A person can have the same job, want the same car, and apply for the same loan as someone else, yet pay thousands of dollars more over time. Why? Often the difference is not the car or the salary alone. It is the record of how that person has handled borrowed money in the past. In the financial world, your past behavior becomes evidence about your future reliability.

When people borrow money, lenders take a risk. A bank, credit union, or credit card company gives money now and expects repayment later. Because lenders cannot see the future, they study a person's credit history, which is the record of how that person has used credit over time. If someone usually pays on time and manages debt carefully, lenders see lower risk. If someone misses payments or leaves debts unpaid, lenders see higher risk.

This matters because borrowing power is more than just whether you are allowed to borrow. It also includes how much you can borrow, how expensive that loan will be, and what terms come with it. Two borrowers may both be approved, but one may get a lower interest rate, a higher credit limit, and a smaller required deposit.

Credit history is a record of a person's past borrowing and repayment behavior.

Borrowing power is a person's ability to qualify for credit, including the amount, interest rate, fees, and terms offered.

Lender means the person or institution that provides money or credit, while borrower means the person receiving and repaying it.

Credit history is important even for teenagers to understand because many financial choices start early. A student who becomes an authorized user on a family card, opens a first credit card after turning eighteen, applies for a car loan, or rents an apartment may begin creating a financial reputation that follows them for years.

A lender usually does not rely on guesswork. It often checks a credit report, which is a detailed record of credit accounts and payment behavior. A credit report may include loans, credit cards, balances, payment patterns, and serious problems such as accounts sent to collections. From information like this, companies may also produce a credit score, which is a numerical estimate of credit risk.

A credit report and a credit score are related, but they are not identical. The report is the full record. The score is a summary number based on that record. Think of it like a transcript and a GPA in school. The transcript shows the full details; the GPA gives a quick measure based on those details.

Lenders use these tools because they help answer practical questions. Has this person paid late before? Do they already owe a lot? Have they handled credit for a long time or only recently? Have they applied for many new accounts in a short period? These patterns help lenders decide how likely they are to be repaid.

A late payment can affect a credit profile for years, even though the actual late event may have lasted only a month. Financial records often move more slowly than everyday life.

That time lag is one reason financial decisions matter so much. A quick choice, such as ignoring a bill or maxing out a card, can stay visible long after the purchase itself is forgotten.

