Have you ever wondered where money goes after a person deposits it, swipes a debit card, or takes out a loan for a car? Financial institutions help people do all of those things every day. They are important because they help people keep money safer, pay for things, save for the future, and sometimes borrow money when they need help paying for something big.

A financial institution is a business or organization that helps people manage money. Instead of hiding cash at home, people often use financial institutions to store money more safely. These institutions also keep records, which means customers can see how much money came in, how much went out, and how much is left.

Financial institutions make money easier to use. A person can deposit a paycheck, use a debit card at a store, withdraw cash from an ATM, or transfer money to another account. They also offer services that help with future goals, like saving for a bike, a college education, a house, or retirement many years later.

Another reason people use financial institutions is that they provide different tools for different money jobs. Some tools are for everyday spending. Others are for saving. Others are for borrowing, and some are for trying to grow money over time.

A checking account is a type of account used for everyday spending and paying bills.

A savings account is a type of account used to hold money for later and often earns interest.

A loan is money that is borrowed and must be paid back, usually with extra money called interest.

An investment is money put into something with the hope that it will grow over time, although growth is not guaranteed.

When people understand these tools, they can make smarter choices. A fifth grader may not open every kind of account yet, but understanding them now builds strong money habits for the future.

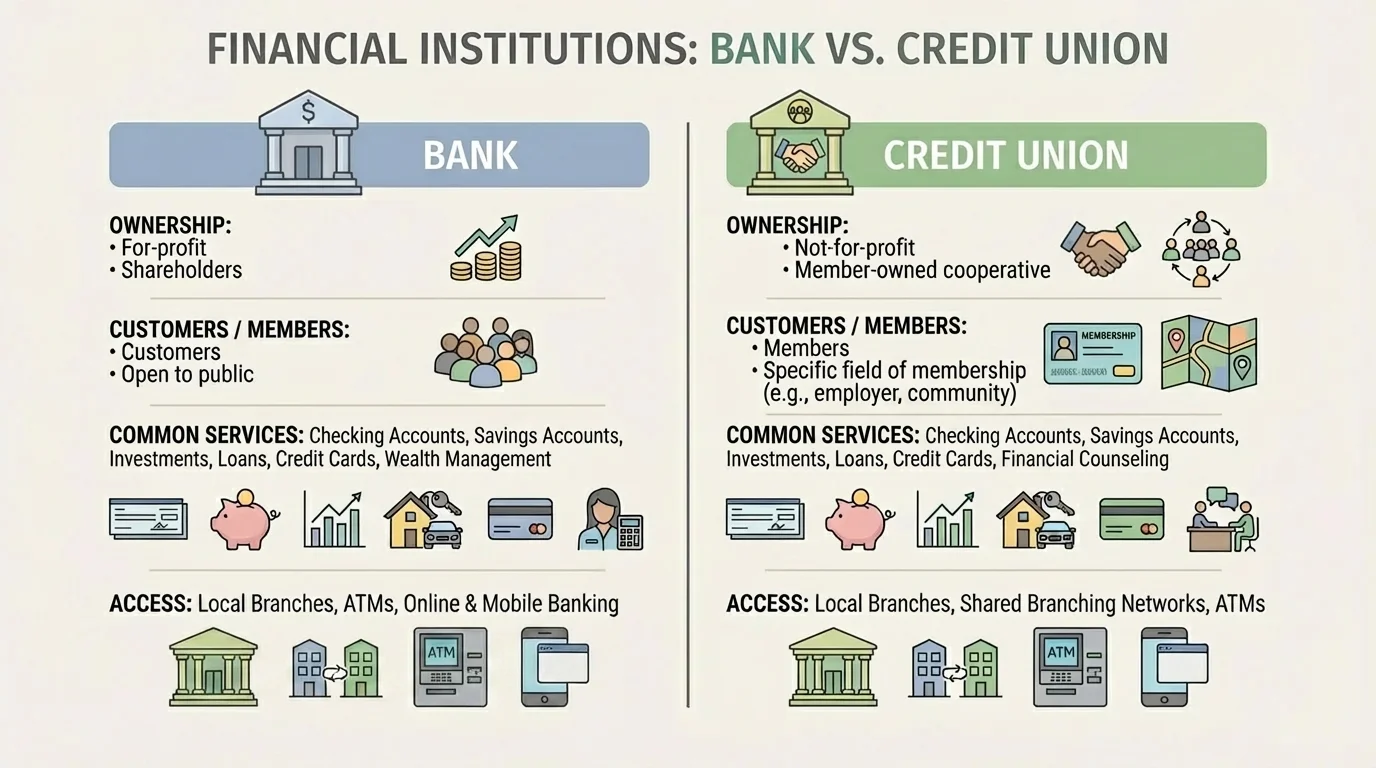

