A budget is one of the few places where values turn into numbers. Two households can earn the same amount of money and live completely different financial lives because one plan directs money with purpose while the other reacts to each bill as it arrives. Designing a household budget is not only about avoiding overspending. It is about deciding what matters most, covering real responsibilities, and still making room for future goals such as college, a car, an apartment, travel, or retirement.

At its core, a household budget is a plan for how money will be earned, spent, saved, and sometimes borrowed over a period of time. Most household budgets are made monthly because many expenses, such as rent and insurance, are due each month. A strong budget helps people pay for necessities, prepare for emergencies, and reduce stress because they know where their money is going.

Every budget is built on the idea of trade-offs. Money spent in one category cannot be spent somewhere else. If a person spends more on entertainment, they may have less available for savings. If they save more for a future goal, they may need to limit impulse purchases now. That is why budgeting is closely connected to decision-making and consumer skills.

A good budget also helps separate short-term wants from long-term priorities. Buying a new phone case, ordering food several times a week, or paying for multiple streaming subscriptions may seem small by themselves. But repeated small expenses can take away money that could be used for larger goals. In one month, spending $8 three times a week adds up to $96, because \(8 \times 12 = 96\).

Small recurring purchases often affect a budget more than one-time big purchases because they are easy to ignore. A person who overlooks a $12 subscription and a $6 weekly snack habit may lose more than $500 in a year.

Budgeting does not mean never spending on fun. It means choosing spending intentionally. A well-designed budget includes both obligations and enjoyment, but it makes sure enjoyment does not damage stability.

