A paycheck can stay the same while life quietly gets more expensive. A meal that used to cost $8 becomes $10. Gas rises. Rent rises. Streaming service prices rise. Even school lunch or athletic fees may increase. The strange part is that nothing about the paper money itself has changed, yet that money suddenly does less work. That is why inflation matters: it changes what people can afford, what they save, and what choices they must make.

In personal finance, people often focus on how much money they have. But a more important question is what that money can actually buy. If your income rises by a small amount while prices rise faster, you may feel poorer even though your paycheck is larger. This is one reason many families pay close attention not just to income, but also to rising prices in groceries, housing, transportation, medical care, and utilities.

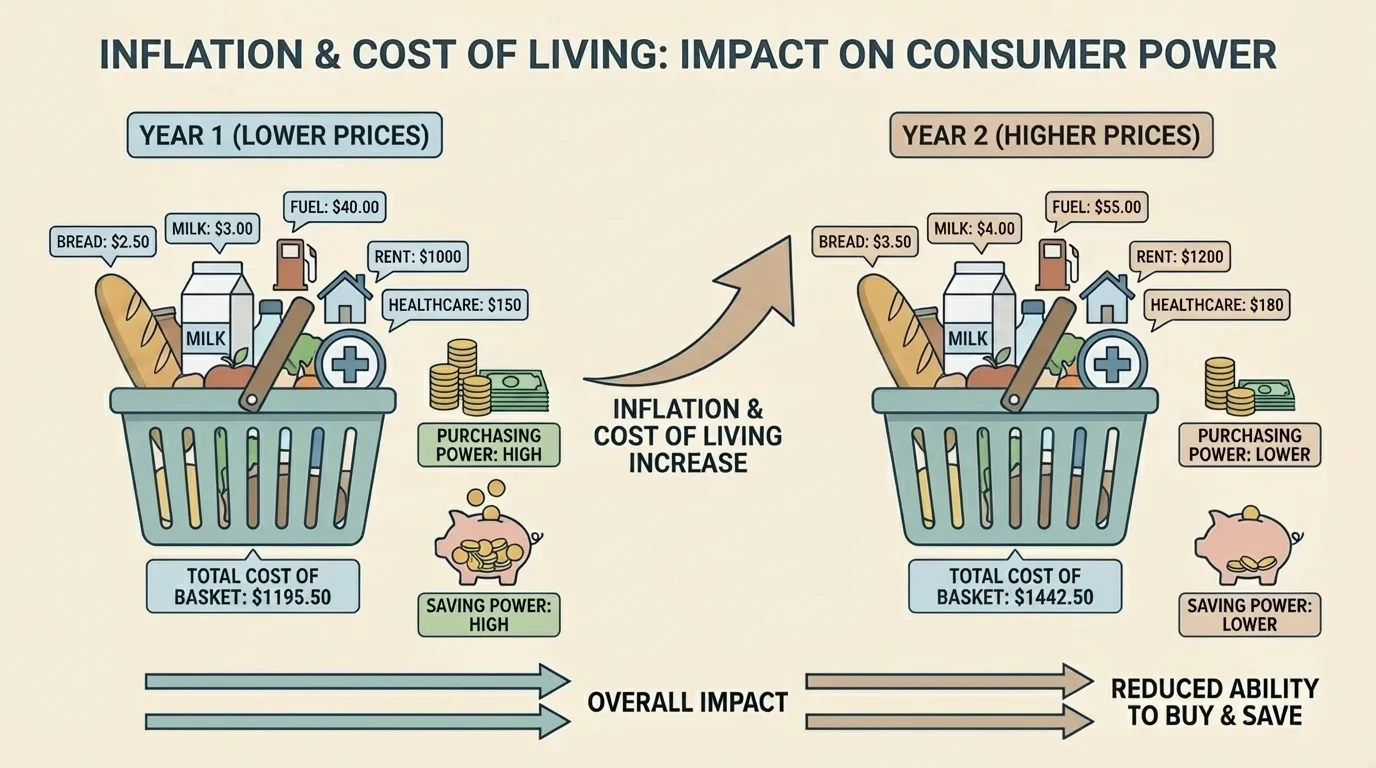

[Figure 1] Understanding inflation helps consumers make smarter decisions. It affects how people plan budgets, when they save, what they buy now versus later, and how they use credit. It also explains why two people with the same income may experience very different levels of financial pressure depending on where they live and what expenses they face.

