Have you ever wondered where your money goes after you get allowance, birthday money, or payment for doing chores? Sometimes money seems to disappear one small purchase at a time. A snack here, a game there, and suddenly the amount in your pocket or account feels much smaller. Keeping track of money is like using a map. It helps you see where your money has been and where you want it to go next.

When people track money, they write down or record the money they spend and the money they save. This helps them answer important questions: How much money do I have now? What am I spending most of it on? Am I getting closer to my goal? A tracker turns guessing into knowing.

Tracking money also helps people be responsible. If you want to buy something special, such as a book, sports item, or art set, you need to know whether you can afford it. If you do not track your money, you might spend too much on small things and not have enough left for something important later.

Adults use money trackers too. They may use a notebook, a phone app, a spreadsheet, or records from a bank or credit union. Students can use simpler versions of the same idea. Learning this skill now builds habits that will help for many years.

Small amounts can add up surprisingly fast. Spending $2 each school day for five days means you spent $10 in one week.

That idea matters because many money choices are not huge. A person usually does not lose money all at once. Instead, money leaves in little pieces. If you record each piece, you can spot patterns and make better decisions.

A few key words make money tracking easier to understand. Income is money that comes in, such as allowance, gifts, or money earned from chores. An expense is money that goes out when you buy something. A balance is how much money you have after adding money in and subtracting money out.

Financial institution means a business that helps people manage money, such as a bank or credit union. An account is a safe place at a financial institution where money is kept and recorded.

When you keep your own money tracker, you are making a personal record. If your money is in a bank or credit union account, that financial institution also keeps a record. Good money management means your record and the institution's record should agree.