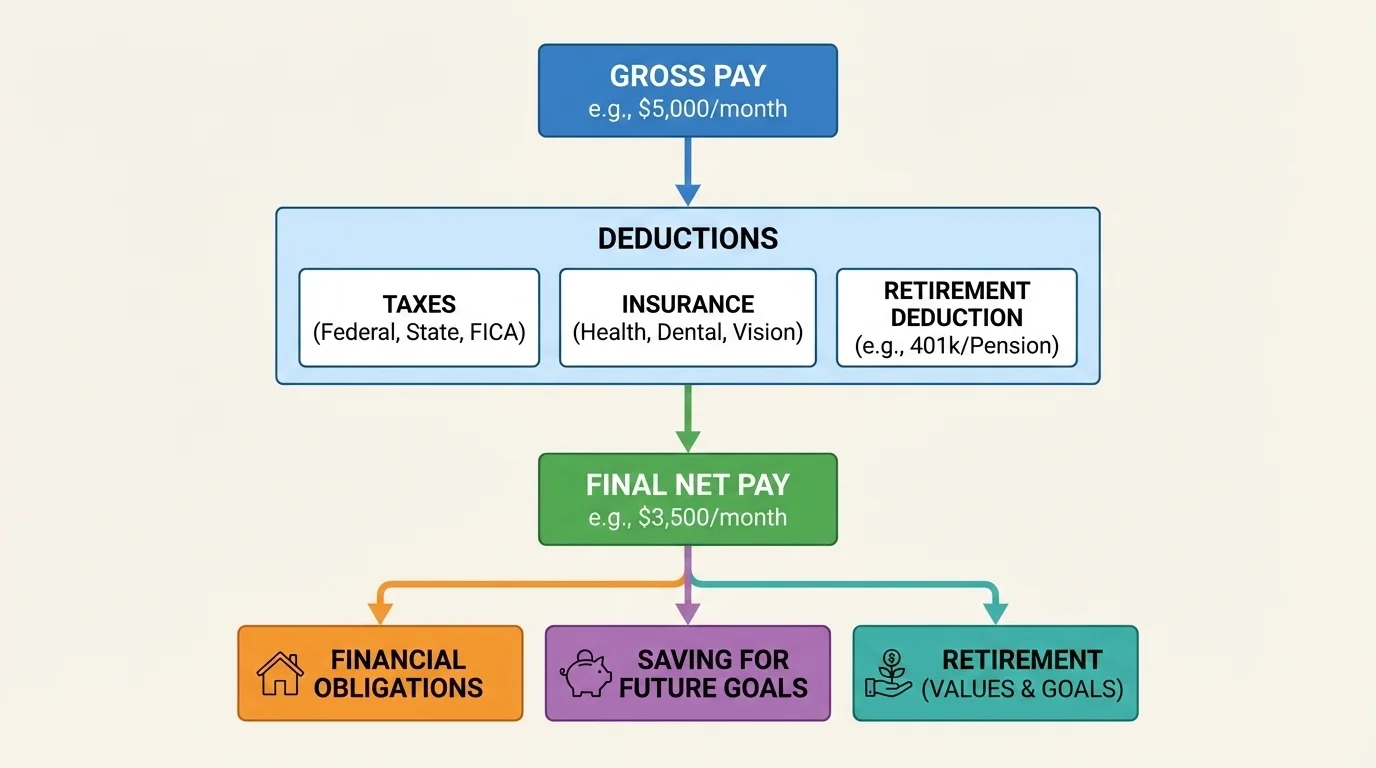

Before building a budget, it is essential to understand income correctly. A paycheck is not the same as the amount a worker actually gets to spend, as [Figure 1] shows by comparing total earnings and take-home pay. This is where two important terms matter: gross income and net income.

Gross income is the total amount earned before deductions. Net income is the amount left after deductions such as taxes, insurance, and retirement contributions. Net income is often called take-home pay.

If a person earns $2,800 in gross monthly income, that does not mean they can budget $2,800 for spending. Deductions may reduce the amount actually available. For example, if taxes are $420, health insurance is $110, and retirement contributions are $140, then net income is calculated as follows:

\[\textrm{Net income} = 2800 - 420 - 110 - 140 = 2130\]

That means the budget should be based on $2,130, not $2,800. Using gross income for spending decisions can cause serious problems because it overestimates the money available.

Net income can come from more than one source. In a household, there may be wages, tips, freelance work, government benefits, child support, or investment income. When building a budget, all reliable income sources should be added together. If income changes from month to month, it is safer to use a conservative estimate based on a lower average.

Some deductions are required, such as many taxes. Others may be optional or partly optional, such as retirement contributions. This matters because a person may choose to increase or decrease some deductions depending on their goals, but reducing retirement contributions today can affect long-term security later, a point that becomes clearer again in [Figure 4].