Inflation is a general rise in prices over time.

Cost of living is the amount of money needed to cover basic expenses such as housing, food, transportation, and health care in a certain place and time.

Purchasing power is the amount of goods and services money can buy.

Saving power is the ability of saved money to keep or increase its value over time after accounting for rising prices.

Real income is income adjusted for inflation, showing what income can actually buy rather than just its face value.

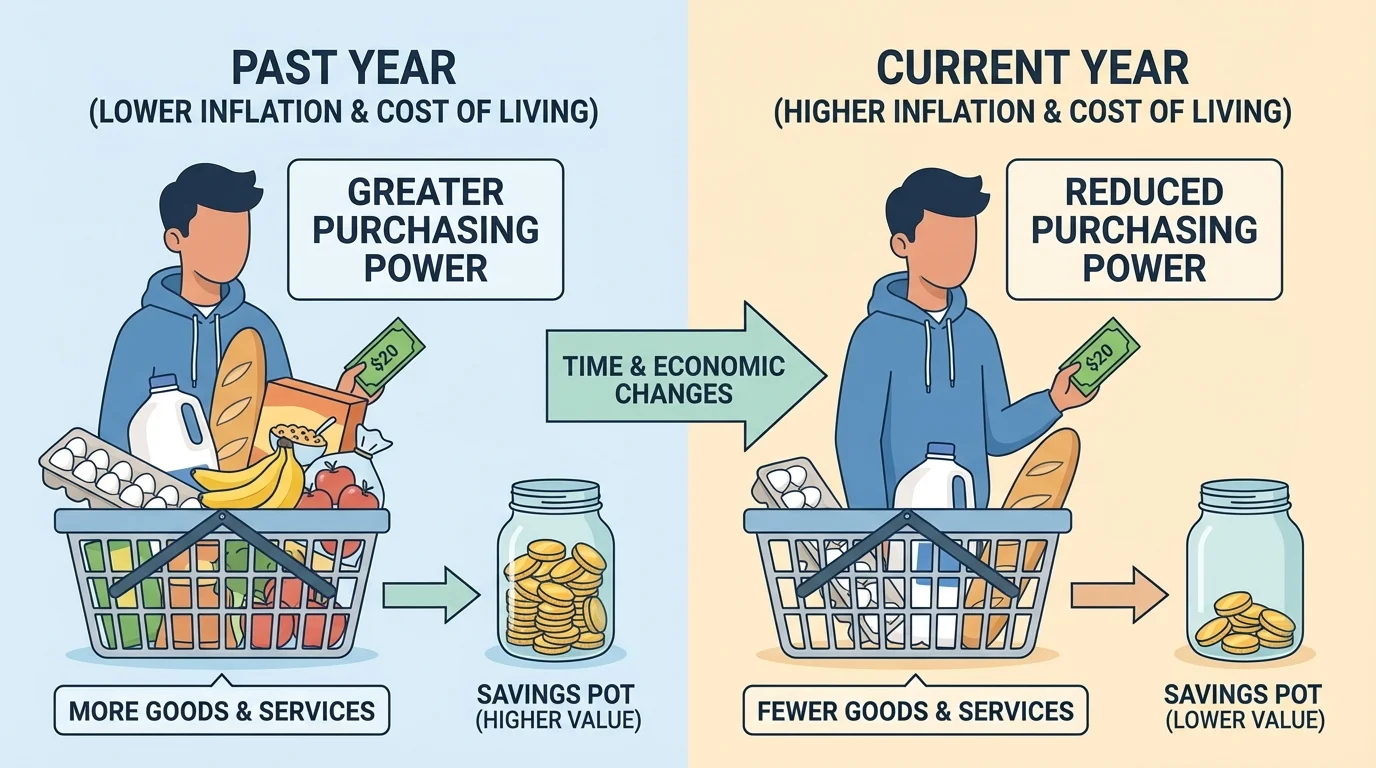

[Figure 2] These ideas are connected. Inflation pushes up prices. Higher prices increase the cost of living. A higher cost of living reduces purchasing power unless income rises enough to keep up. At the same time, inflation can weaken saving power if money in a savings account grows more slowly than prices do.

Economists often track Consumer Price Index changes by looking at a "market basket" of goods and services that typical households buy. This basket may include food, rent, transportation, clothing, and medical costs. By comparing the total cost of that basket in different years, economists estimate how much prices have changed overall.

A common way to express inflation is as a percentage increase in prices over time. The basic formula is

\[\textrm{Inflation rate} = \frac{\textrm{New price level} - \textrm{Old price level}}{\textrm{Old price level}} \times 100\%\]

Suppose a basket of goods costs $200 one year and $214 the next year. The inflation rate is

\[\frac{214 - 200}{200} \times 100\% = \frac{14}{200} \times 100\% = 7\%\]

That means average prices increased by 7\% over that period.

Inflation does not mean every price rises by the same amount. Some prices rise quickly, some slowly, and some may even fall. For example, food prices might jump because of drought or supply problems, while the cost of some electronics may fall because technology becomes cheaper to produce. What matters is the overall pattern of prices.

There is also a difference between a one-time high price and ongoing inflation. If the price of eggs rises sharply for a short time, that is a price spike. If many prices across the economy keep rising over months and years, that is inflation. This difference matters because long-term budgeting depends on broad price trends, not just one expensive item.