The two most common kinds of financial institutions are banks and credit unions. They can seem very similar because both often offer checking accounts, savings accounts, debit cards, loans, and online banking. However, they are organized differently, as [Figure 1] shows in a side-by-side comparison.

A bank is a business that offers money services to customers. Banks may be small local banks or very large national banks with many branches. Some banks are owned by stockholders, which means people have invested in the business and aim to earn profits.

A credit union is a financial cooperative owned by its members. A person usually joins a credit union because of where they work, where they live, or another connection. Instead of having customers only, credit unions have members who share ownership. Because of this, credit unions may focus strongly on serving members and may sometimes offer lower fees or better rates.

There are also online banks. These banks do not always have buildings that customers can visit in person. Instead, people use websites and apps to check balances, transfer money, and pay bills. Online banks can be convenient, but some people still prefer a branch where they can talk face-to-face with an employee.

No matter what type a person chooses, the main purpose is similar: helping people manage money safely and effectively. Later, when deciding where to open an account, people compare services, fees, location, and convenience. That comparison connects back to the differences we saw in [Figure 1].

Some credit unions started because groups of workers wanted a trusted place to save and borrow money together. That cooperative idea is why members are considered owners.

It is important to remember that not every bank or credit union is exactly the same. One bank may have many ATMs, while another may have fewer fees. One credit union may focus on local families, while another serves workers in a certain job.

