Have you ever noticed that money can seem to disappear fast? One day you have enough for a snack, a small toy, and maybe some savings. A little later, it is almost gone. That happens because money has two big jobs in a budget: money comes in, and money goes out. Learning the difference between those two jobs helps you make smart choices with money.

A budget is a plan for how to use money. It helps you decide how much money you have, how much you can spend, and how much you can save. A budget is not just for grown-ups. Kids can use budgets too when they get allowance, gift money, or money for doing chores.

When you make a budget, you look at two main parts. First, you look at money that comes in. Second, you look at money that goes out. These two parts are called income and expenses. If you understand both, you can make a better plan and work toward something important, like saving for a book, a game, or a bike helmet.

Income is money that comes in to you.

Expenses are money you spend or money that goes out.

Budget is a plan that shows income, expenses, and money left to save or use later.

Financial goal is something you want to do with money, such as saving for a special item.

Even a simple budget can answer important questions: Do I have enough money? Should I wait before buying something? Can I save a little now so I can buy something bigger later? Those are smart money questions.

One important money word is income. Income is money you receive. For a child, income might not come from a job the way it often does for adults. Instead, it may come from an allowance, birthday money, money earned by helping with chores, or money earned from running a lemonade stand.

Here are some examples of income for a third grader:

All of those are forms of income because the money is coming in to the person. Income makes it possible to spend, save, or share money. Without income, there is no money to put into a budget.

Sometimes income is regular, which means it comes at the same time again and again, like $5 each week. Sometimes income is not regular, which means it comes only once in a while, like birthday money. It is helpful to know the difference because regular income is easier to plan with.

Another important money word is expense. Expenses are the money you spend on things. When you buy something, money leaves your wallet, piggy bank, or account. That is an expense.

Here are some examples of expenses for a child:

Expenses are not always bad. Many expenses are useful or necessary. Buying school supplies, paying for lunch, or replacing something important can all be good reasons to spend money. A budget does not say, "Never spend." A budget says, "Spend carefully and with a plan."

Some expenses happen often, like buying a snack. Some happen less often, like buying a present for a friend. It helps to notice both kinds so your budget feels realistic.

When people create a budget, they compare income and expenses, as [Figure 1] shows with money moving in and money moving out. Income gives the budget money to use. Expenses use some of that money. The budget helps you see whether you still have money left after spending.

If your income is greater than your expenses, you have money left over. You can save it, spend it later, or use it for a financial goal. If your expenses are greater than your income, you have a problem. You are planning to spend more than you have. That means you need to lower expenses, wait to buy something, or find a way to earn more income.

Think of a budget as a bucket. Income pours water into the bucket. Expenses let water out. If more water comes in than goes out, the bucket keeps some water. If more goes out than comes in, the bucket empties. This is why both parts matter.

You can compare them with subtraction. If Elena has $12 of income and $7 of expenses, then the money left is calculated by \(12 - 7 = 5\).

That means Elena has $5 left. The income started the budget, and the expenses reduced it. Both jobs are important, but they are not the same. Income adds to the budget. Expenses take away from the budget.

Example: Comparing income and expenses

Marcus gets $8 for chores and $4 as a gift. He spends $3 on a snack and $2 on trading cards.

Step 1: Find total income.

Marcus's income is \(8 + 4 = 12\).

Step 2: Find total expenses.

Marcus's expenses are \(3 + 2 = 5\).

Step 3: Subtract expenses from income.

Money left is \(12 - 5 = 7\).

Marcus has $7 left. His income brought in money, and his expenses used part of it.

Later, when you think about saving, the same idea still matters. Money entering and leaving the budget must be tracked, or it becomes hard to know what is left.

