A surprising number of money problems do not begin with low income. They begin with missing information. People forget a bill due date, lose track of a subscription, cannot prove a purchase, or do not notice a false charge until weeks later. A strong financial system does not require wealth. It requires organization. Learning to keep and use financial records means building a reliable picture of where your money comes from, where it goes, and how your choices connect to your goals.

Financial records are documents or saved information that show money coming in, money going out, assets owned, debts owed, and agreements related to money. Good recordkeeping supports both everyday choices and major life decisions. If you want to build savings, compare jobs, apply for college, rent an apartment, share expenses fairly, or prepare taxes, records make those decisions more accurate and less stressful.

Financial records also help you act on your values. Suppose one student values independence and wants to save for a car, while another values community involvement and wants to donate regularly to a local cause. Both students need records to see whether their spending matches their priorities. Without records, money choices can feel random. With records, choices become intentional.

Financial recordkeeping is the process of collecting, organizing, storing, updating, and using money-related documents and information. Cash flow is the movement of money in and out of your life over time. Reconciliation is the process of comparing two sets of records, such as your spending log and your bank statement, to make sure they match.

Records are also proof. A pay stub proves you were paid. A receipt proves what you purchased and when. A bank statement shows transactions that actually cleared your account. An insurance document proves coverage. If a problem arises, records turn memory into evidence.

Many students think financial records only matter once they have a full-time job. In reality, they start much earlier. If you earn money from part-time work, receive money through an app, buy items online, pay for transportation, or subscribe to streaming services, you already have financial records.

Main categories of records include income records, spending records, banking records, tax records, debt records, savings and investment records, and legal or service agreements. One important technical document is a pay stub, which shows your earnings, hours, and deductions. Another useful document is a receipt, which gives proof of a purchase. A monthly bank statement lists deposits, withdrawals, and balances. A contract may explain payment terms, cancellation rules, or penalties.

Digital life creates records too. Debit card transactions, payment app histories, email confirmations, online invoices, automatic subscription charges, and downloaded statements all count. A record does not have to be on paper to matter. In fact, many people now keep most records digitally.

| Record Type | What It Shows | Why It Matters |

|---|---|---|

| Pay stub | Earnings, hours, deductions | Confirms income and explains take-home pay |

| Receipt | Item purchased, amount, date | Proof of purchase, returns, warranties |

| Bank statement | Account activity and balance | Tracks actual transactions and helps catch errors |

| Bill or invoice | Amount due and due date | Prevents late payments |

| Tax form | Income reported for tax purposes | Needed for tax filing and financial aid processes |

| Loan record | Amount owed, interest, payment terms | Helps manage debt responsibly |

| Insurance document | Coverage, premiums, claim information | Proves protection and explains costs |

Table 1. Common financial records, the information they contain, and why they are useful.

A recordkeeping system should be simple enough to maintain and detailed enough to be useful. If a system is too complicated, people stop using it. If it is too loose, important details get lost. The best system is one you can update regularly in a few minutes each week.