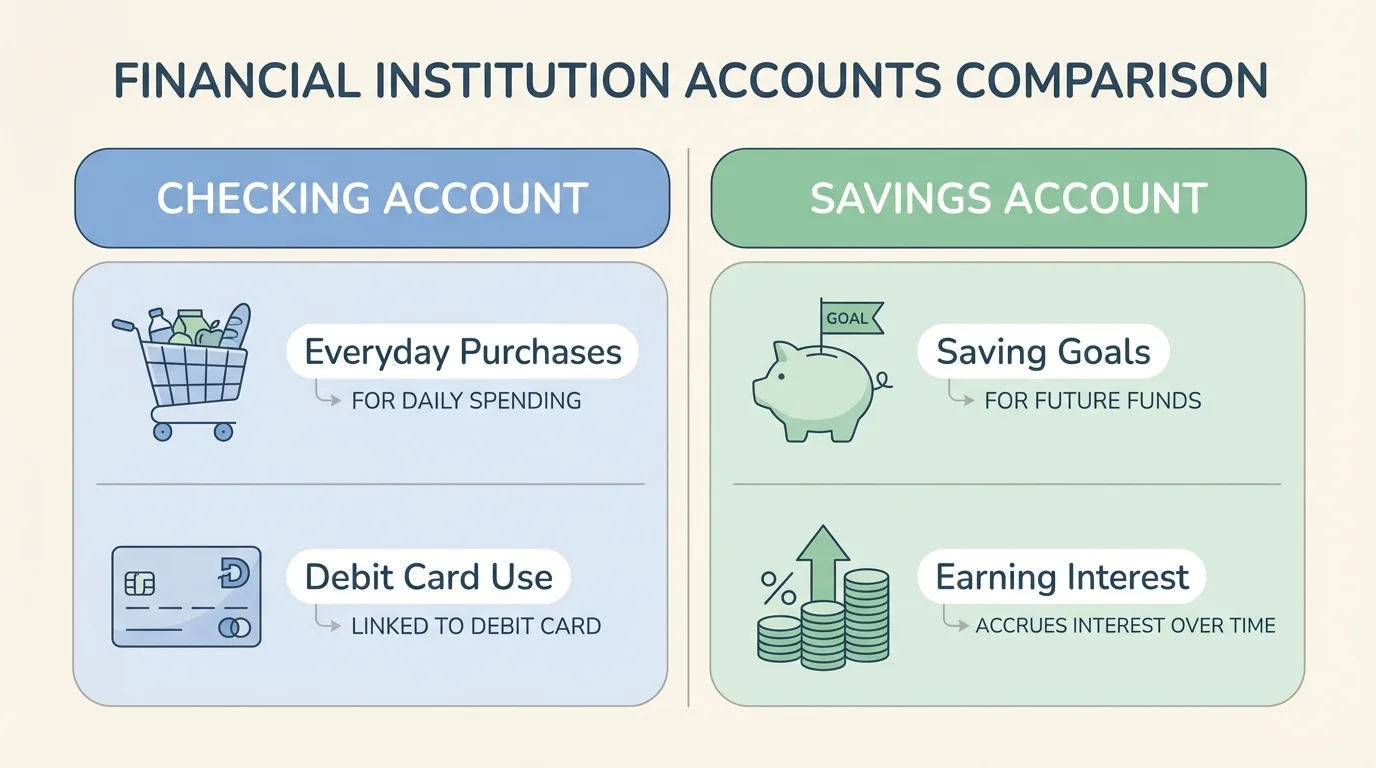

Two of the most common account types are checking accounts and savings accounts. These accounts help with different goals, and [Figure 2] compares money used often with money kept for later. Knowing the difference helps people choose the right place for each dollar they have.

A checking account is designed for money that people use often. It is useful for buying groceries, paying bills, or making purchases with a debit card. Many checking accounts allow withdrawals often, and some come with checks, debit cards, mobile apps, and online bill pay.

For example, if Elena receives $20 for helping with yard work and plans to use $12 soon to buy a book, a checking account would be a good place to keep money she expects to spend soon. After buying the book, she would have $8 left because \(20 - 12 = 8\).

A savings account is meant for money a person wants to keep for a future goal. A savings account is not usually for constant spending. Instead, it helps people separate money they want to protect and build over time.

Many savings accounts earn interest. Interest is extra money the financial institution pays for keeping money in the account. If a child saves $100 and earns $2 in interest, the account grows to $102 because \(100 + 2 = 102\). The amount may be small at first, but over time it can grow.

Checking accounts and savings accounts work best together. A family might keep spending money in checking and money for emergencies or goals in savings. If they want to save $10 each week for a game system, after \(4\) weeks they would have \(10 \times 4 = 40\) dollars saved, not counting any interest.

Choosing between checking and savings

Marcus has $50 from birthday gifts. He wants to spend $15 this week on a soccer ball and save the rest for later.

Step 1: Separate the spending money from the saving money.

Spending money: $15

Saving money: \(50 - 15 = 35\), so $35 is left to save.

Step 2: Match each amount to the best account.

The $15 that Marcus plans to use soon fits a checking account better.

The $35 he wants to keep for later fits a savings account better.

This helps Marcus organize his money by purpose.

As students think about future financial choices, the simple comparison in [Figure 2] remains useful: checking is mainly for frequent use, while savings is mainly for storing money for later goals.