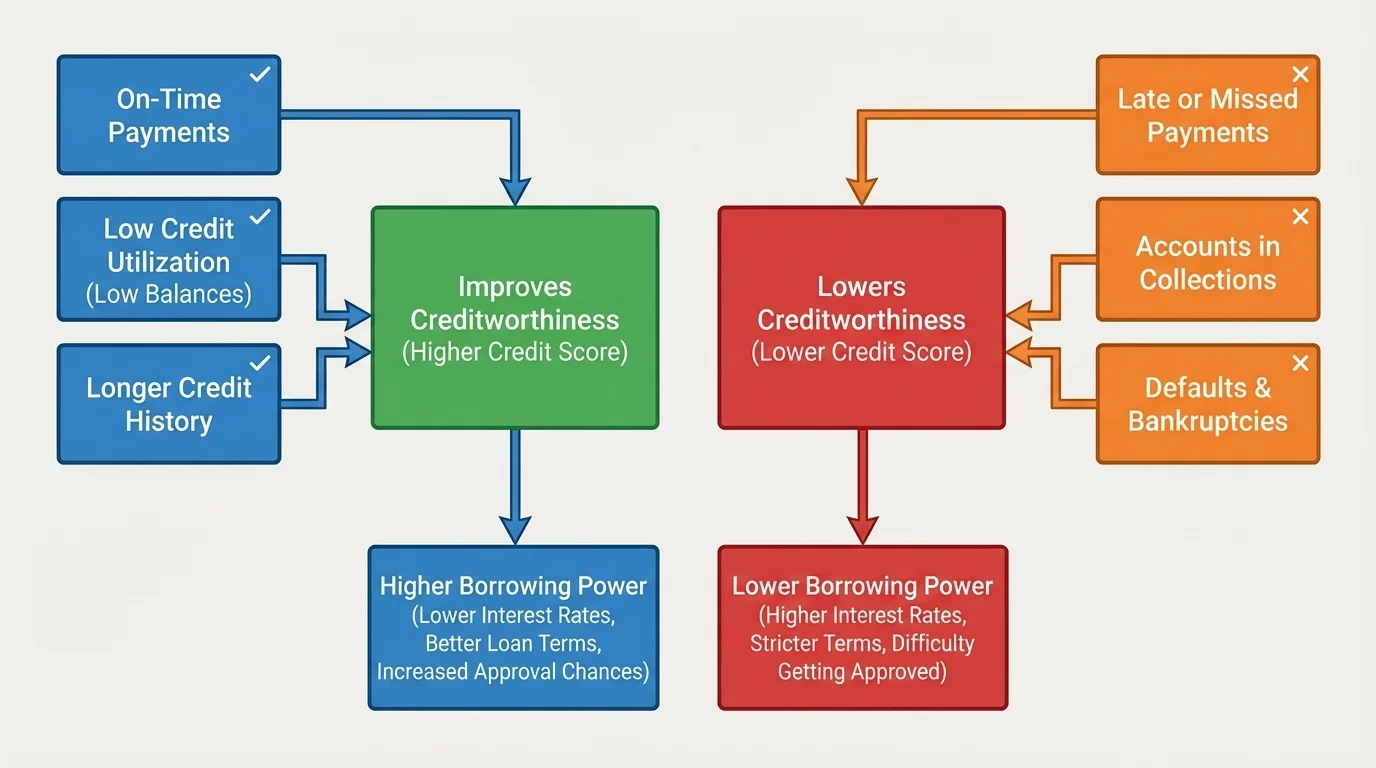

Credit history changes over time based on financial behavior, as [Figure 1] illustrates through actions that improve or weaken a credit profile. One of the biggest factors is payment history. People who make payments on time build trust with lenders. People who pay late, skip payments, or default on loans damage that trust.

Another important factor is how much of available credit a person is using. Suppose someone has a credit card with a $1,000 limit. If they owe $900, they are using a large share of the available credit. That can signal financial stress. If they owe $100 instead, they are using less of their limit, which usually looks safer to lenders. This idea is often called credit utilization.

The length of credit history also matters. A longer record gives lenders more evidence. Someone who has borrowed responsibly for several years may appear more predictable than someone with only a few months of history. New credit applications can matter too. Opening many accounts in a short period may suggest that a borrower urgently needs money.

Serious negative events can have a strong effect. These include accounts in collections, loan default, repossession, foreclosure, or bankruptcy. These events tell lenders that previous debts were not managed successfully, so future lending appears riskier.

Good credit history does not mean a person is rich, and bad credit history does not automatically mean a person is irresponsible in every part of life. Credit history is narrower than that. It is specifically about patterns of borrowing and repayment. But because lending decisions depend heavily on those patterns, the effects are real.

| Behavior | Likely Effect on Credit History | Why It Matters to Lenders |

|---|---|---|

| Paying bills on time | Improves credit standing | Shows reliability |

| Keeping balances low | Improves credit standing | Suggests lower financial strain |

| Missing payments | Hurts credit standing | Shows higher repayment risk |

| Opening many accounts quickly | May hurt credit standing | Can suggest urgent borrowing |

| Defaulting on a loan | Strongly hurts credit standing | Shows major failure to repay |

Table 1. Common financial behaviors and how they tend to affect a borrower's credit profile.

As the pattern in [Figure 1] makes clear, lenders are not reacting to one isolated number alone. They are reading a story told by repeated actions over time.

Borrowing power has several parts. First, there is approval: will the lender say yes or no? Second, there is the loan amount: how much money will the lender allow the borrower to receive? Third, there is the interest rate, which is the price of borrowing money. Fourth, there are the terms, such as how many months the borrower has to repay, whether a down payment is required, and whether extra fees or a security deposit apply.

A strong credit history can increase borrowing power in all of these areas. A weak credit history can reduce it. For example, a lender may approve a borrower with strong credit for a $15,000 car loan at a relatively low rate, while a borrower with weak credit may be approved for only $9,000, or may face a much higher rate that makes the same car unaffordable.

Risk and price in lending

Lenders treat interest rates like prices connected to risk. If a borrower seems more likely to repay, the lender may offer a lower rate. If the borrower seems more likely to miss payments, the lender often charges a higher rate to compensate for that risk. In other words, weaker credit usually makes borrowing more expensive.

This means credit history affects both access and cost. Even when someone can technically borrow, poor terms may make that borrowing a bad financial decision.