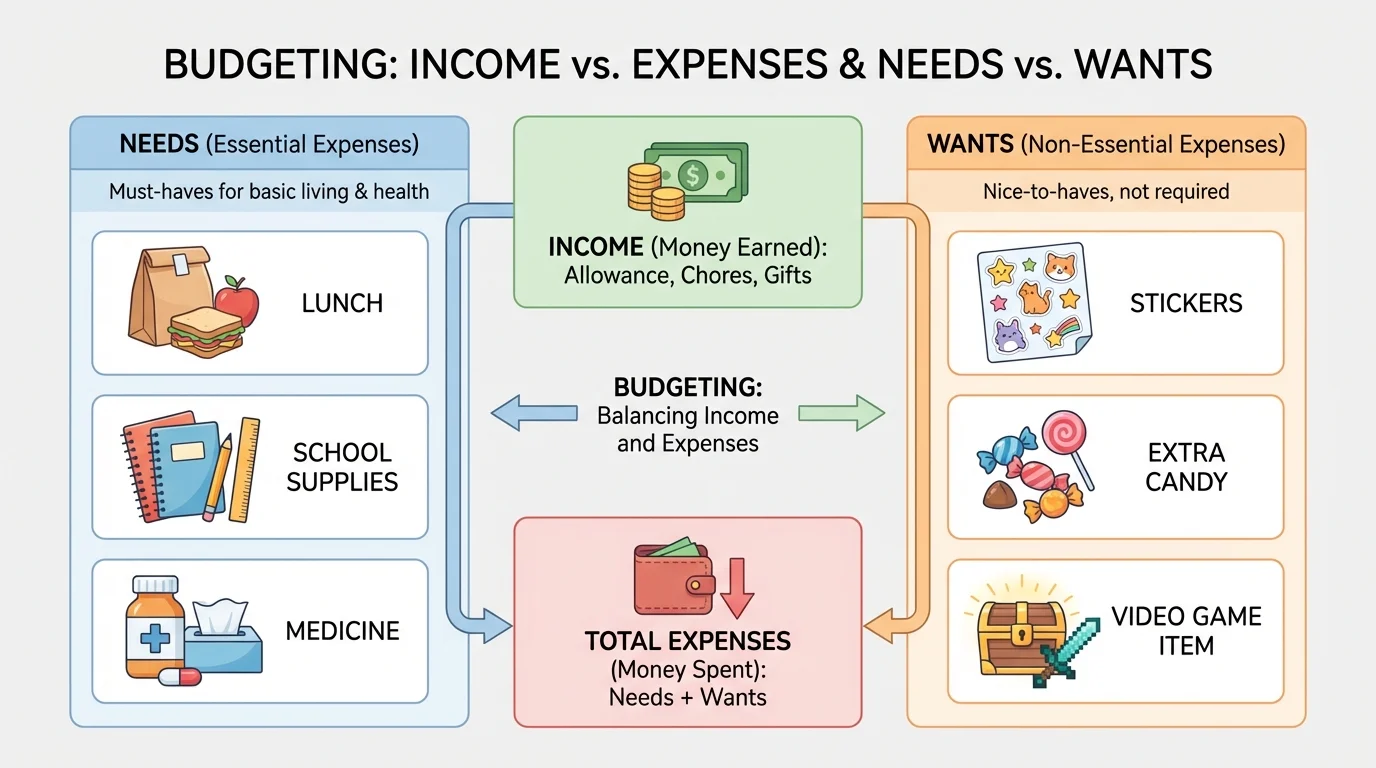

[Figure 2] Some expenses are more important than others, and a budget helps you sort them. A simple needs-and-wants chart makes this easier. A need is something important for health, safety, or learning. A want is something you would like to have but can live without.

For a child, needs might include school supplies, lunch, or medicine. Wants might include a new toy, extra candy, or a fun app purchase. Sometimes a choice is tricky. A backpack is usually a need if you do not have one. A backpack with glitter lights and extra decorations may have a want part too.

Budgets help you make choices. If money is limited, needs usually come before wants. This does not mean wants are wrong. It just means important expenses should be handled first.

Suppose Ava has $10. She needs a folder for school that costs $3, and she wants a bracelet that costs $8. If she buys the bracelet first, she may not have enough for the folder. The budget helps her see that the better plan is to take care of the need first.

This is one way income and expenses are different in a budget. Income tells what money is available. Expenses force choices about how that available money will be used.

People of all ages use budgets. Kids may budget for small goals, while adults may budget for groceries, housing, transportation, and saving for the future.

