without this law, lenders could hide the true price of borrowing behind confusing language.

The Fair Credit Reporting Act helps protect the accuracy, fairness, and privacy of information in credit reports. If a report contains wrong information, consumers have the right to dispute it and request an investigation.

The Equal Credit Opportunity Act prohibits certain forms of discrimination in lending. A qualified applicant should be evaluated on relevant financial factors, not unlawful bias.

The Electronic Fund Transfer Act protects consumers using electronic banking tools such as debit cards, ATMs, and some online transfers. It provides rules for disclosures, receipts, and error resolution for unauthorized electronic transfers.

The Fair Debt Collection Practices Act limits abusive, deceptive, and unfair collection behavior. Debt collectors cannot legally threaten, harass, or lie to pressure a person into payment.

Other laws and regulations address privacy, fraud, telemarketing, product safety, and identity theft. State laws also matter, especially for contracts, cancellation rights, and deceptive trade practices. Because contract rules can vary, consumers should not assume every state handles the same dispute in exactly the same way.

Earlier personal finance topics such as budgeting, credit, insurance, and recordkeeping connect directly to consumer protection. A person with an emergency fund, organized files, and good account habits can usually respond to a financial problem faster and more effectively.

Consumer laws do not guarantee that every purchase will go well. Instead, they create rules for disclosure, fairness, and correction. A strong legal protection is most effective when the consumer understands it and uses it promptly.