Purchasing power falls when the same amount of money buys fewer goods and services. This is one of the most direct ways inflation affects consumers. If you have $50 and your usual weekly purchases now cost $55 instead of $50, your money has lost purchasing power.

Think about a student who buys lunch, fuel, and school supplies each week. Last year, $30 might have covered five lunches at $5 each plus a small snack. If lunches rise to $6 each, those same five lunches now cost $30 before the snack is added. The student has not lost any dollars, but the dollars have lost buying ability.

This effect can be shown mathematically. If an item cost $40 and now costs $46, the percentage increase is

\[\frac{46 - 40}{40} \times 100\% = \frac{6}{40} \times 100\% = 15\%\]

A consumer who used to buy that item regularly must now either spend more, buy less often, or choose a substitute.

Worked example: comparing what the same money buys

A student has $25 for entertainment. Movie tickets cost $10 each last year and $12.50 each this year. How many tickets can the student buy each year?

Step 1: Divide the budget by last year's ticket price.

\[\frac{25}{10} = 2.5\]

Last year, the student could buy 2 tickets and still have some money left.

Step 2: Divide the same budget by this year's ticket price.

\[\frac{25}{12.5} = 2\]

This year, the student can buy exactly 2 tickets.

Step 3: Interpret the result.

The amount of money stayed the same, but the number of tickets fell from 2.5 possible tickets to 2. That is a drop in purchasing power.

Consumers often respond to reduced purchasing power in several ways. They may delay nonessential purchases, switch to store brands, buy in bulk, use coupons, compare prices online, or look for secondhand options. These are not just shopping habits; they are economic responses to inflation.

As seen earlier in [Figure 1], inflation is measured across a basket of goods, but households feel it personally through day-to-day choices. A family may decide to eat out less often because restaurant prices rose faster than grocery prices. Another may carpool because transportation costs climbed. Inflation becomes real when it changes behavior.