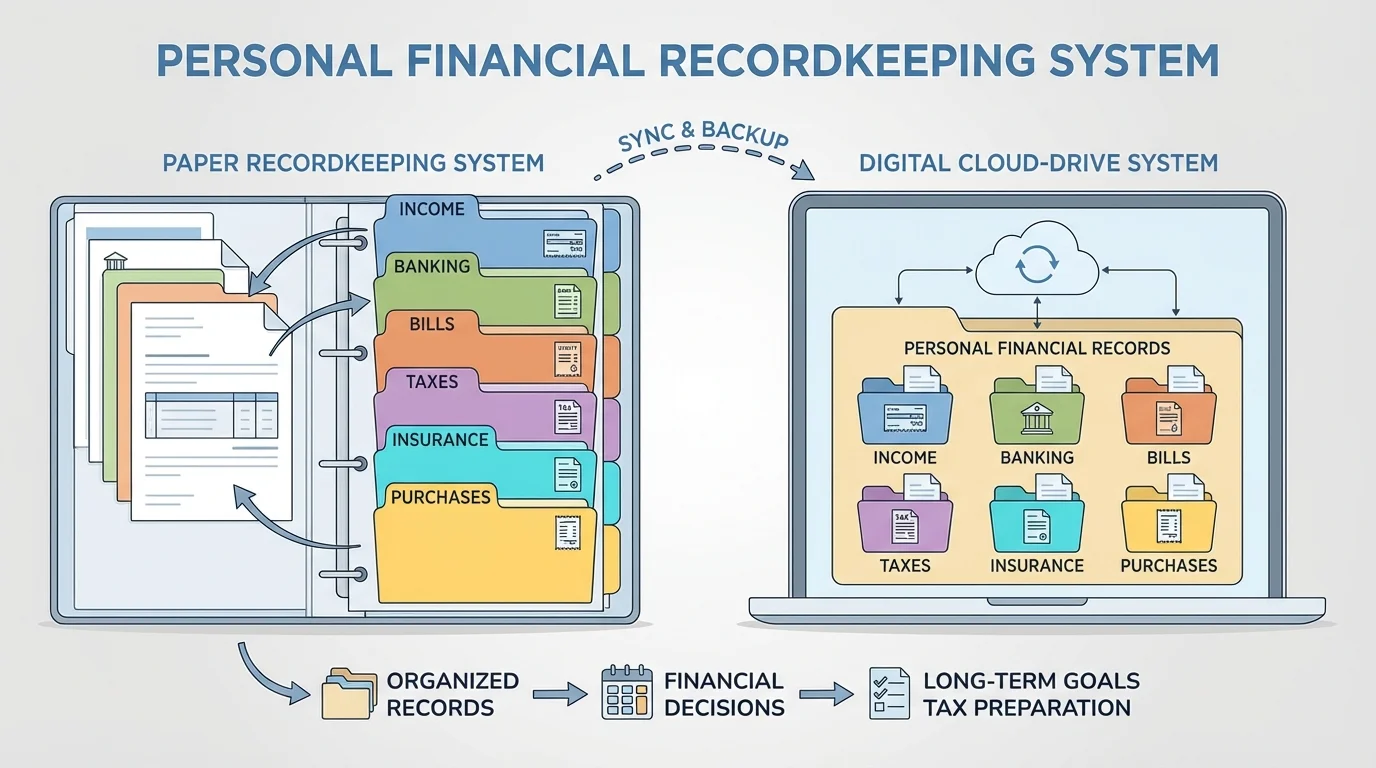

As [Figure 1] shows, you can use a paper system, a digital system, or a combination of both. A paper system might include a binder or file box with labeled sections. A digital system might use cloud folders, scanned PDFs, and a spreadsheet. Many people use both: paper copies for major legal documents and digital copies for monthly tracking.

Start by creating broad categories such as Income, Banking, Bills, Taxes, Insurance, Loans, Savings, and Purchases. Inside each category, sort by month or year. Name files consistently. For example, instead of saving a statement as "document1," use a clear format such as "2026-03 checking statement" or "2026-04 phone bill." A date-first format helps files sort in order.

Consistency matters more than perfection. If every receipt, statement, and bill enters the same system, finding information becomes much easier. If half your records are in email, some are in a backpack, and some are saved with random names, using them later becomes frustrating and time-consuming.

A good system reduces decision fatigue. When categories, file names, and update times are already chosen, you do not have to invent a method every time you get paid or buy something. That consistency makes it more likely that your records stay complete and accurate.

A useful routine might look like this: once a week, save digital receipts, enter transactions into your tracker, and review your balances; once a month, download statements and compare them to your records; once a year, move older files into a yearly archive. As we saw in [Figure 1], the system works best when each document has an obvious place.