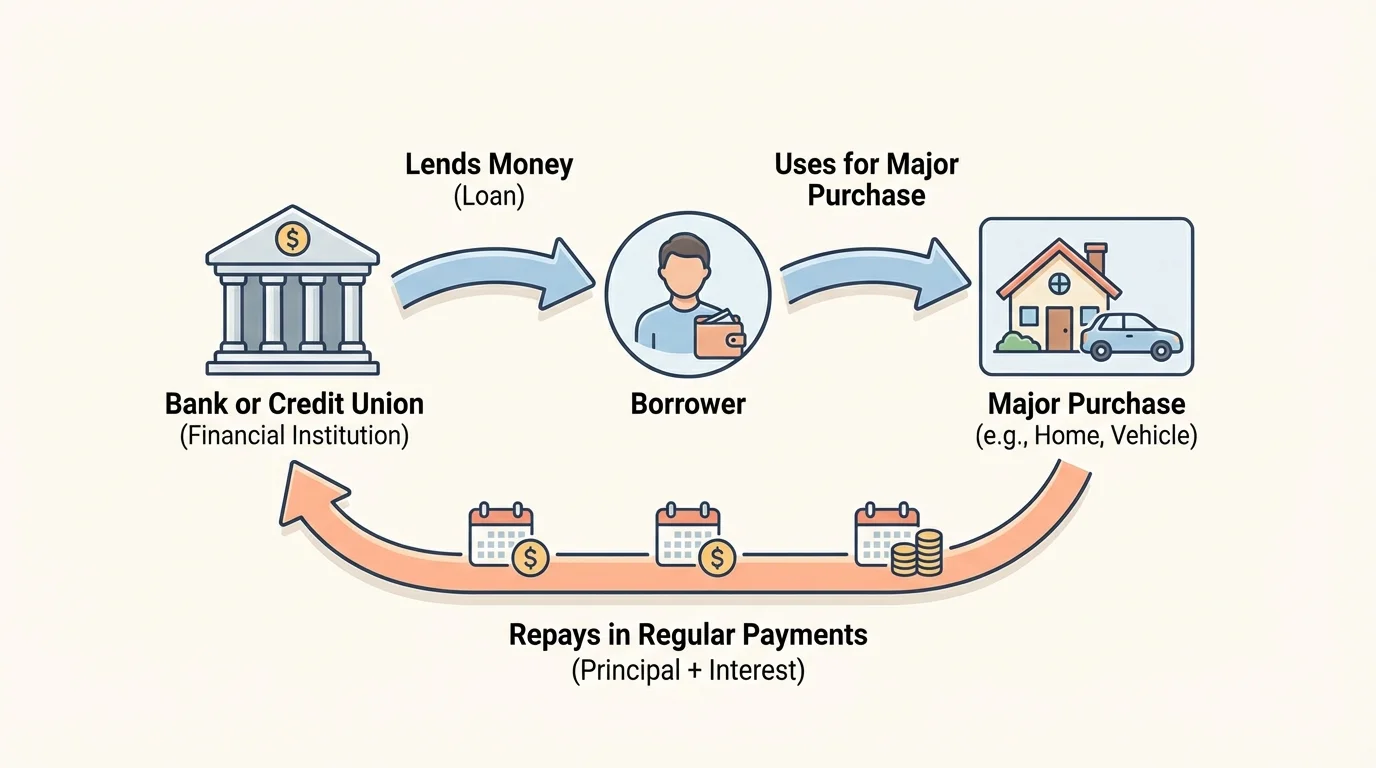

Sometimes people do not have enough money to pay for something important all at once. In that case, they may use a loan. A loan lets a person borrow money now and pay it back over time, as [Figure 3] illustrates with the path from lender to borrower to repayment.

When a bank or credit union gives a loan, it expects the borrower to repay the amount borrowed plus interest. The original amount borrowed is called the principal. Interest is the cost of borrowing. If a person borrows $500 and pays back $530, then the extra cost is $30 because \(530 - 500 = 30\).

People use loans for many reasons. Adults may take out car loans, home loans, or personal loans. A small business owner might borrow money to buy equipment. A family might use a loan to handle a major need when they cannot pay the full amount at once.