Cost of living is closely related to inflation, but it is not exactly the same thing. Inflation is the rate at which prices rise. Cost of living is the total amount needed to maintain a certain standard of living in a particular place. A city with high rent, expensive transportation, and costly food has a higher cost of living than an area where those expenses are lower.

This means that the same income may stretch very differently in different locations. A person earning $40,000 in a small town may have lower housing costs than someone earning $40,000 in a large city. If rent, insurance, and transit costs are much higher in the city, the second person may have less money left for saving or recreation.

Cost of living is about place, timing, and lifestyle. Two households can face different financial pressure even in the same city because their needs differ. A person with a long commute spends more on fuel or transportation. A family with medical needs may face higher health expenses. Cost of living depends on both market prices and personal circumstances.

Some expenses are fixed, meaning they stay about the same each month, such as rent or a car payment. Others are variable, such as food, gas, or entertainment. Inflation can hit both kinds of expenses, but variable expenses often show changes first and most visibly. Students notice this when snack prices, bus fares, or clothing costs increase.

Because of cost-of-living differences, budgeting should never be copied blindly from someone else. A sample budget online may look realistic, but it may not fit local rent prices or transportation needs. Smart consumers adjust budgets to the real prices in their own area.

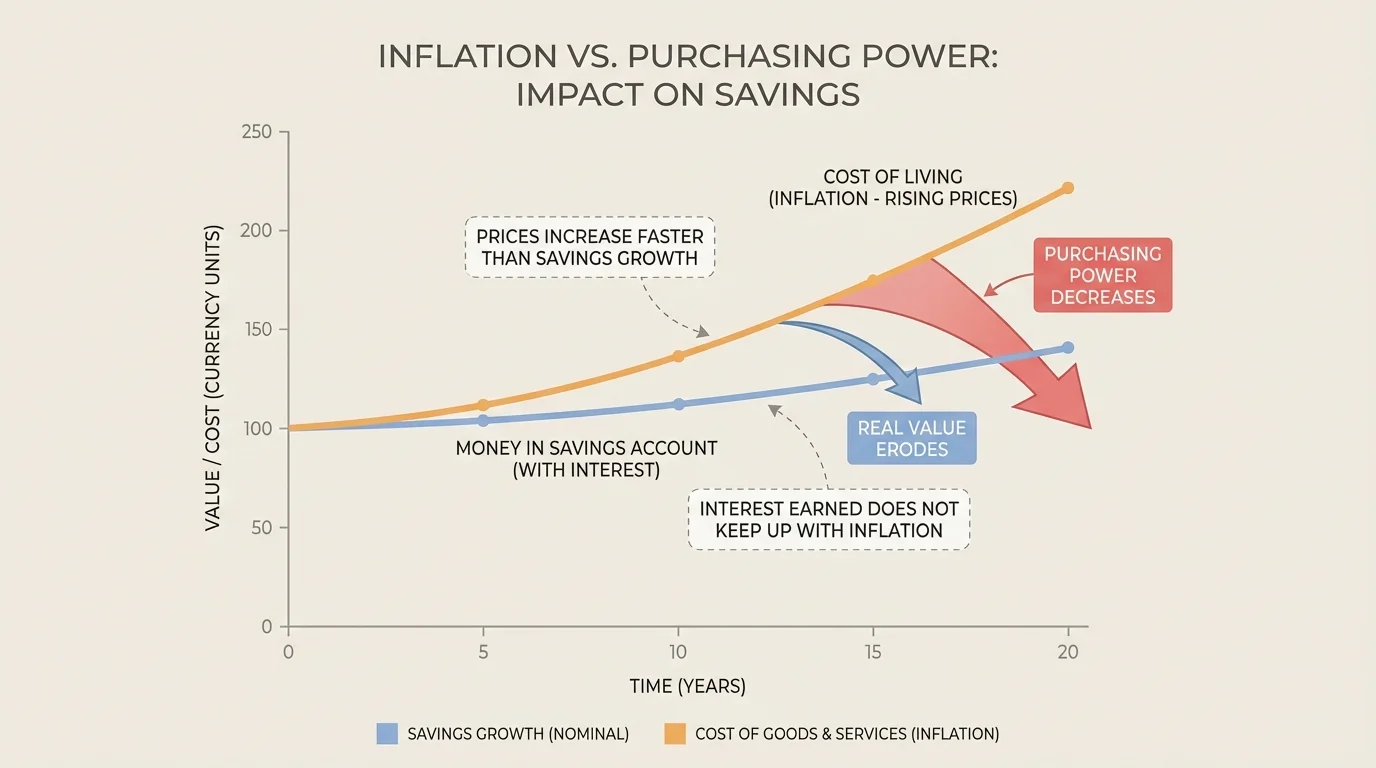

[Figure 3] Real return matters because a savings account balance can grow while its actual buying power shrinks. If money earns interest more slowly than prices rise, then the saver is losing saving power. This is one of the least obvious but most important effects of inflation.