When students understand needs and wants, they become stronger decision-makers. They learn that every expense changes what money is still available.

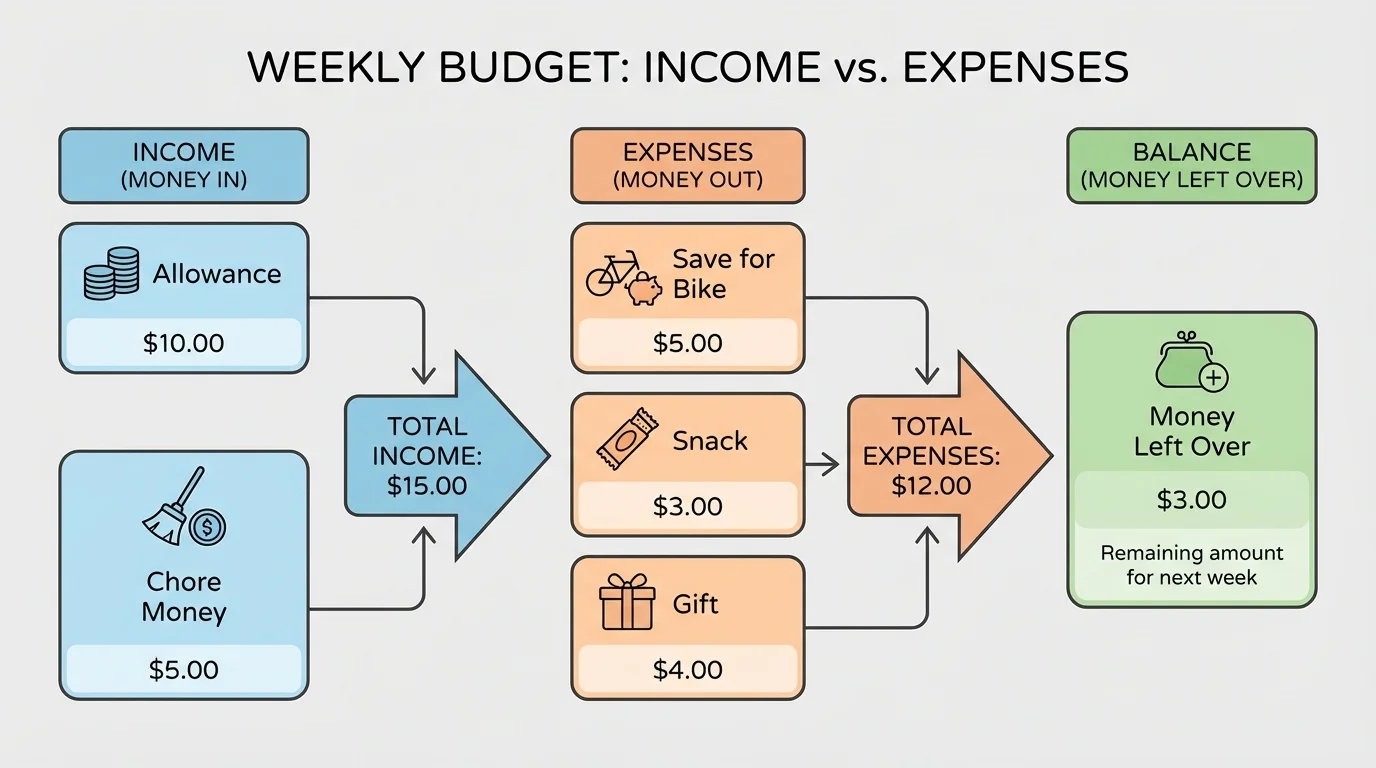

[Figure 3] A simple budget begins with a list of money coming in and money going out, illustrated with a weekly budget chart. You do not need anything complicated. You just need to be honest and careful.

Here is one way to make a simple budget:

Step 1: Write down all income.

Maybe you get $6 allowance and $4 for chores. Total income is \(6 + 4 = 10\).

Step 2: Write down planned expenses.

Maybe you plan to spend $2 on a snack and $3 on markers. Total expenses are \(2 + 3 = 5\).