Loans can be helpful, but they must be used carefully. Borrowing means making a promise to repay. If a person borrows more than they can manage, repayment becomes difficult. That is why lenders check whether a borrower is likely to repay on time.

A monthly payment plan divides the total repayment into parts. If a person owes $240 and repays it in \(12\) equal monthly payments, each payment is \(240 \div 12 = 20\) dollars per month, not including extra fees or additional interest that may apply in real situations.

Why interest matters in a loan

Interest is not just extra money added for no reason. It is how the lender earns money for allowing someone to use borrowed funds. The more money borrowed, or the longer it takes to pay back, the more important it becomes to understand the total cost.

Thinking about total repayment helps people compare choices. The borrowing process shown in [Figure 3] reminds us that a loan does not end when money is received. The full job includes repayment over time.

Saving money is important, but some people also want their money to grow over long periods of time. That is where investments come in. An investment is money put into something, such as stocks, bonds, or a business, with the hope that it will increase in value.

Investments are different from savings accounts. A savings account is usually designed to keep money safer and easier to reach. Investments can grow more, but they also involve more risk. Risk means there is a chance the value could go down as well as up.

For a simple example, suppose someone invests $100. If the value grows by $10, the investment becomes $110 because \(100 + 10 = 110\). But if the value drops by $8 instead, the investment becomes $92 because \(100 - 8 = 92\). This is why investments are not the same as storing money in a regular savings account.

Adults often use investments for long-term goals, such as retirement or college savings. They may choose different kinds of investments depending on how much growth they want, how much risk they can handle, and how long they plan to leave the money invested.

Saving and investing are not opposites. Many people do both. Savings are often for shorter-term needs or emergency money, while investments are often for longer-term growth.

Even though fifth graders may not invest on their own yet, understanding the idea is useful. It teaches an important lesson: different financial tools are built for different goals.