There is a difference between nominal value and real value. The nominal value is the number printed in the account balance. The real value is what that balance can buy after accounting for inflation. If your savings account grows from $1,000 to $1,020, that sounds positive. But if prices rose by 4% during the same time, your money did not keep up.

A simple way to estimate real change is to compare the interest rate with the inflation rate. If savings earn 2% but inflation is 5%, then the approximate real change is about -3%.

Worked example: inflation versus savings growth

A student saves $500 in an account paying 3% annual interest. Over the same year, prices rise by 6%. What happens to the student's saving power?

Step 1: Find the new account balance.

\[500 + (0.03)(500) = 500 + 15 = 515\]

The nominal balance becomes $515.

Step 2: Compare the account growth with inflation.

The account grew by 3%, but prices rose by 6%.

Step 3: Estimate the real change.

\[3\% - 6\% = -3\%\]

The student's money increased in dollar amount, but its buying power fell by about 3%.

This is why people often look for savings tools or investments that may earn more over time, although higher returns usually involve more risk. For short-term goals, people may accept lower returns for safety and quick access. For longer-term goals, they may seek growth that has a better chance of outpacing inflation.

Later, when comparing options like savings accounts, certificates of deposit, bonds, or investing, the key point illustrated in [Figure 3] remains the same: it is not enough for money to grow in number alone. It must grow enough to protect real buying power.

Even moderate inflation can have a powerful effect over time. If prices rise by 3% per year for many years, the total cost of everyday life can become much higher even without any single dramatic price jump.

People on fixed incomes are especially vulnerable. If someone receives the same monthly amount from a pension or other source while prices keep rising, that money buys less each year. Retirees, people receiving limited benefits, and households with little room in their budget often feel inflation most sharply.