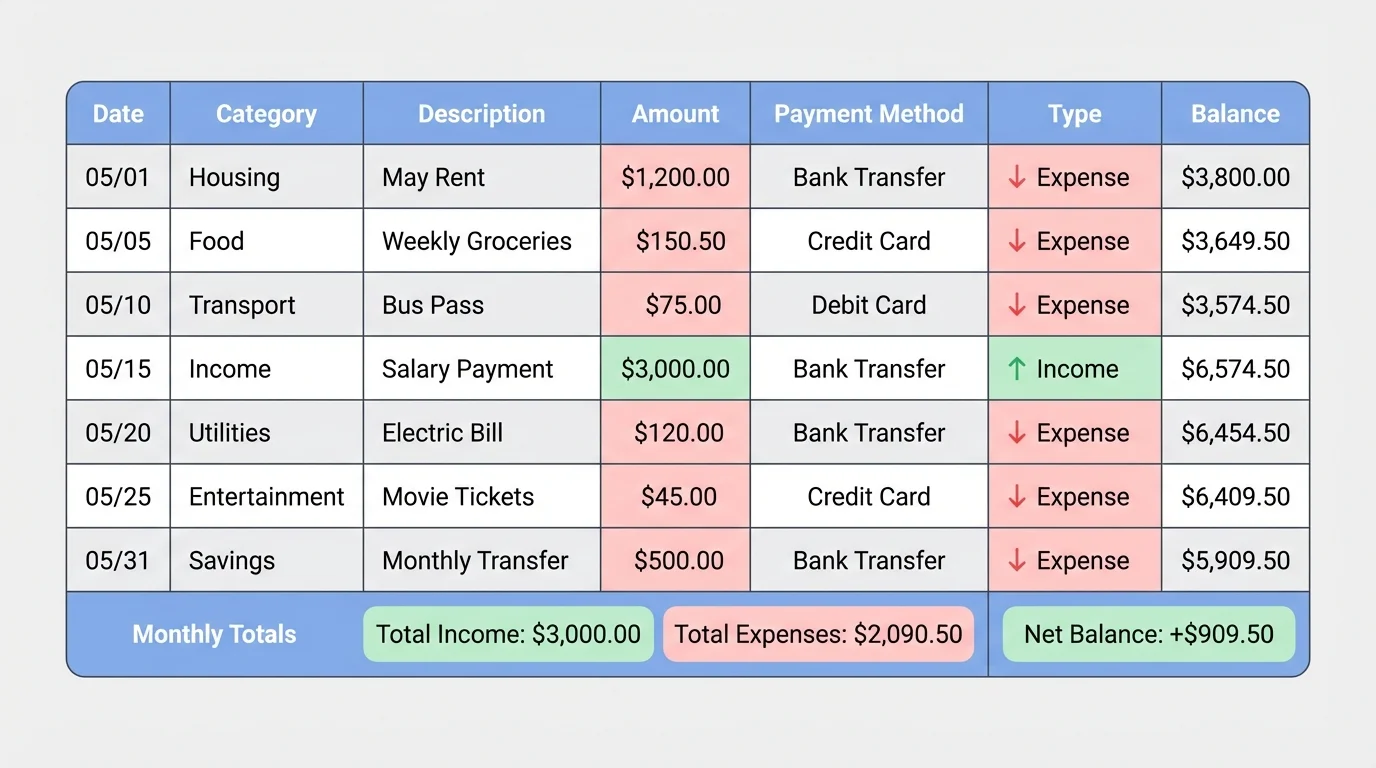

A strong recordkeeping system does more than store papers. As [Figure 2] illustrates, it helps you measure your money habits. A transaction log turns scattered purchases into a pattern. Each entry should include the date, description, category, amount, and payment method.

Common spending categories include food, transportation, clothing, entertainment, school costs, gifts, savings, and subscriptions. Income categories may include wages, tips, gifts, refunds, or money from selling items. When categories stay consistent, you can compare one month to the next.

To evaluate your financial position for a period, calculate net cash flow:

\[\textrm{Net Cash Flow} = \textrm{Total Income} - \textrm{Total Expenses}\]

If the result is positive, more money came in than went out. If it is negative, you spent more than you received during that time.

Worked example: finding monthly net cash flow

A student earns $420 from a part-time job, receives $35 for tutoring a younger neighbor, and spends $58 on transportation, $96 on food, $24 on a music subscription, $40 on school supplies, and $75 on entertainment during one month.

Step 1: Add total income.

\[420 + 35 = 455\]

Total income is $455.

Step 2: Add total expenses.

\[58 + 96 + 24 + 40 + 75 = 293\]

Total expenses are $293.

Step 3: Subtract expenses from income.

\[455 - 293 = 162\]

Net cash flow is $162.

This means the student has $162 available to save or use for future expenses.

A transaction tracker is especially useful because small purchases add up. Five snacks at $4 each may not seem important at the moment, but over a month that becomes \(5 \times 4 = 20\) dollars, and repeated habits can grow much larger over a year. A clear monthly tracker makes those patterns visible instead of hidden.

Keeping records is only half of the skill. The other half is using them. Your records help answer questions such as: Can I afford this purchase? Am I meeting my savings goal? Which expenses are fixed and which are flexible? Is a subscription worth its cost? Which spending categories are higher than I expected?

A budget becomes much more realistic when it is based on actual records instead of guesses. If your records show that transportation usually costs about $60 per month and food away from home averages about $90, you can build a plan that reflects real life. Good records also help you compare choices. For example, if a student is deciding whether to buy a used laptop now or save for a better one later, past records show how much can realistically be set aside each month.

Worked example: using records to set a savings timeline

A student wants to save $600 for a used laptop. Their records show an average monthly net cash flow of $150.

Step 1: Identify the goal and monthly saving capacity.

Goal: $600

Available each month: $150

Step 2: Divide the goal by the monthly amount.

\[\frac{600}{150} = 4\]

Step 3: Interpret the result.