Step 3: Find the amount left.

Subtract expenses from income: \(10 - 5 = 5\).

Step 4: Decide what to do with the money left.

You may save the $5, keep it for later, or use part of it for a goal.

| Category | Amount | Type |

|---|---|---|

| Allowance | $6 | Income |

| Chore money | $4 | Income |

| Snack | $2 | Expense |

| Markers | $3 | Expense |

| Money left | $5 | Saved or used later |

Table 1. A simple budget showing income, expenses, and money left over.

This budget works because it clearly separates income from expenses. That is the big idea. If you mix them together, it becomes harder to understand where your money comes from and where it goes.

Example: Building a budget

Sofia earns $9 by helping in the yard. She plans to buy a notebook for $4 and a fruit cup for $2.

Step 1: Write the income.

Sofia's income is $9.

Step 2: Add the expenses.

Her expenses total \(4 + 2 = 6\).

Step 3: Find the amount left.

She has \(9 - 6 = 3\) left.

Sofia can save $3 or use it later.

Notice that the budget is really a plan before spending happens. It helps you make choices ahead of time instead of wondering later where the money went.

A budget is especially helpful when you have a financial goal. A financial goal is something you want to do with money in the future. Maybe you want to save for a $20 art set or a $15 soccer ball.

Let's say Jayden wants a $20 board game. He already has $6. Each week he earns $4 in income. If he spends all $4 each week, his savings do not grow much. But if he plans his expenses carefully and only spends $1 each week, then he can save \(4 - 1 = 3\) each week.

After one week, he saves $3. After two weeks, he saves another $3. In two weeks, he adds \(3 + 3 = 6\) to the $6 he already has, for a total of \(6 + 6 = 12\).

He still needs \(20 - 12 = 8\) more. If he keeps following the budget, he gets closer to the goal. This is why budgets are powerful. They turn big goals into smaller, manageable steps.

Income supports the goal, and expenses shape the path. Income gives you the money you can work with. Expenses decide how much of that money remains. If you control your expenses wisely, more of your income can help you reach your goal.

Saving does not happen by accident very often. It usually happens because someone made a plan and followed it.

Budgets are not frozen forever. Sometimes income changes. Sometimes expenses change. A good budget can be adjusted.

Suppose Liam expected $10 of income, but he only got $7 this week. If his budget still includes $9 of expenses, then he now has a problem because \(7 - 9 = -2\). A negative result means he planned to spend $2 more than he has. He must change the plan.

He could remove one expense, choose a cheaper item, or wait until he has more income. This is another important difference between income and expenses. Income sets the limit. Expenses must fit inside that limit.

The same thing happens if a price changes. If a snack usually costs $2 but now costs $3, then the expense has increased. The budget must be updated so the plan stays accurate.

Example: Changing a budget

Nora has $11 of income planned. She wants to buy a pen for $3, a snack for $4, and a gift for $5.

Step 1: Add the expenses.

The total is \(3 + 4 + 5 = 12\).

Step 2: Compare to income.

Income is $11, but expenses are $12. Since \(12 > 11\), the plan does not work.

Step 3: Adjust the budget.

If Nora removes the $4 snack, then the new expense total is \(12 - 4 = 8\).

Now the budget works because \(11 - 8 = 3\). Nora has $3 left.

Checking your budget before spending helps you avoid mistakes. It is much easier to change a plan on paper than after money is already gone.

Good budgeting is not about being perfect. It is about paying attention. A few smart habits can help:

Students who practice these habits learn that money choices have results. Small expenses may seem tiny, but many small expenses can add up. For example, three snacks that each cost $2 make a total of \(2 + 2 + 2 = 6\). That $6 might have helped pay for something bigger later.

Budgets also help families and communities make decisions. Schools, teams, and clubs often have budgets too. They all must know how much money is coming in and what it will be used for. So, the same idea you use for your own budget is used in many real-world places.

When you understand the different roles of income and expenses, you become more confident with money. Income is the supply of money. Expenses are how that money is used. A budget brings them together so you can make a plan that helps you spend wisely and save for what matters.