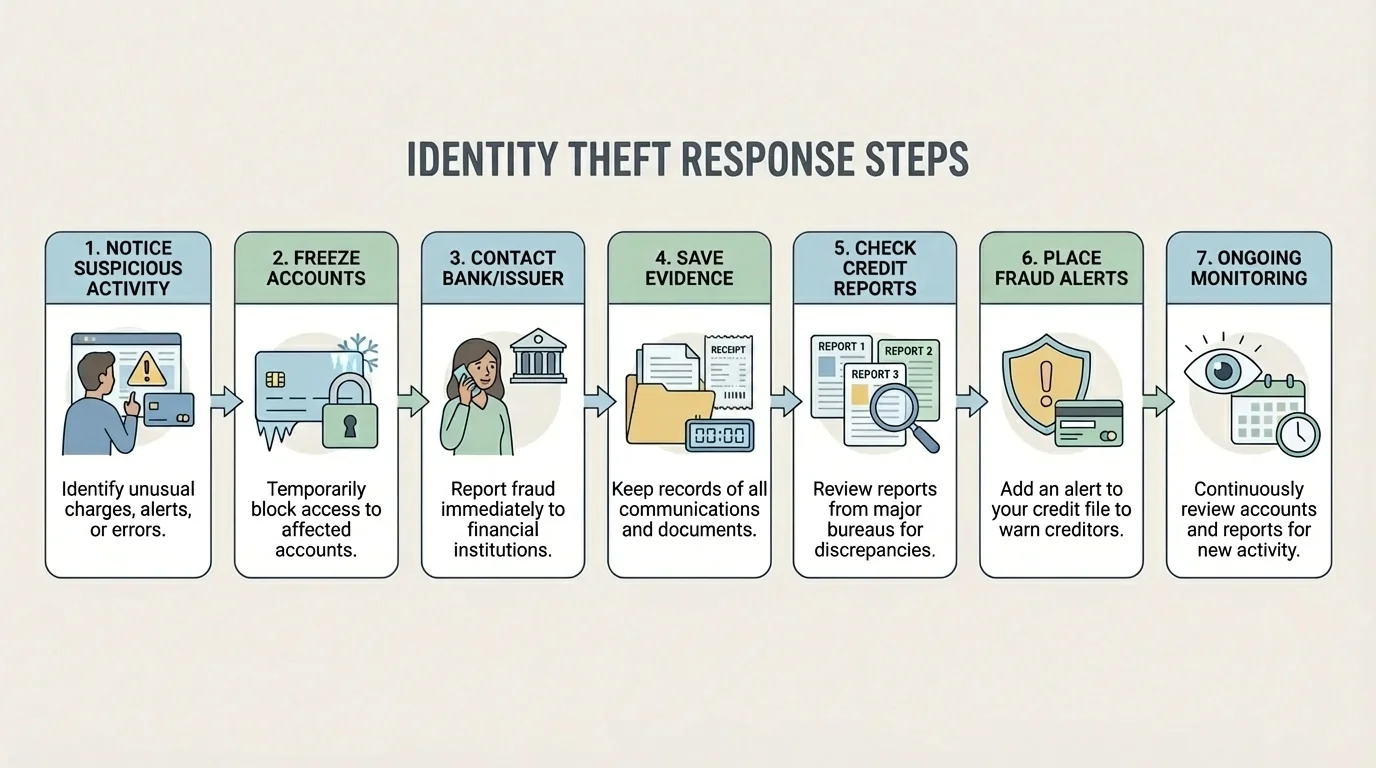

Fraud often succeeds because it looks ordinary at first. A fake text from a bank, a copied online store, or a "payment problem" email may seem urgent enough to trigger a quick response. The safest response follows a clear order: stop the damage, contact the right institution, save evidence, and monitor for continued misuse.

As [Figure 3] illustrates, identity theft happens when someone uses another person's personal information without permission, often for financial gain. This can include opening accounts, making purchases, filing false claims, or taking over existing accounts. Identity theft can affect bank balances, credit scores, and future borrowing opportunities.

Warning signs include charges you do not recognize, missing bills, alerts about password changes, unfamiliar accounts on a credit report, debt collection calls about debts you never created, or tax or medical records that do not make sense.

The first response should usually be immediate contact with the bank, card issuer, or payment platform. Consumers should freeze cards or accounts when possible, change passwords, preserve screenshots and messages, and review recent transactions. For serious identity theft, people may also place fraud alerts, freeze credit files, and report the crime to government agencies and law enforcement.

Many scams depend on emotional pressure: fear, urgency, excitement, or embarrassment. A scammer may claim your account will close in ten minutes, that you won a prize, or that a friend needs emergency money. Slowing down is a form of consumer protection.

Case study: Unauthorized debit card charge

A student notices a $92 purchase from an online electronics store that they did not make.

Step 1: Check account activity.

The student reviews recent transactions and confirms the charge is unfamiliar.

Step 2: Contact the bank quickly.

The student reports the unauthorized charge and asks the bank to block further use of the card.

Step 3: Save records.

The student takes screenshots, writes down the date and time of the report, and keeps copies of all messages.

Step 4: Monitor follow-up.

The student checks whether provisional credit, investigation updates, or replacement-card notices arrive as expected.

Fast reporting often improves the consumer's legal protection and reduces the chance of larger losses.

The sequence shown earlier in [Figure 3] is useful beyond identity theft. The same pattern works for many payment disputes: notice the problem, secure the account, document everything, and follow the formal reporting process.

Consider an online store offering designer shoes at an unbelievably low price and asking for payment through an app transfer only. This situation raises several warning signs: unrealistic pricing, limited payment choices, and weak buyer protections. A responsible consumer pauses, researches the seller, checks reviews, and avoids payment methods that are hard to reverse.

Now consider a phone contract that advertises "$0 today" but requires long monthly payments and includes a steep fee for leaving early. The consumer has the right to clear disclosure of the real costs, but also the responsibility to read the financing agreement before accepting it. The best question is not "What do I pay today?" but "What am I promising over time?"

A third example involves a credit report error. Suppose a student applies for an apartment after graduation and learns that a delinquent account appears on the report even though it belongs to someone else with a similar name. Consumer law gives the right to dispute inaccurate reporting, but the consumer should submit copies of identification, account records, and a written explanation.

These situations show a repeated pattern. Good consumer decisions combine legal awareness with practical habits: reading carefully, comparing options, documenting transactions, guarding information, and reporting problems immediately.

When a dispute cannot be solved informally, consumers can contact the business, their bank or card issuer, a state attorney general's office, a consumer protection agency, or a federal agency such as the Consumer Financial Protection Bureau or the Federal Trade Commission, depending on the issue. Credit bureaus are also important when correcting report errors.

Clear communication matters. A strong complaint usually includes the date of the transaction, the amount involved, account information, copies of receipts or statements, the exact problem, and the resolution requested. Emotional language is less effective than specific evidence.

Sometimes consumers also have cancellation rights for certain transactions, especially when laws provide a limited period to cancel specific kinds of agreements. However, these rights are not universal. That is why people should never assume they can always back out later.

Being a consumer in modern life means making decisions in a system filled with convenience, legal language, advertising, and digital risk. The smartest consumers are not the ones who never encounter problems. They are the ones who know their rights, carry out their responsibilities, and act quickly when something goes wrong.