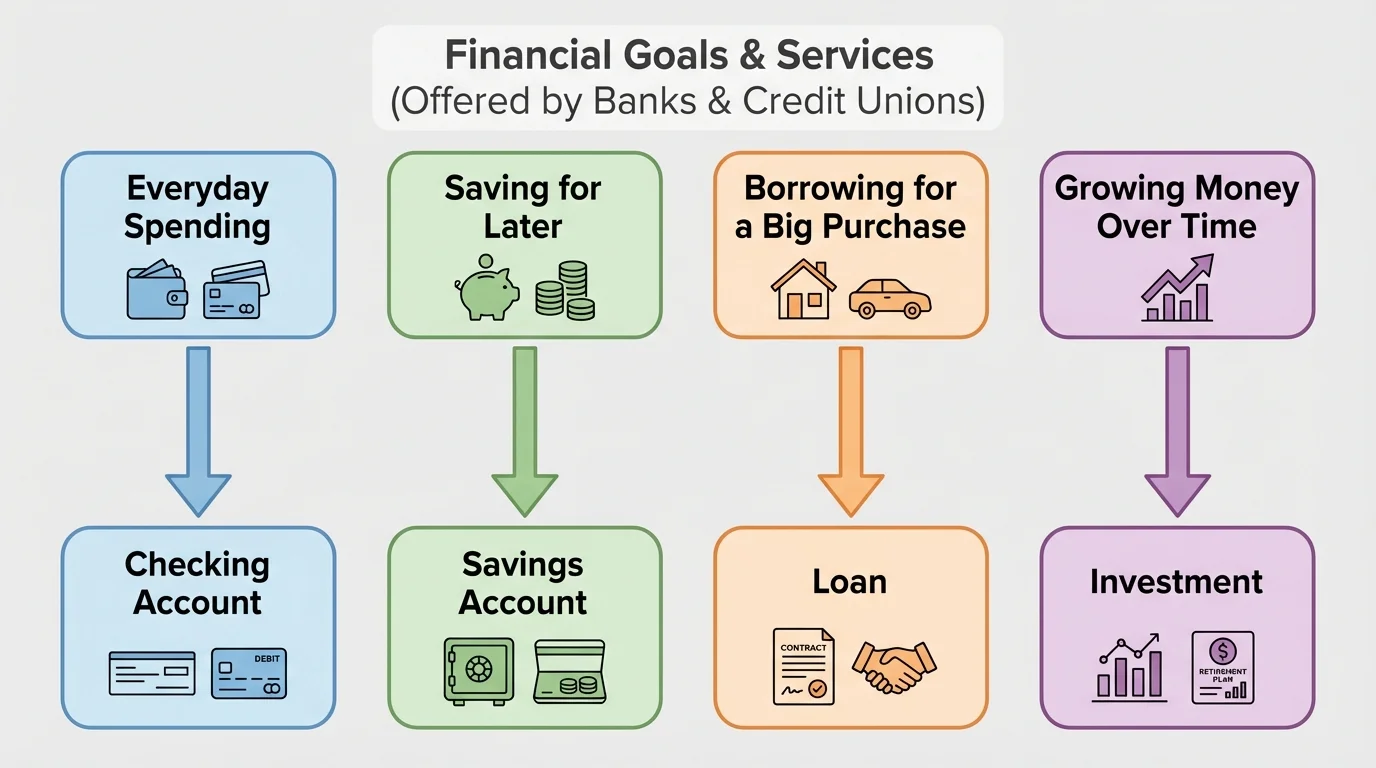

No single bank account or financial institution is perfect for every person. The best choice depends on what someone needs the money to do, and [Figure 4] matches common goals to useful services. A person who needs to spend often may choose differently from a person who wants to save quietly for months.

When comparing financial institutions, people often look at fees, branch locations, ATM access, apps, customer service, and interest rates. For example, one checking account might charge a monthly fee, while another may not. One savings account might pay more interest than another.

A family may choose a credit union because it is nearby and has lower fees. Another family may choose a large bank because it has many ATMs in different cities. Someone else may choose an online bank because using a phone app is most convenient.

People also match services to goals. If the goal is daily spending, checking may fit best. If the goal is building emergency money, savings may be better. If the goal is paying for something expensive now and repaying later, a loan may be needed. If the goal is long-term growth, an investment may make sense.

| Service | Main Purpose | Example Use |

|---|---|---|

| Checking account | Frequent spending | Buying groceries or paying bills |

| Savings account | Money for later | Saving for a trip or emergency fund |

| Loan | Borrowing money | Paying for a car or home |

| Investment | Trying to grow money | Long-term future goals |

Table 1. Comparison of common financial services and their main purposes.

Students can return to the decision paths in [Figure 4] whenever they ask a simple question: "What job does this money need to do?" That question helps lead to the right service.

Using financial institutions wisely also means using them safely. People should protect account numbers, passwords, PINs, and debit cards. Sharing this information with the wrong person can lead to stolen money or unauthorized purchases.

Another good habit is checking account records. A bank statement or app shows deposits, withdrawals, and purchases. Looking at records helps people notice mistakes and keep track of spending. If someone deposits $25 and later spends $7 and $6, the remaining amount is \(25 - 7 - 6 = 12\) dollars.

People should also be careful about fees. Some accounts charge for using certain ATMs, having too little money in the account, or missing loan payments. Reading the rules helps people avoid surprises.

Reading an account record

Sofia has $40 in an account. She deposits $15, then uses $9 for a purchase.

Step 1: Add the deposit.

\(40 + 15 = 55\), so the new balance is $55.

Step 2: Subtract the purchase.

\(55 - 9 = 46\), so the balance becomes $46.

By checking the record, Sofia knows exactly how much money is left.

Good money habits begin with understanding. When people know the difference between banks and credit unions, and when they understand checking accounts, savings accounts, loans, and investments, they are better prepared to make wise choices with their money.