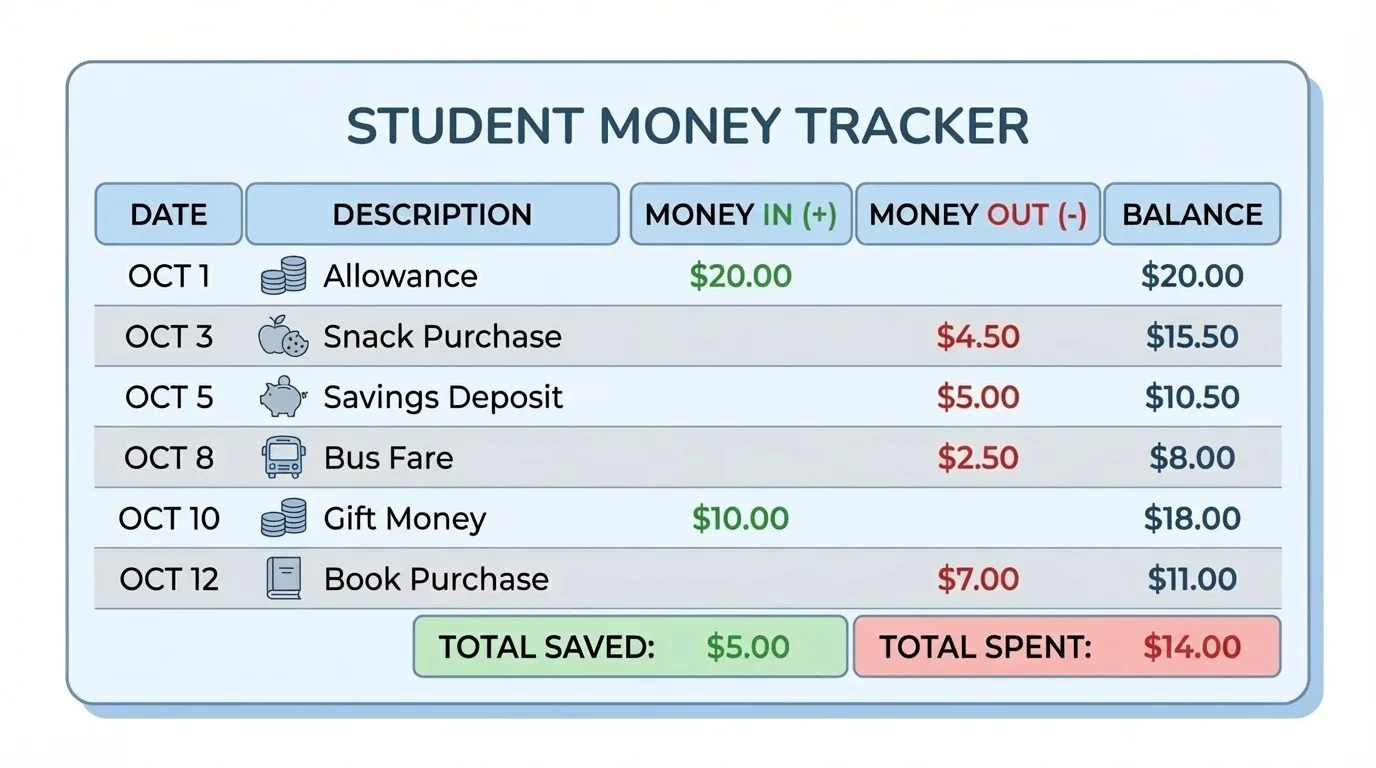

A strong money tracker has clear parts. The organizer in [Figure 1] shows that each row should tell a short story about one money action. A good tracker usually includes the date, what happened, the amount spent, the amount saved, and the new balance. When everything is placed in columns, it becomes easier to read and check.

You can make your own tracker on paper or on a device. One simple system uses five columns: Date, Description, Money In, Money Out, and Balance. Some students also add a Category column, such as food, fun, gift, or savings.

| Column | What goes there |

|---|---|

| Date | When the money activity happened |

| Description | What you bought or received |

| Money In | Money added, such as allowance or gift money |

| Money Out | Money spent on something |

| Balance | How much money you have after the change |

Table 1. The basic parts of a simple money tracker.

The balance is especially important. It changes every time you add or subtract money. If you start with $20 and spend $3, your new balance is found by subtraction: \(20 - 3 = 17\). If you later save $5 more, the balance changes by addition: \(17 + 5 = 22\).

A tracker works best when you fill it in right away. If you wait too long, you may forget a purchase or write the wrong amount. Good record-keeping is careful, honest, and regular.