If the student consistently saves $150 per month, the goal can be reached in 4 months.

Without records, this plan would be only a guess. With records, it becomes a realistic timeline.

Financial records also help with shared spending. If friends split a streaming service, club fee, or travel cost, written records reduce conflict. Instead of relying on memory, everyone can refer to actual numbers and dates.

Decision-making becomes stronger when records connect to values. A student who cares about avoiding debt may use records to build an emergency fund. A student who values generosity may track donations along with other expenses. A student focused on education may use records to compare how much money can go toward books, exam fees, or college applications.

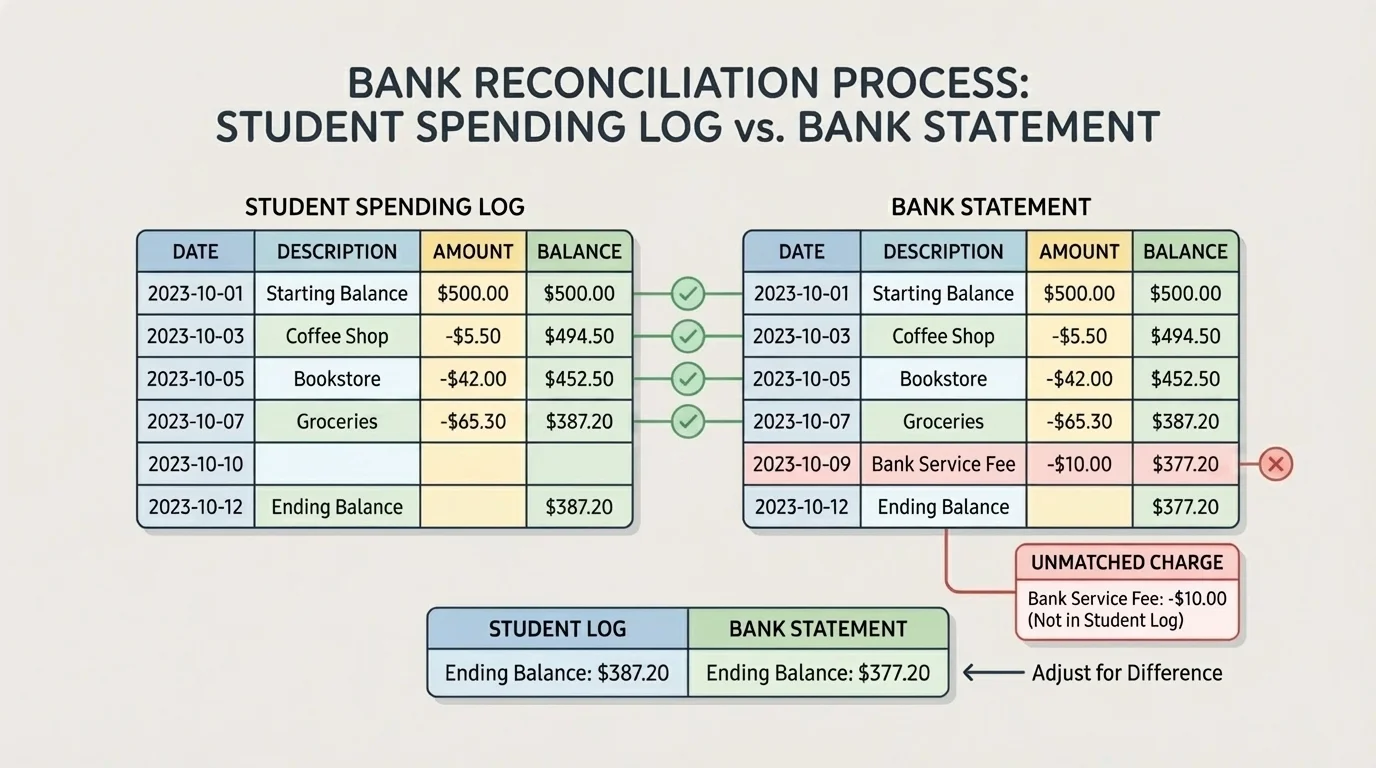

No system is complete unless it also checks for mistakes. As [Figure 3] illustrates, reconciliation means comparing your own records with an outside source such as a bank statement to confirm that every transaction matches. This process can reveal forgotten purchases, double charges, bank errors, or unauthorized transactions.

Suppose your tracker shows a purchase of $18.50 at a café, but your bank statement shows $28.50. That difference matters. Maybe you entered the amount incorrectly, maybe a tip was added, or maybe there is an error. Reconciliation helps you investigate instead of guessing.