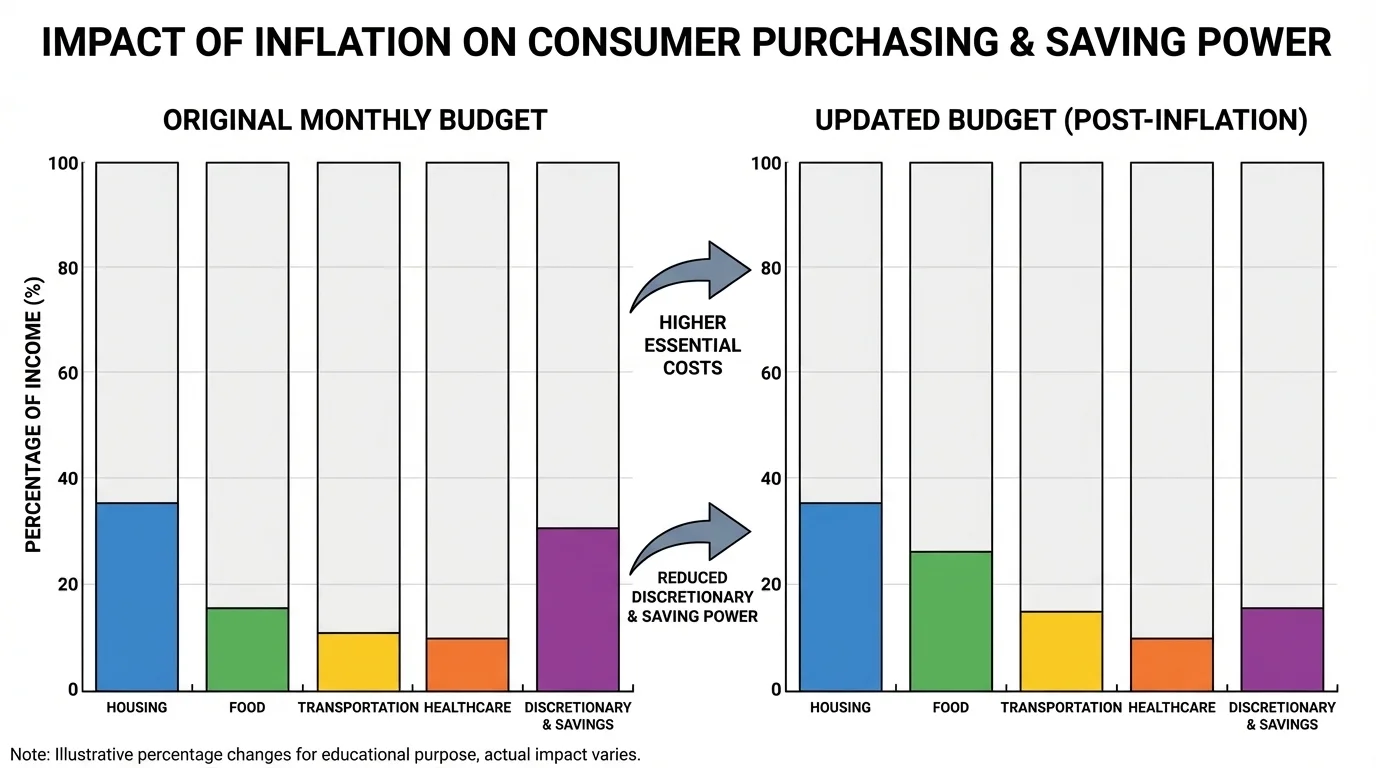

[Figure 4] When inflation rises, strong consumer skills become essential. A budget is not just a list of expenses; it is a decision-making tool. Students learning to manage money should recognize that inflation can force trade-offs between needs, wants, and future goals.

In a budget under pressure, consumers often shift money away from discretionary spending and toward necessities. If food and transportation costs rise, there may be less room for entertainment, subscriptions, or impulse purchases. That does not always mean giving up enjoyment; it means choosing intentionally.

One useful strategy is to separate expenses into categories such as needs, wants, and savings. If inflation causes needs to take a larger share of income, the other categories must adjust unless income also rises. This is one reason emergency funds matter. Unexpected price increases are easier to handle when savings already exist.

Borrowing decisions also change during inflation. Credit cards may help cover higher prices in the short term, but carrying a balance can become dangerous if interest charges are high. A person who relies on credit to handle rising living costs may end up paying much more later. That reduces future financial flexibility.

At the same time, inflation can affect borrowers and lenders differently. If someone has a fixed-rate loan, inflation may make repayment easier in real terms because future dollars are worth less than current dollars. However, this does not make borrowing automatically wise. The monthly payment must still fit the budget, and new loans may come with higher interest rates if lenders expect inflation.

| Financial choice | Possible effect during inflation | Smart consumer response |

|---|---|---|

| Buying groceries | Food costs rise and reduce disposable income | Compare unit prices, switch brands, plan meals |

| Using savings | Cash may lose buying power over time | Keep emergency money accessible, but review return rates |

| Using credit cards | Higher balances become expensive with interest | Avoid borrowing for routine overspending when possible |

| Signing a lease | Housing costs may rise in future periods | Read terms carefully and plan for total monthly costs |

| Transportation choices | Fuel and maintenance may increase | Carpool, compare routes, budget for variable costs |

Table 1. Examples of how inflation influences personal budgeting, spending, saving, and borrowing decisions.