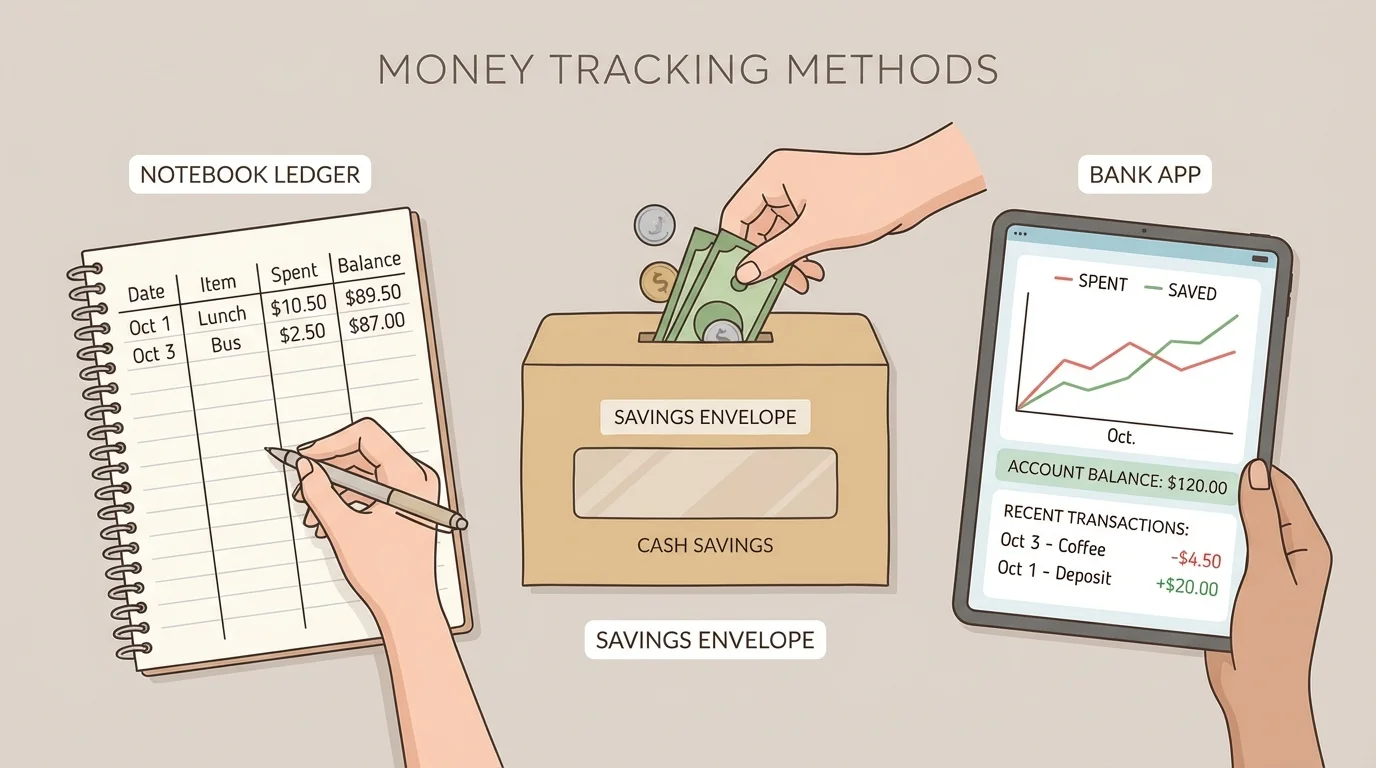

There is more than one good way to track money, and [Figure 2] illustrates three common choices. The best method is the one you can use accurately and often. Some students like paper because they can carry it easily. Others like digital tools because the totals can be updated quickly.

One way is a notebook tracker. In a notebook, you make a table and write each money action on a new line. Another way is the envelope method, where you label envelopes such as spending, saving, and gifts. You still record amounts, but the envelopes help you separate money by purpose. A third way is a bank app or online account, where a financial institution records deposits and withdrawals for you.

A spreadsheet is another useful choice. It can automatically do the math if you enter the numbers correctly. But even with digital tools, you still need to understand what the numbers mean. Technology helps, but it does not replace careful thinking.

Whichever method you choose, keep it simple at first. A complicated tracker that you never use is less helpful than a simple one you use every day.

Addition helps when money comes in. Subtraction helps when money goes out. A running total changes after every money action.

That running total is the heart of your tracker. Each new amount depends on the amount before it, so one mistake can affect everything after it. That is why checking your math matters.

When you spend money, you write the amount in the money-out column and subtract it from your current balance. Be sure to include even small purchases. A small amount still changes the total.

Worked example 1

You start with $15. You buy a notebook for $4.

Step 1: Identify the starting balance.

The starting balance is \(15\).

Step 2: Identify the money spent.

The money out is \(4\).

Step 3: Subtract to find the new balance.

\(15 - 4 = 11\)

Your new balance is $11.

Notice that the purchase is not just a number. It also needs a label, such as "notebook," so you remember what the money was used for. Later, those labels help you notice patterns in your spending.

Here is another subtraction example using several purchases in one week. Suppose your balance is $18. On Monday you spend $2 on a snack, and on Wednesday you spend $5 on markers. First subtract the snack: \(18 - 2 = 16\). Then subtract the markers: \(16 - 5 = 11\). Your new balance is $11.

Worked example 2

A student has $24 and spends $3 on a snack and $6 on a small toy.

Step 1: Subtract the first expense.

\(24 - 3 = 21\)

Step 2: Subtract the second expense from the new balance.

\(21 - 6 = 15\)

Step 3: Check total spending.

Another way is to add the expenses first: \(3 + 6 = 9\), then compute \(24 - 9 = 15\).

The balance after both purchases is $15.

Both methods give the same answer. That is a good way to check your work.

Saving money means keeping some of it for later instead of spending it now. When money is added to your tracker, you write it in the money-in column and add it to your balance. This could happen when you receive allowance, birthday money, or money from chores.

Saving first means setting aside money before spending on extras. Many people find this easier than waiting to see what is left over at the end.

If your balance is $12 and you receive $8, you add: \(12 + 8 = 20\). The new balance is $20. If you decide that all $8 should go toward a savings goal, you still record it as money in because it increases the total amount you have.

Some trackers use special categories to show where saved money is going. For example, you might label one entry "bike fund" or "gift fund." This makes saving feel more real because the money has a job.

Worked example 3

You have $9. You earn $7 from helping clean the yard, then save $4 more from gift money.

Step 1: Add the first amount of money in.

\(9 + 7 = 16\)

Step 2: Add the second amount of money in.

\(16 + 4 = 20\)

Step 3: State the balance.

The final balance is \(20\).

You now have $20.

Money tracking is not only about what leaves your wallet or account. It is also about noticing what grows when you choose to save.