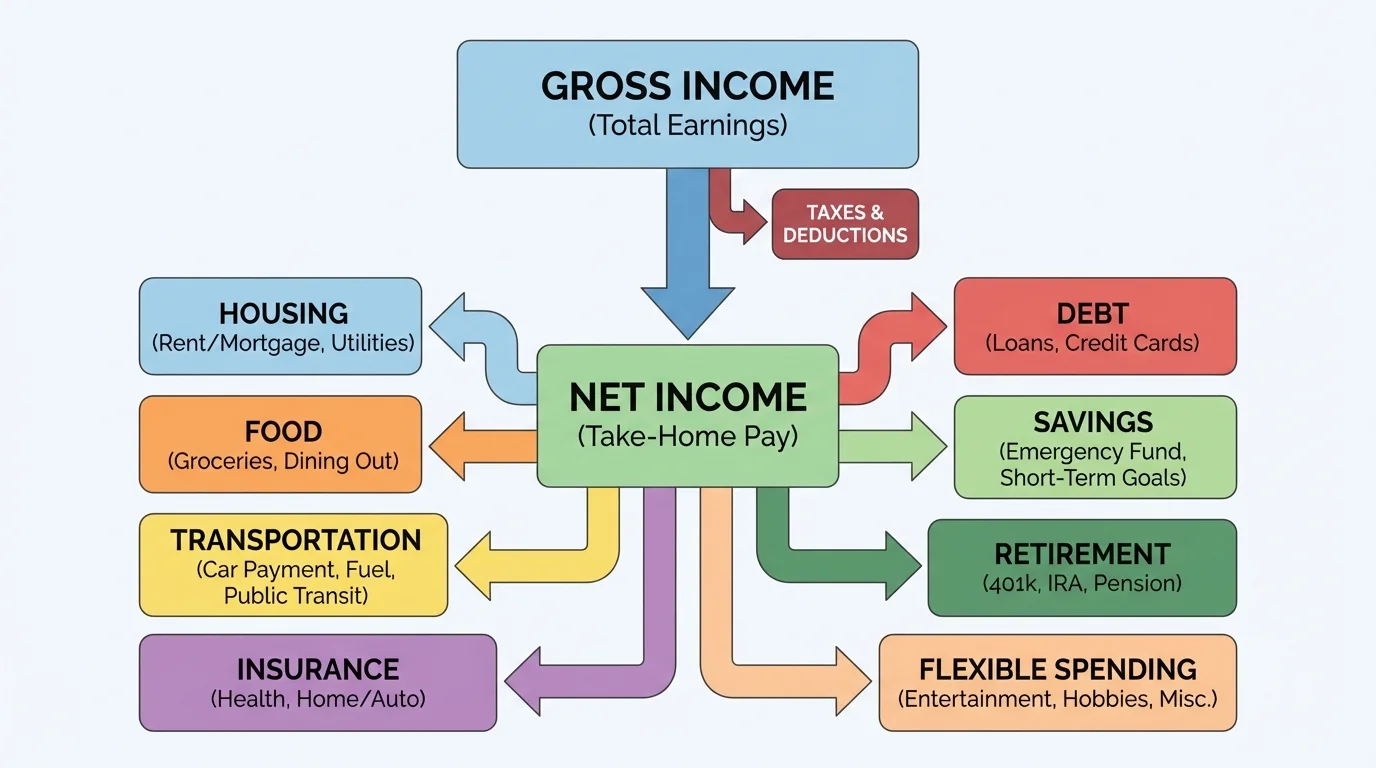

A household budget organizes money into categories, and each category has a different level of flexibility, as [Figure 2] illustrates. Some expenses are predictable and required, while others can be adjusted more easily. Understanding these categories helps people respond wisely when money is tight.

Fixed expenses are costs that stay about the same each month. Examples include rent, a car payment, internet service, or a student loan payment. These are usually the hardest to change quickly.

Variable expenses change from month to month. Grocery costs, gas, electricity, and entertainment often vary. These categories usually offer more opportunities for adjustment.

Financial obligations are payments a household is responsible for making. These include housing, utilities, insurance, transportation, minimum debt payments, and essential food costs. Obligations come before optional spending.

A complete budget should also include periodic expenses, which do not happen every month but still must be planned for. Examples include holiday gifts, school fees, vehicle registration, annual memberships, and medical copays. A smart way to handle these is through a monthly set-aside amount.

Another major category is savings. Savings should not be treated as "whatever is left over," because often nothing is left over. Instead, savings should be included as a planned category. This may include an emergency fund, savings for a future purchase, or money for education.

Retirement belongs in a budget too, even for young people. Retirement may seem far away, but beginning early gives savings more time to grow. A small amount started early can become much larger than a bigger amount started late because of growth over time.

| Category | Purpose | Examples |

|---|---|---|

| Housing | Secure shelter | Rent, mortgage |

| Utilities | Keep home functioning | Electricity, water, internet |

| Food | Meet basic needs | Groceries, limited dining out |

| Transportation | Travel to work or school | Gas, bus pass, car payment |

| Insurance | Manage risk | Health, auto, renters insurance |

| Debt | Meet borrowing obligations | Credit card minimums, loans |

| Savings | Prepare for future needs | Emergency fund, car fund |

| Retirement | Support long-term security | Retirement account contributions |

| Flexible spending | Personal choice spending | Clothes, entertainment, hobbies |

Table 1. Major household budget categories and the purpose of each category.