Just as [Figure 4] shows a budget shifting toward necessities, real households often respond by making substitutions rather than simply spending more. Choosing generic medication, repairing a device instead of replacing it, or waiting for seasonal sales are all examples of consumer adaptation.

Inflation does not affect everyone equally. People with wages that rise quickly may keep up or even move ahead. People whose wages stay flat fall behind. Savers with money sitting in low-interest accounts may lose buying power, while some borrowers with fixed-rate debt may benefit because they repay loans with less valuable dollars.

Fixed income households usually face the greatest pressure. If monthly income remains unchanged while rent, food, and medicine rise, those households must cut other spending or use savings. In contrast, workers in fields with strong wage growth may be better able to handle inflation.

Worked example: nominal wage versus real wage

A worker's hourly pay rises from $15 to $15.60 over one year. During that year, inflation is 5%. Did the worker's real earning power rise or fall?

Step 1: Find the percentage increase in wage.

\[\frac{15.60 - 15.00}{15.00} \times 100\% = \frac{0.60}{15.00} \times 100\% = 4\%\]

The nominal wage increased by 4%.

Step 2: Compare wage growth with inflation.

Wage growth is 4%, but inflation is 5%.

Step 3: Estimate the real change.

\[4\% - 5\% = -1\%\]

The worker's real earning power fell by about 1%.

This explains why people may say, "I got a raise, but it does not feel like it." If prices increase faster than income, the raise does not fully protect purchasing power. Looking only at the paycheck can be misleading; the more important measure is what that paycheck can buy.

For students, inflation may seem like something adults or economists worry about, but it already affects everyday choices. It changes the price of rideshare trips, snacks after practice, concert tickets, textbooks, gas for part-time jobs, and college costs. It also influences decisions about whether to save birthday money, spend it now, or compare prices more carefully.

A smart consumer asks several questions during inflation: Which expenses are rising fastest? Are these needs or wants? Can I substitute a cheaper option? Is this the right time to borrow? Is my savings strategy keeping up with price increases? These questions help turn an economic concept into practical action.

Good budgeting already requires tracking income, fixed expenses, variable expenses, and financial goals. Inflation does not replace these skills; it makes them more important because small price increases across many categories can create a large total impact.

One useful habit is reviewing a budget regularly instead of assuming old numbers still work. If transportation used to cost $80 per month and now costs $95, or if lunch spending rose from $40 to $55, those updates should be reflected in the budget. Otherwise, overspending happens quietly.

Another smart habit is comparison shopping. Online tools make it easier to compare price per ounce, delivery fees, subscriptions, and contract terms. When inflation is high, careless spending becomes more expensive, so informed spending becomes more valuable.

Inflation cannot be controlled by individual consumers, but responses to it can. Strong long-term habits include building an emergency fund, increasing savings when income rises, avoiding unnecessary high-interest debt, and learning the difference between short-term cash storage and long-term growth strategies.

It also helps to understand that not all inflation is equally harmful. Mild inflation can happen in growing economies. The problem becomes serious when prices rise faster than wages and savings, making it difficult for households to afford basic needs or plan confidently for the future.

"It's not how much money you make, but how much money you keep, how hard it works for you, and how many generations you keep it for."

— Robert Kiyosaki

That idea connects directly to inflation. Keeping money is not enough if its value erodes. Making money "work" includes protecting its purchasing power. For consumers, this begins with awareness: knowing that a dollar amount alone does not tell the full story.

When people understand inflation and cost of living, they become better decision-makers. They can judge whether income is truly improving, whether a budget is still realistic, whether savings are holding value, and whether borrowing is helping or hurting. Those skills matter not just in economics class, but in every stage of adult financial life.