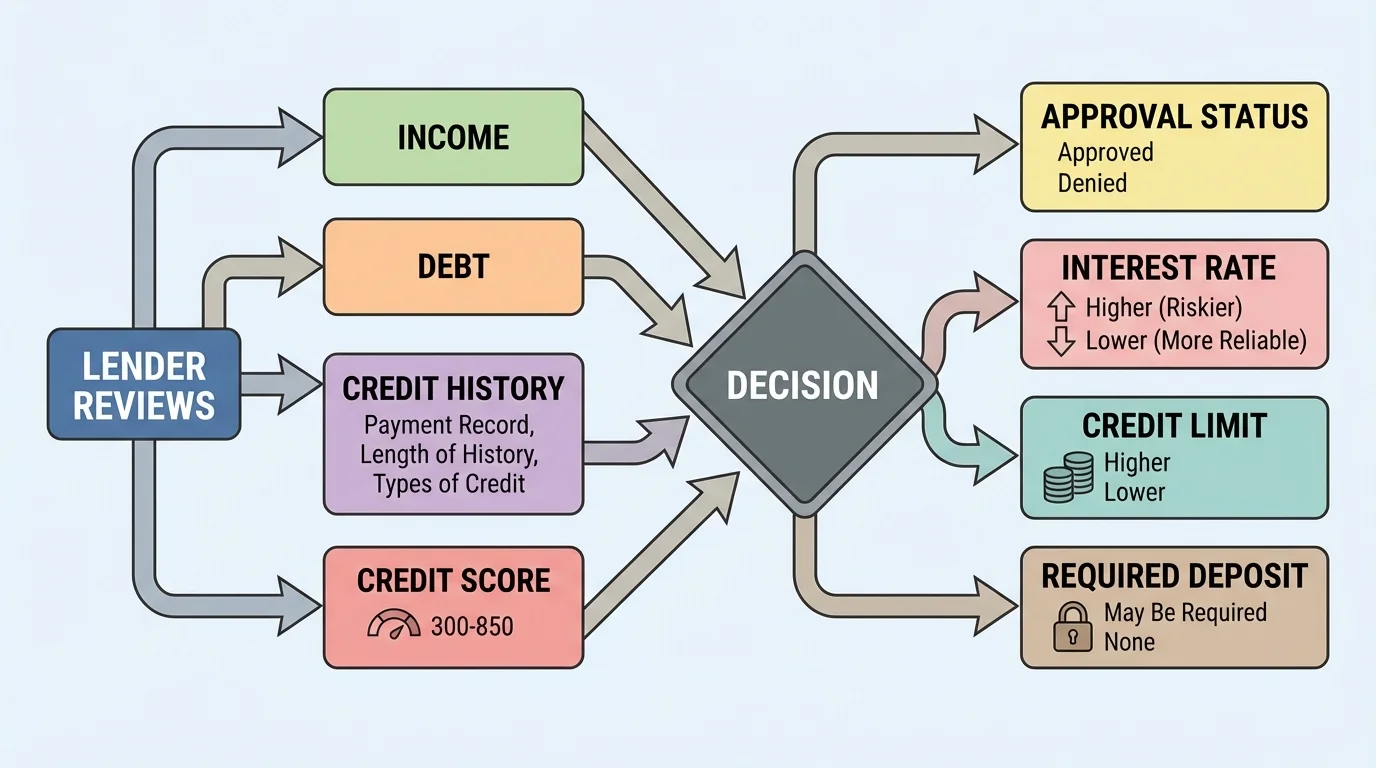

Lenders combine several pieces of information to judge risk, and [Figure 2] shows this as a decision pathway from application to final loan terms. Credit history is important, but it is not the only factor. Lenders may also look at income, job stability, current debt, and the value of any property tied to the loan.

Still, credit history often acts like a shortcut to trust. If a person has already shown a pattern of paying as promised, a lender may be more willing to offer favorable terms. If that pattern is weak, the lender may respond in several ways: deny the application, reduce the amount offered, raise the interest rate, shorten the repayment period, or require a co-signer or deposit.

For credit cards, this may appear as a lower credit limit. For apartments or utilities, it may appear as a larger security deposit. For auto loans, it may mean a higher down payment. The exact form changes, but the basic idea is the same: weaker credit history reduces the lender's confidence.

This is why two people with similar incomes may receive different offers. A lender is not only asking, "Can this person pay?" It is also asking, "How likely is this person to pay consistently and on time?" Credit history helps answer the second question.