A simple way to reconcile is to mark every transaction in your log that appears on the statement. Any unmatched item needs attention. This line-by-line check is especially important for debit cards, payment apps, and automatic withdrawals.

Protecting records is just as important as organizing them. Financial records often contain private details such as addresses, account numbers, earnings, or identification information. Digital files should be stored with strong passwords and, when possible, two-factor authentication. Important files should be backed up in more than one place, such as a device and secure cloud storage.

Identity theft often begins with small pieces of information collected over time, not with one dramatic event. A lost statement, weak password, or shared screenshot can give away enough details for someone to misuse an account.

Paper records need protection too. Keep major documents in a safe location. Shred papers that contain sensitive personal information before throwing them away. Later, when you review suspicious charges or account changes, the checking process from [Figure 3] helps you respond quickly.

Not every document needs to be kept forever, but some should be stored much longer than others. Short-term records, such as monthly bills and routine receipts, may only need to be kept until you confirm the payment, complete a return, or finish the month's review. Other records are more important for the long term.

Keep tax-related documents for several years, because they may be needed for filing questions, financial aid applications, or proof of income. Keep contracts, loan agreements, insurance policies, major purchase records, and warranty information as long as they remain active and often beyond that if they document ownership or legal responsibility. Records related to major life events, education, or long-term assets may deserve permanent storage.

| Retention Group | Examples | Typical Reason for Keeping |

|---|---|---|

| Short-term | Routine receipts, monthly utility bills | Proof of payment, returns, monthly review |

| Medium-term | Bank statements, annual summaries, school payment records | Budget review, account history, planning |

| Long-term | Tax forms, contracts, loan records, insurance policies | Legal proof, applications, debt tracking |

| Permanent or very long-term | Major ownership records, important legal identity documents | Ongoing proof of identity or ownership |

Table 2. General categories for how long different kinds of financial records are usually kept.

Consider Maya, a high school student with a part-time job, a checking account, and a goal of saving $1,200 for college-related costs. She creates digital folders labeled Income, Banking, Spending, School, Taxes, and Savings. Each week, she downloads receipts from online purchases, photographs paper receipts, and enters all transactions into a spreadsheet.

In one month, Maya records income of $520 and expenses of $410. Her net cash flow is

\[520 - 410 = 110\]

so she transfers $100 into savings and keeps $10 in her checking account as an extra cushion. After reviewing her records, she notices that food delivery appeared four times and cost a total of $68. That number surprises her because each order seemed small by itself. Her records reveal a pattern she had not noticed.

Worked example: comparing planned and actual spending

Maya planned to spend $50 on entertainment but actually spent $74.

Step 1: Find the difference.

\[74 - 50 = 24\]

Step 2: Interpret the result.

She spent $24 more than planned.

Step 3: Use the record to adjust a decision.

Because her records identify the overage clearly, she can decide whether to reduce entertainment next month or lower another category intentionally.

This is how records support better decisions: they turn vague feelings into measurable facts.

Over several months, Maya can compare trends. If her average monthly savings becomes $100, then reaching a goal of $1,200 would take

\[\frac{1,200}{100} = 12\]

months. That timeline helps her decide whether she needs to increase income, reduce spending, or adjust the goal date.

One common mistake is keeping records but never reviewing them. A pile of saved receipts does not help much unless the information is organized and used. Another mistake is mixing categories so that spending cannot be analyzed clearly. For example, if transportation, snacks, and school supplies are all listed as "miscellaneous," it becomes harder to learn from the records.

Students also sometimes forget irregular expenses. A monthly budget may look fine until seasonal costs appear, such as sports fees, gifts, testing fees, or annual subscriptions. Recordkeeping should include these less frequent expenses so they do not feel like surprises later.

Accurate financial decisions depend on reliable information. Estimating is useful for quick thinking, but long-term planning works best when supported by actual records, verified amounts, and regular review.

Another problem is relying only on memory. Memory is useful for stories, but not for precise money management. If you cannot remember whether a charge was $14.99 or $19.99, a saved record answers the question immediately. If you are unsure how much you saved last quarter, your records provide evidence.

Good habits include entering transactions soon after they happen, saving records in one place, reviewing them on a schedule, and comparing them to outside sources for accuracy. These habits reduce stress and increase control. Over time, recordkeeping becomes less of a chore and more of a tool for independence.

"What gets measured gets managed."

— A widely used principle in business and personal finance

When people manage money without records, they are often reacting. When they manage money with records, they are planning. That difference matters in school, at work, in families, and in communities where financial choices affect more than one person.