Looking at one day is helpful, but looking at a whole week is even better. A weekly tracker helps you see habits. You may discover that you spend the most on snacks, or that you usually save more on days when you pack your own food instead of buying something extra.

Suppose a student starts the week with $10. On Monday, they get $5 allowance. On Tuesday, they spend $2 on a snack. On Thursday, they save $3 from chore money. On Friday, they spend $4 on a game card. The running balance changes like this: start with \(10\), then \(10 + 5 = 15\), then \(15 - 2 = 13\), then \(13 + 3 = 16\), then \(16 - 4 = 12\). The final balance is $12.

Using categories can make the weekly tracker even more useful. If you add all snack purchases together and get \(2 + 3 + 1 = 6\), you know $6 went to snacks that week. If you add all savings deposits and get \(5 + 3 = 8\), you know you saved $8.

| Day | Action | Math | Balance |

|---|---|---|---|

| Start | Beginning amount | \(10\) | $10 |

| Monday | Allowance | \(10 + 5 = 15\) | $15 |

| Tuesday | Snack | \(15 - 2 = 13\) | $13 |

| Thursday | Chore money saved | \(13 + 3 = 16\) | $16 |

| Friday | Game card | \(16 - 4 = 12\) | $12 |

Table 2. A sample weekly money tracker showing a running balance.

As you saw earlier in [Figure 1], each entry changes the next balance. That is why reading a tracker from top to bottom matters. The order of events tells the money story clearly.