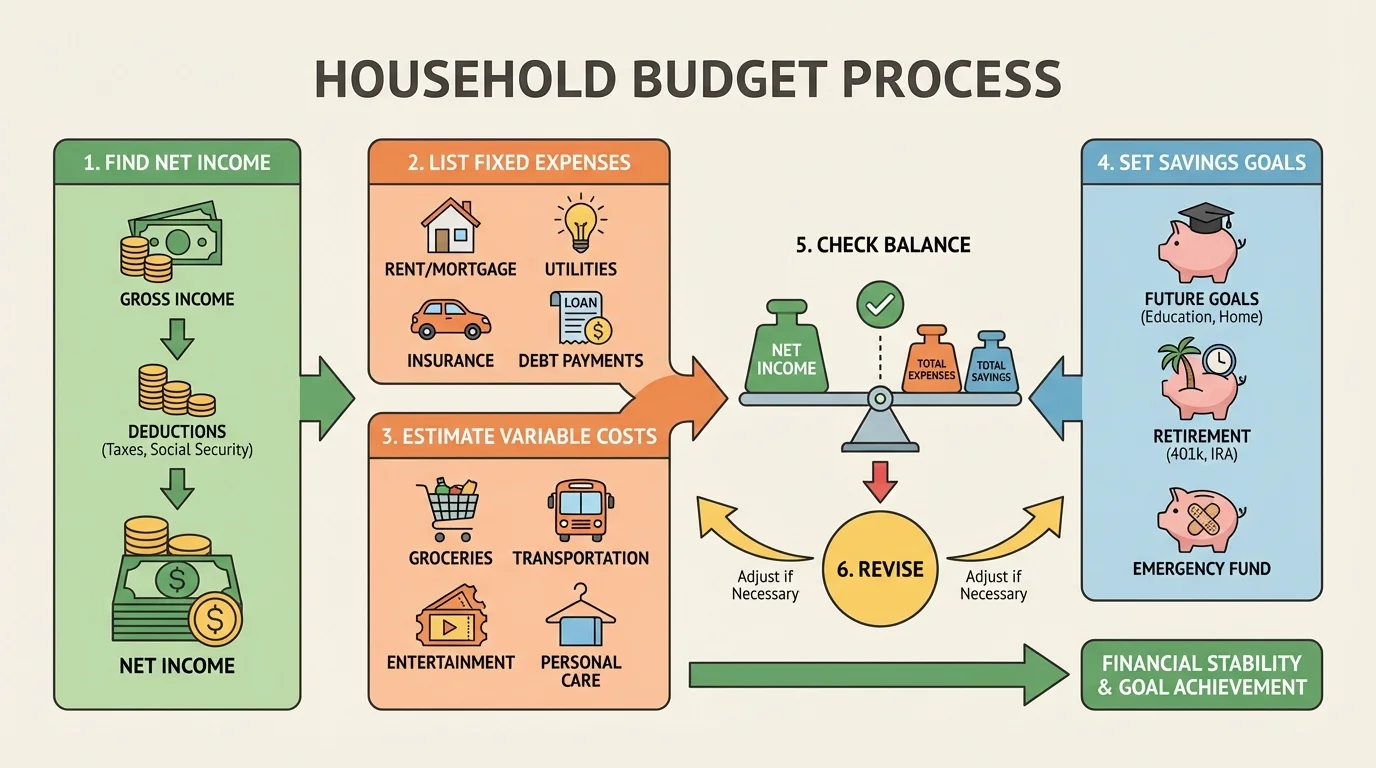

Budgeting works best when it follows a clear process rather than a guess, and [Figure 3] presents that process from income to revision. The goal is to make sure money has a planned job before it is spent.

Step 1: Find total monthly net income. If income is weekly or every two weeks, convert it to a monthly amount carefully.

Step 2: List fixed expenses and required bills first. These are usually the least flexible and most urgent.

Step 3: Estimate variable expenses realistically. It is better to overestimate slightly than to pretend spending will always be lower than usual.

Step 4: Add savings and retirement categories based on goals and values.

Step 5: Compare total planned outflows with total net income. A balanced budget satisfies the relationship \(\textrm{income} - \textrm{expenses} - \textrm{savings} = 0\), meaning every dollar has been assigned a purpose.

Step 6: If planned outflows exceed net income, revise the budget. Usually, flexible spending is reduced first. Sometimes larger structural changes are needed, such as lowering housing costs, increasing income, or refinancing debt.

A budget should reflect values. Someone who strongly values education may save aggressively for college courses. Someone who values stability may focus first on an emergency fund. Someone supporting family members may place more of the budget toward obligations at home. There is no single perfect budget for every person, but there are healthy principles: cover needs, protect against risk, reduce harmful debt, and save for the future.

The best way to understand budgeting is to build one from actual numbers. Consider a household with one working adult and one teenager. The adult earns $3,200 in gross monthly income. Deductions are $480 for taxes, $120 for insurance, and $160 for retirement contributions.

Worked example 1: Find net income

Step 1: Start with gross monthly income.

Gross income is $3,200.

Step 2: Add total deductions.

Total deductions are \(480 + 120 + 160 = 760\) dollars.

Step 3: Subtract deductions from gross income.

\[\textrm{Net income} = 3200 - 760 = 2440\]

The household has $2,440 in net monthly income available for budgeting.

Now suppose the household estimates the following monthly budget categories to be paid from net income: rent $900, utilities $180, groceries $350, transportation $220, phone $70, debt payment $120, emergency savings $150, and flexible spending $250. Retirement contributions are not included here because they were already deducted from pay.

Worked example 2: Total the planned expenses

Step 1: Add all listed budget categories.

\(900 + 180 + 350 + 220 + 70 + 120 + 150 + 250\)

Step 2: Calculate the sum.

\[900 + 180 + 350 + 220 + 70 + 120 + 150 + 250 = 2240\]

Step 3: Compare total planned expenses to net income.

\[2440 - 2240 = 200\]

This budget leaves $200 unassigned.

That extra $200 should not simply disappear through random spending. It can be assigned intentionally. For example, the household might put $100 toward a car repair fund and $100 toward a college savings goal.