For students, this can matter sooner than expected. A young adult with little or damaged credit may have trouble qualifying for a first apartment lease, a student-friendly credit card, or a reasonably priced car loan needed to get to work or college classes.

Consider two fictional borrowers, Maya and Jordan. Both want to borrow money for a used car so they can commute to school and work. Maya has a history of paying a starter credit card on time and keeping her balance low. Jordan has several late payments and one account sent to collections. Even if both now earn similar income, lenders may not treat them the same.

Maya may receive more offers, lower rates, and a higher approved amount. Jordan may receive fewer offers, face higher monthly payments, or need a co-signer. In some cases, Jordan may be denied entirely. That difference is borrowing power in action.

Case study: apartment application

Two recent graduates apply for the same apartment. The landlord reviews both applications.

Step 1: Applicant A has a strong credit profile.

The landlord sees consistent on-time payments and manageable debt. Applicant A is approved with a standard security deposit.

Step 2: Applicant B has a weaker credit profile.

The landlord sees missed payments and a collection account. Applicant B may still be approved, but only with a larger deposit or a guarantor.

Step 3: Compare the result.

Both applicants want the same housing, but their credit histories lead to different financial conditions. Better credit increases options and lowers barriers.

This pattern appears in many parts of life. A stronger credit profile can save money and create flexibility. A weaker one can force a person to delay plans, accept more expensive financing, or use savings for larger deposits instead of other goals.