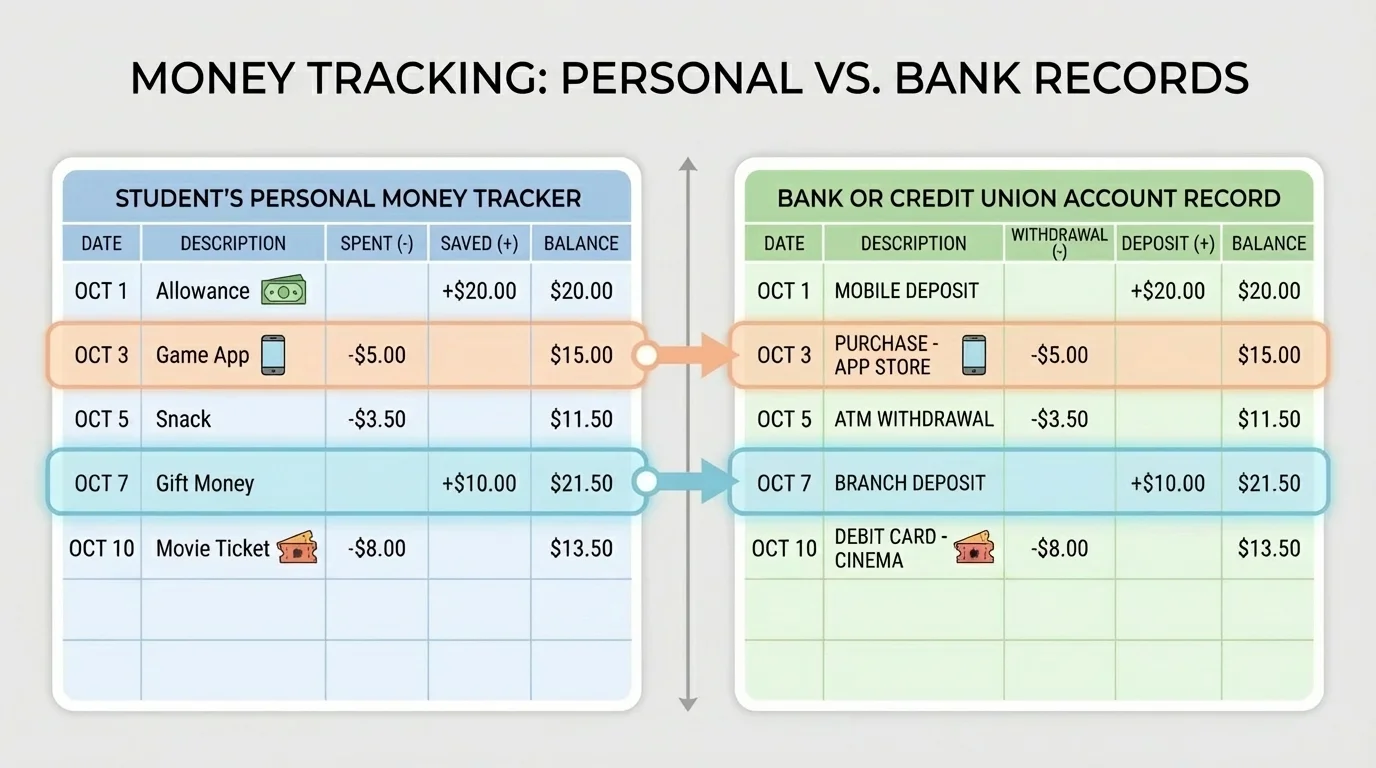

Banks and credit unions are financial institutions that help people store money safely and keep records of deposits and withdrawals. When your money is in an account, the institution records each change. A careful money manager compares personal records with institution records, and [Figure 3] shows how the entries should line up.

If your notebook says you deposited $10 on Tuesday, the bank or credit union record should also show that deposit. If your tracker shows a purchase for $3, the account record should show the same amount if that money came from the account. This process is called checking or matching records.

Sometimes the records do not match. Maybe you forgot to write something down. Maybe you copied a number incorrectly. Maybe a deposit has not appeared yet. Comparing line by line helps you find the difference.

This is one reason financial institutions are useful. They do more than hold money. They also provide records that help people manage, review, and protect their finances.

Checking records example

Your tracker shows a starting balance of $30. Then you deposit $10 and spend $6.

Step 1: Update your own tracker.

\(30 + 10 = 40\), then \(40 - 6 = 34\)

Step 2: Compare with the account record.

If the bank record also shows one deposit of $10 and one withdrawal of $6, the ending balance should be \(34\).

Step 3: Look for mismatches.

If the account says \(35\) instead, one record may contain an error that needs checking.

Matching records helps keep your money information correct.

Later, when people use debit cards, online transfers, or savings accounts more often, this checking skill becomes even more important.

A money tracker is useful only if you read it and learn from it. After a week or two, look back and ask questions. What did I spend the most on? What was worth it? What could I spend less on? How much did I save?

You can use the answers to set goals. For example, if you want to save $40 for a new soccer ball and already have $12, you can find how much more you need: \(40 - 12 = 28\). If you plan to save $7 each week, then \(28 \div 7 = 4\). It will take 4 weeks to reach the goal if you stay on track.

"Tell your money where to go instead of wondering where it went."

This idea is powerful because it turns money from a mystery into a plan. The same tracker that records the past can help guide future choices.

Looking back at [Figure 2], notice that every method works best when the information is clear and updated often. The tool matters, but the habit matters even more.

One common mistake is forgetting small purchases. Another is waiting too long to record an entry. Some people also mix up money spent with money saved. For example, putting $5 into savings is not money leaving your total funds if you still own it; it is money moved into a savings category.

Math mistakes can also cause trouble. If your starting balance is $25 and you spend $8, the new balance is \(25 - 8 = 17\), not \(18\). If you make one small error, every later balance can become incorrect.

Another mistake is not using clear descriptions. Writing only "stuff" or "item" is not helpful later. A better description would be "snack," "gift," "markers," or "allowance." Clear words make the tracker easier to understand.

Comparing with institution records, as shown again in [Figure 3], helps catch many of these mistakes. Your own tracker and the financial institution record work together like two ways of checking the same answer.

Suppose Maya wants to buy a craft kit that costs $36. She currently has $14. She needs \(36 - 14 = 22\) more. Maya decides to track every dollar for the next few weeks.

In week 1, she earns $6 from chores and spends $2 on a snack. Her balance changes by \(14 + 6 = 20\), then \(20 - 2 = 18\). In week 2, she gets $5 as allowance and spends $1 on stickers. Her balance changes by \(18 + 5 = 23\), then \(23 - 1 = 22\). In week 3, she receives $4 from helping a neighbor and spends nothing extra, so her balance becomes \(22 + 4 = 26\).

Maya still needs \(36 - 26 = 10\). Because she tracked her money, she can see exactly how close she is to her goal. She also notices that snacks and small extras slowed her progress a little. That does not mean she can never buy small things. It means she understands the trade-off. Spending some money now may mean waiting longer for a bigger goal.

That is the real power of money tracking. It helps people choose, plan, and use financial tools wisely. Whether the money is kept in a jar, an envelope, or a bank account, a good tracker helps make every dollar easier to understand.