Worked example 3: Adjust the budget to match a goal

Suppose this household wants to save $300 per month for a future car instead of $100.

Step 1: Find the additional amount needed.

Additional car savings needed: \(300 - 100 = 200\).

Step 2: Use the $100 already available.

After using that amount, the remaining gap is \(200 - 100 = 100\).

Step 3: Reduce flexible spending by $100.

Flexible spending becomes \(250 - 100 = 150\).

The revised budget now supports the household's goal without exceeding net income.

This example shows a central idea: budgeting is not only arithmetic. It is decision-making guided by priorities.

Values shape budgets in powerful ways. If a person values independence, they may focus on building emergency savings and avoiding unnecessary debt. If they value family support, they may choose a smaller entertainment budget so they can contribute more to household needs. If they value future opportunity, they may put more toward education or skill development.

Goals can be short-term, medium-term, or long-term. A short-term goal might be saving $300 for school supplies. A medium-term goal might be saving $4,000 for a used car. A long-term goal might be retirement or buying a home. Different goals require different strategies, but all of them should appear in the budget.

One useful approach is to divide goals into time horizons and monthly amounts. If a student wants $1,200 for a laptop in one year, the monthly savings target is:

\[\frac{1200}{12} = 100\]

That means saving $100 per month. If the budget cannot support that amount, the student must change one of three things: increase income, reduce spending elsewhere, or extend the timeline.

This is where consumer skills matter. Comparing prices, avoiding impulse buying, and reading contract terms can protect room in a budget. A lower phone plan or cheaper insurance policy can create money for goals without reducing quality of life much.

Saving is easier when it has a clear purpose. People are more likely to protect savings when they know what it is for. An emergency fund is money set aside for unexpected costs, such as medical bills, urgent travel, or car repairs. Without it, households may need to borrow and pay interest.

Another useful tool is a sinking fund. A sinking fund is money saved gradually for a known future expense, such as gifts, school fees, or replacing tires. Instead of being surprised by a bill, the household prepares in advance.