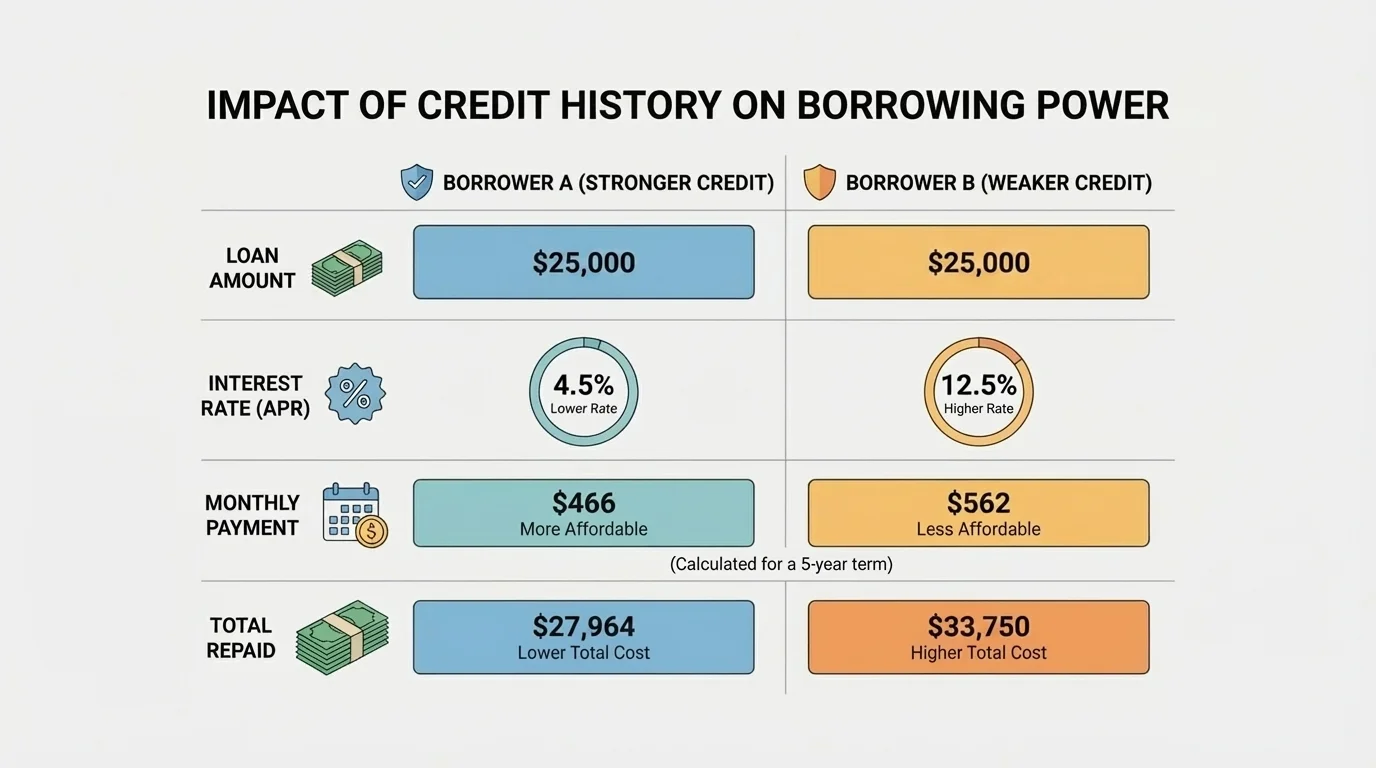

The numbers make borrowing power easier to see, and [Figure 3] compares how different credit profiles can change the cost of the same basic loan. Even a few percentage points in interest can create a major difference over time.

Suppose two borrowers each take a $10,000 car loan. To compare how credit history can affect borrowing cost, assume Borrower A has stronger credit and receives an annual interest rate of 6%, while Borrower B has weaker credit and receives an annual interest rate of 12%.

Using simple interest for a basic comparison, if Borrower A pays a rate of 6% for 3 years, the interest is calculated using \(I = Prt\). Substituting values gives \(I = 10{,}000 \times 0.06 \times 3 = 1{,}800\). The total repaid is \(10{,}000 + 1{,}800 = 11{,}800\).

If Borrower B, with weaker credit, pays 12% for 3 years, then \(I = 10{,}000 \times 0.12 \times 3 = 3{,}600\). The total repaid is \(10{,}000 + 3{,}600 = 13{,}600\).

The difference in interest alone is \(3{,}600 - 1{,}800 = 1{,}800\). That means the borrower with weaker credit pays $1,800 more on the same principal under this simplified model.

Worked example: comparing monthly affordability

A lender allows monthly loan payments up to $250. Compare two possible 36-month repayment plans.

Step 1: Stronger-credit offer

If the monthly payment is $230 for 36 months, the total paid is \(230 \times 36 = 8{,}280\).

Step 2: Weaker-credit offer

If the monthly payment is $250 for 36 months, the total paid is \(250 \times 36 = 9{,}000\).

Step 3: Compare the difference

The extra amount paid is \(9{,}000 - 8{,}280 = 720\).

Even when both borrowers stay within the same budget limit, the weaker-credit borrower gets less favorable terms and pays more overall.

These examples are simplified, but the main lesson is accurate: higher rates and stricter terms reduce what a borrower can comfortably afford. That means poor credit history can shrink choices, not just raise costs.

This comparison shows why borrowing power is not just about approval. It is about the entire financial package attached to the loan.

Building credit is usually less dramatic than damaging it. Good credit often grows through repeated ordinary habits: paying bills on time, borrowing only what can be repaid, keeping balances manageable, and avoiding unnecessary applications for new credit.

For young people, one smart principle is simple: never borrow to look wealthier than you are. Using credit to cover spending you cannot actually afford can quickly lead to high balances, late payments, and a damaged record. Budgeting and saving support healthy borrowing because they reduce pressure to rely on debt for everyday expenses.

Budgeting, spending, and saving choices affect borrowing decisions. A person who tracks expenses, builds emergency savings, and avoids overspending is better prepared to handle credit responsibly.

It is also important to check credit information for mistakes. Errors on a report can unfairly hurt borrowing power. Identity theft can also create accounts or debts a person never opened. Reviewing credit reports and disputing false information helps protect a financial reputation.

When problems do happen, improvement is still possible. Credit history is not fixed forever. Over time, consistent on-time payments and better debt management can rebuild trust, though serious negative marks may take years to fade.

Credit history affects more than a single purchase. It can influence transportation, housing, education, and even the ability to respond to opportunities quickly. A person with stronger credit may be able to finance a reliable car to get to work, qualify for housing with a lower deposit, or handle an emergency without facing extreme borrowing costs.

A person with weaker credit may need to spend more just to access the same things. That creates a difficult cycle. Higher borrowing costs can leave less money for saving, and less saving can make future financial shocks harder to manage. In that way, credit history becomes connected to the bigger picture of financial stability.

"Credit is easiest to get when you do not urgently need it."

— A practical rule of personal finance

Understanding credit history helps people make wiser decisions before they apply for a loan. It encourages them to think ahead: Will this borrowing help me reach a goal, or will it make future choices harder? That question belongs at the center of responsible personal finance.