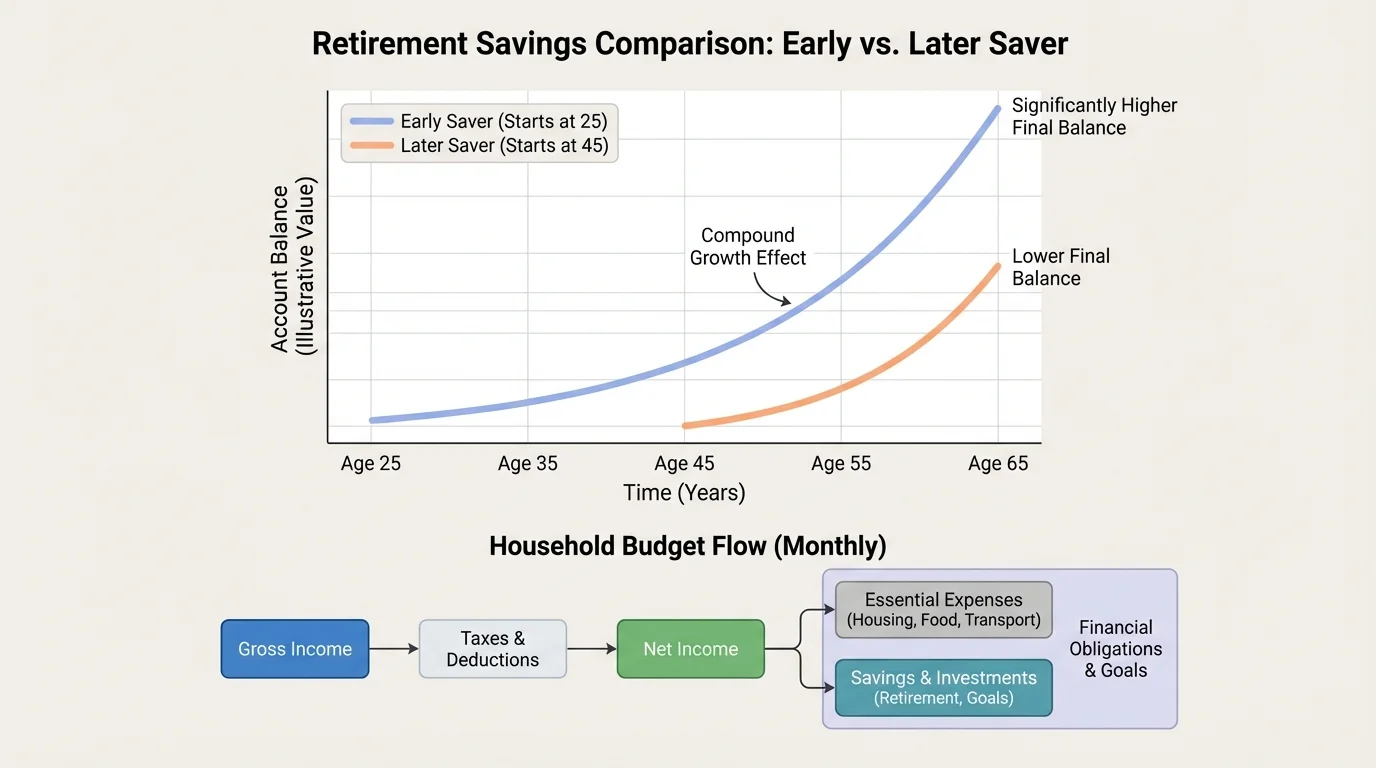

Why retirement saving starts earlier than most people expect

Retirement saving benefits from growth over time. Money in a retirement account can earn returns, and those returns may also earn returns later. This process, called compound growth, means time can be just as important as the amount saved.

Time is one of the most powerful tools in retirement planning, and [Figure 4] shows why starting earlier can matter more than people first assume. Even modest contributions begun early can outgrow larger contributions started years later.

Suppose one person saves $100 each month starting at age \(18\), while another waits until age \(28\). The exact future value depends on the rate of return, but the early saver has an extra \(10\) years of contributions and growth. That time difference can lead to a much larger balance by retirement.

Retirement savings may happen through employer-sponsored plans or individual retirement accounts. Even if students are not using these now, the principle matters: saving early lowers the pressure to save huge amounts later. As seen earlier in [Figure 1], retirement contributions may already be deducted before net pay is received, which means they should be recognized as part of the full financial plan.

A practical budget often includes savings in layers: first basic obligations, then emergency savings, then savings for known goals, and then retirement contributions. In reality, many households work on several layers at once, but all should be considered.

One challenge is irregular income. People who work part-time, seasonally, or for tips may not receive the same amount each month. In that case, budgeting from a lower average income is safer than budgeting from the highest month. If a worker earns $1,900, $2,200, and $1,700 over three months, the average is:

\[\frac{1900 + 2200 + 1700}{3} = \frac{5800}{3} \approx 1933.33\]

To stay cautious, the person might budget using about $1,900 rather than $2,200.

Another challenge is debt. Borrowing can help with major purchases or emergencies, but debt also creates future obligations. Credit cards are especially risky when balances are not paid in full because interest increases the true cost of purchases. A $500 purchase is no longer just $500 if interest is added over time.

Subscriptions are another hidden problem. A person might not notice several small automatic charges, but together they reduce flexibility. Reviewing bank statements and canceling unused services is a practical budgeting habit.

When comparing borrowing choices, remember that the lowest monthly payment is not always the cheapest option. A lower payment stretched over more months may mean paying more total interest.

Smart consumer behavior strengthens a budget. This includes comparing unit prices at stores, reading return policies, checking fees, avoiding emotional spending, and asking whether a purchase supports a real need or a meaningful goal. Budgeting is not separate from consumer skills; it depends on them.

A budget is a living plan, not a one-time document. Actual spending often differs from planned spending. The difference between a planned amount and the actual amount is called a budget variance. For example, if a household planned $300 for groceries but spent $340, then the variance is \(340 - 300 = 40\). That $40 must be covered by reducing another category or using extra income.

Tracking spending each month makes the next budget more accurate. If utility bills rise in winter, the budget should reflect that pattern. If gas spending drops because of carpooling, that category may be adjusted downward and the savings redirected.

Budgets also change when life changes. A new job, loss of income, moving, graduation, a new child, or higher insurance costs can all require revision. The purpose of budgeting is not perfection. It is awareness, control, and alignment between money and priorities.

One practical rule is to review a budget monthly and ask four questions: What income came in? What obligations were paid? What changed? What goal needs more support next month? Those questions help a household respond instead of drift.

"A budget is telling your money where to go instead of wondering where it went."

— Common personal finance principle

Designing a household budget is one of the most important financial skills a person can learn. It uses math, planning, self-control, and values all at once. When a budget is based on net income, covers financial obligations, and includes savings for both future goals and retirement, it becomes more than a spending plan. It becomes a strategy for building stability and choice over time.